Artificial intelligence (AI) is a buzzword in tech these days. The term, which encompasses a range of technologies including machine learning and data analysis. The goal is to create systems that can perceive, learn, and reason in ways that mimic human capabilities. At its best, AI will allow machines to understand the gestalt of a situation and react accordingly, a capability that humans take for granted – but has tended to elude computer systems, which in their turn excel at analyzing minute details.

A wide range of tech companies are working on AI systems; artificial intelligence holds the promise of real-time data analysis and situation monitoring, with the machines capable of handling routine decisions. While it hasn’t been achieved yet, the outlines of success are visible on the horizon.

Every smart investor knows to keep his eyes on the horizon; that is, to plan every investment with long-range intentions. Just how long is up to the individual, but most investors agree that a move isn’t long-term unless it’s held for more than one year. Warren Buffett has famously said, “If you are not willing to own a stock for 10 years, do not even think about owning it for 10 minutes.”

With this in mind, we used TipRanks’ database to identify three AI stocks that have been highlighted by some of Wall Street’s best tech sector analysts. These are analysts with 5-star ratings, standing above their peers in accuracy and average returns – and they’ve tapped Artificial Intelligence as a tech segment for the long run.

Veritone, Inc. (VERI)

We’ll start with Veritone. This media tech company offers a cloud-based operating system for AI that uses machine learning to turn data into useful intelligence. The software allows users to process audio and video in real time, enhance analytics and research apps, reduce content review times, and streamline time spent on ‘low-value, high-effort’ tasks.

The value of the product to the customers can be seen in the quarterly earnings trends and the share appreciation. The last six months – covering the worst of the global pandemic and economic recessionary pressures – have seen VERI’s earnings steadily improve and the share price rise to its best level in over two years. Earlier this month, Veritone showed its confidence by adjusting its Q2 revenue guidance upwards. The guidance, of $13.1 to $13.3 million, is well above the previous upper guide of $12.2 million.

The share price has tracked the gains in revenue and earnings. The stock has more than doubled since the February/March market collapse, rising from $3.03 to $10.83 now.

Patrick Walravens, writing from JMP Securities, was impressed by Veritone’s new revenue guidance, and reiterated his Buy rating on the stock. In his comments, he said, “Veritone seems to be gaining traction in its Government, Legal, and Compliance verticals as it experienced record bookings in the quarter… we believe the company is moving its cost structure in the right direction with recent cost-reduction initiatives and upgrades…”

With his $17 price target, Walravens shows his own confidence that VERI will see 57% growth in the year ahead. (To watch Walravens’ track record, click here)

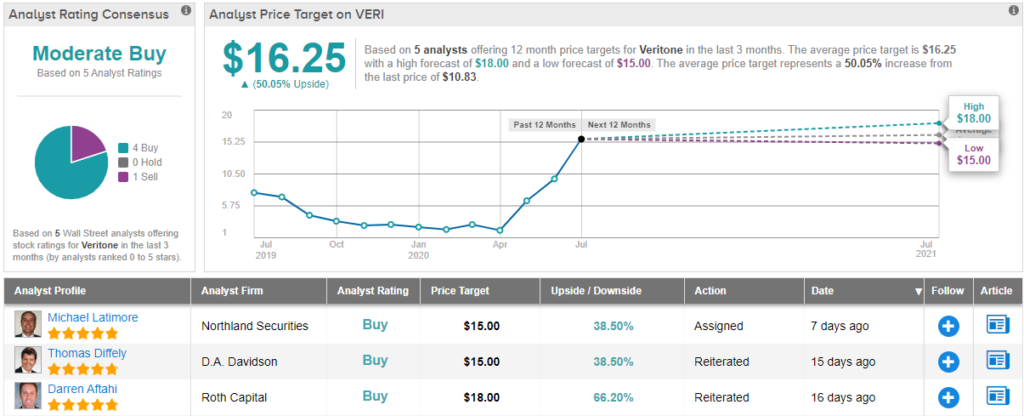

Overall, VERI’s Moderate Buy analyst consensus rating is based on 4 Buys and just a single Sell. The stock’s current price is $11.80, and the average price target $16.25 suggests it has a 50% upside potential. Note that even the low-ball target estimate, of $15, is well above the current price. (See Veritone stock analysis on TipRanks)

ZoomInfo Technologies (ZI)

Next up is ZoomInfo, a marketing tech company. ZI offers the usual features and services that customers expect in digital marketing intelligence, including account management, data management, demand generation, and lead prospecting. The company’s AI cloud software is specifically designed to improve efficiency in these tasks, letting sellers get to the business of selling.

ZoomInfo is a newly public company, having held its IPO just this past June. The opening was a success, with share prices almost doubling on the first day and nearly tripling in the first few trading sessions. Even now, after nearly two months during which the initial excitement waned and the glow came off the rose, the stock is still trading 88% above its initial price of $21.

The strong IPO prompted SunTrust Robinson analyst Terry Tillman – who is rated in the top 10 of the TipRanks analyst database – to initiate coverage of the stock with a Buy rating. Tillman wrote of ZoomInfo, “We believe ZoomInfo represents a rare combination of strong top-line growth and best-in-class profitability. Its go-to-market (GTM) sales intelligence platform drives positive outcomes for B2B sales and marketing organizations – increasing leads, customers and revenue. Premium valuation justified owing to accelerating demand for GTM intelligence and company-specific drivers leading to significant revenue and profit upside.”

Tillman’s Buy rating comes with a $60 price target, implying an impressive 51% upside potential. (To watch Tillman’s track record, click here)

ZoomInfo holds a Moderate Buy rating from the analyst consensus. This is based on 16 reviews, including 7 Buys and 9 Holds. The stock’s $55.07 average price target suggests it has room for 32% growth from the $41.66 trading price this year. (See ZoomInfo stock analysis on TipRanks)

CareDx (CDNA)

Last on today’s list is a tech company in the health care sector. CareDx develops and delivers diagnostic surveillance systems for heart transplant patients. The company’s AI-powered software monitors patient progress in real time, allowing both the patient and the doctors to respond to any rapidly changing health issues in time to ensure a more successful outcome. The result is a novel development in long-term care.

While CareDx’s products were originally designed to monitor heart transplants, the company has expanded. Its products now monitor most human organ transplants – including kidneys, an important niche, as the first successful organ transplant was conducted with a kidney, and this procedure is still among the most common of transplants. CareDx also has cloud-based AI systems to monitor lab results, and to connect digital implants with remote monitors.

The company’s earnings have proven mostly immune to recent economic instability, as medical transplant patients and doctors cannot simply stop using the monitoring systems. And with a firm user base, the stock recovered well from the late-winter market crash. CDNA is up over 130% since bottoming out in March.

Covering the stock for Piper Sandler, analyst Steven Mah wrote, “We believe CareDx has the broadest transplant care platform in the industry and we remain confident that it is well-positioned to protect and extend its first-mover advantage in both pre- and post-transplant patient management to drive long-term growth. In addition, we are encouraged by the resiliency of its essential tests and ability to operate in a COVID-19 environment.”

Mah gives CDNA a Buy rating, along with a $54 price target that implies an upside of 66% for the next 12 months. (To watch Mah’s track record, click here)

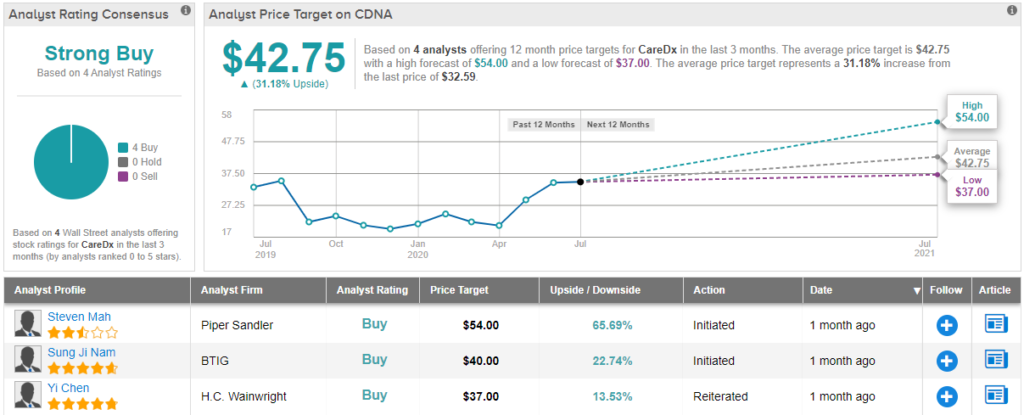

All in all, with 4 recent reviews on record, all Buys, CareDx has a unanimous Strong Buy rating from the analyst consensus. The stock is currently selling for $32.59, and the average price target, at $42.75, suggests a one-year upside of 31%. (See CareDx stock-price forecast on TipRanks)

To find good ideas for tech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.