Dividend stocks are the Swiss army knives of the stock market.

When dividend stocks go up, you make money. When they don’t go up — you still make money (from the dividend). Heck, even when a dividend stock goes down in price, it’s not all bad news, because the dividend yield (the absolute dividend amount, divided by the stock price) gets richer the more the stock falls in price.

Knowing all this, wouldn’t you like to own find great dividend stocks? Of course you would!

Using the TipRanks platform, we’ve looked up two stocks that are offering dividends of at least 10% yield – that’s more than 4x higher the average yield found in the markets today. Each of these is Strong Buy-rated, with some positive analyst reviews on record, and best of all, they all offer investors a low cost of entry, under $10 per share. Let’s take a closer look.

BrightSpire Capital (BRSP)

First up, BrightSpire Capital, is an internally managed real estate investment trust (REIT) focused on the commercial real estate market. The company holds a strong portfolio of properties, worth more than $5.3 billion and composed of 126 total investments in floating mortgage loans. The bulk of the portfolio, some 80%, is composed of multifamily dwellings or office space; 78% of the portfolio properties are located in the West or Southwest regions of the US.

In its last reported quarter, for 3Q22, BrightSpire showed a set of mixed results that nevertheless supported the strong dividend. The company’s bottom line was reported as a net loss, of $20.5 million – or a loss of 16 cents per share, attributable to common stockholders. At the same time, the company’s adjusted distributable earnings, which backs up the common share dividend payment, came to a total of $32.3 million, or 25 cents per common share. This went hand-in-hand with a positive net book value, by GAAP measures, of $10.87 per share.

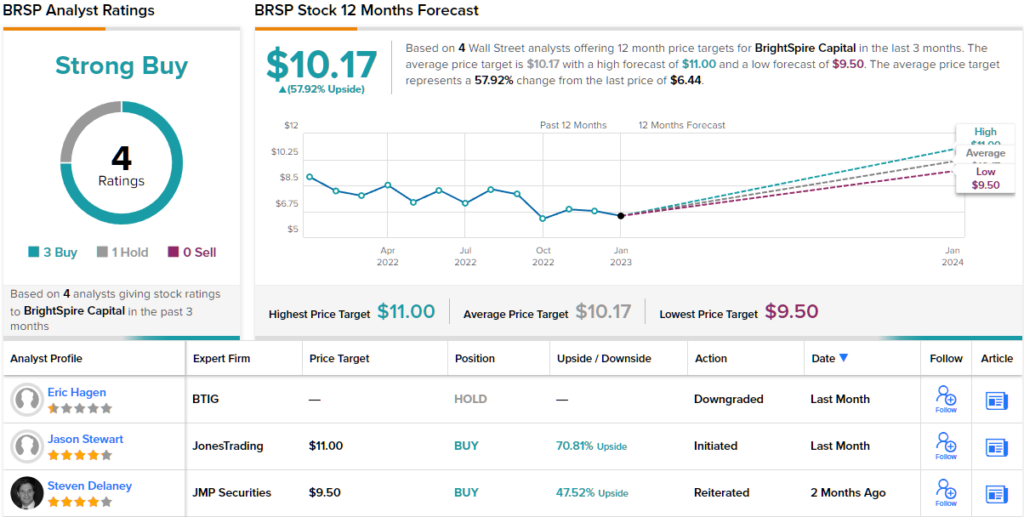

In mid-December, BrightSpire turned those ‘distributable earnings’ into a distribution to be paid this month, by announcing the Q4 dividend payment. At 20 cents per common share, the dividend is fully covered, and the annualized payment of 80 cents per share yields 12.4%.

Covering BrightSpire for Jones Research, analyst Jason Stewart sees plenty of potential for investors to grab onto. He writes, “The company has a scaled balance sheet, diverse origination platform and demonstrated ability to manage assets across sectors. The company’s portfolio is structured to benefit from increased short term rates (97% of loans are floating rate). The company is holding substantial liquidity and focused on asset management in the current uncertain macro-economic environment. As volatility subsides and the demand for commercial real estate credit improves, the company is in position to make opportunistic investments.”

Trading at 0.6x of book value per share (BVPS) and at a [12.4]% dividend yield, shares are substantially discounted to peers and below intrinsic value,” Stewart summed up.

In line with his bullish stance, Stewart rates BRSP a Buy, and his $11 price target implies room for ~70% upside potential in the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~82% potential total return profile. (To watch Stewart’s track record, click here)

Overall, there are 4 recent analyst reviews on record for BRSP shares and they break down to 3 Buys and 1 Hold, for a Strong Buy consensus view. The stock is selling for $6.44 and its $10.17 average price target suggests a gain of ~58% in the next 12 months. (See BRSP stock forecast on TipRanks)

Barings BDC, Inc. (BBDC)

The next high yield dividend stock is Barings BDC, a business development company, and part of the larger asset management firm Barings LLC, a $338 billion financial player. BBDC is one of the smaller components of the giant parent firm, with a portfolio of debt investments in the mid-market enterprise sector. Barings BDC’s investment portfolio was worth $2.33 billion at fair value, as of September 30, 2022, and the company had $2.64 billion in total assets.

This portfolio brought Barings BDC a total of $27.9 million in net investment income for Q3 of 2022, the last quarter reported. This income came to 26 cents per share. The company saw net realized gains of $7.9 million, or 7 cents per share, and the net assets gained from operations in Q3 was reported as $9.9 million, or 9 cents per share. The net gains, as positive values, were a strong turnaround from the losses recorded in 2Q22. The company has a net asset value per share (NAV) of $11.28 as of the end of 3Q22.

During this past December, BBDC paid out a quarterly cash dividend of 24 cents per common share. This annualizes to 96 cents, and gives a yield of 11.4%.

Barings BDC also uses an active share repurchase program to support the share value and return profits to shareholders. As of this past November, the company had bought back more than 2.26 million shares of its common stock, paying on average $9.69 per share.

5-star analyst Robert Dodd, of Raymond James, explains why Barings’ repurchase and dividend policies are right for investors – especially investors who intend to hold onto the stock into the longer-term. He writes, “Over the next several quarters, we do believe BBDC NII earnings power will exceed the dividend, and there could be some potential for incremental dividends. However, the company has also articulated plans for more share repurchases – such a use of capital is accretive to NAV/share and, in principle to NII and dividends long term.”

“Retaining earnings (though spillover) is doubly accretive to NAV: first by accruing to spillover ,which grows NAV, then by utilization to repurchase stock, which also grows NAV. In the short run, with many BDCs increasing dividends due to base rate upside, we do believe here may be some slight market disappointment in the BBDC approach. In the long-run however, we believe an NAV focus approach is likely to produce market outperformance,” Dodd continued.

Quantifying his stance for investors, Dodd goes on to give BBDC shares an Outperform (i.e. Buy) rating and $11 price target. If met, the figure could yield returns of ~31% over the one-year timeframe. (To watch Dodd’s track record, click here)

Overall, Wall Street tends to agree with the bull. The 4 recent analyst reviews include 3 Buys and 1 Hold, for a Strong Buy consensus rating, and the $10.25 average price target indicates a 28% upside potential from the current share price of $8.37. (See BBDC stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.