The hot war in Ukraine continues, pitting the smaller country’s stubborn resistance against Russia’s bigger battalions. The Western nations have responded with economic sanctions against Russia, the aggressor, and the sanctions have triggered higher volatility and sharp losses in global stock markets. On Wall Street, the S&P 500 is down 2.95% today, while the tech-heavy NASDAQ has fallen 3.6%. Year-to-date, the indexes are down 12% and 18%, respectively.

Despite these overall losses, investors can still find some strong buys in the markets – if they know which signals to follow. While the trends now are downward, some stocks are getting primed for forward gains, but those signs might not be clearly visible. Insiders will know what to look for – and fortunately for the retail investor, the insiders are required to publish their trading activity regularly.

These insiders are the company officers of the public firms. They hold high positions – as CEOs, as CFOs and COOs, as executive VPs, and as Board members – and those positions give them a clearer view of what’s ‘under the hood’ at their firms. At the same time, they are responsible for keeping those companies profitable, and Boards of Directors and shareholders can hold them to the fire. This means that corporate insiders don’t trade their own stock lightly – so we can follow their trades, for clues to forward performance.

We’ve done just that, using the Insiders’ Hot Stocks tool at TipRanks to find a couple of equities that the insiders are picking up. There are other positive signifiers to follow; these stocks are rated as Strong Buys by the analyst consensus and are projected to pick up steam in the months ahead. Let’s take a closer look.

AES Corporation (AES)

The first stock we’ll look at is AES Corporation, a leading power company. The Virginia-based firm employs more than 10,000 people around the world, and generates and distributes power in 15 countries. The company operates in the US, as well as South America, Europe, the Middle East, and Southeast Asia. In 2021, AES built or acquired over 2,000 megawatts of renewable power generation, and currently has a backlog of 9,239 megawatts under construction or contract through the year 2025.

In its most recent quarterly report, for 4Q21, AES showed $2.77 billion at the top line, up 8.2% from the year-ago revenue of $2.56 billion. On earnings, AES reported 45 cents per share in adjusted APS. This was down from the 48 cents reported one year ago, but slightly beat the forecast.

For the full year 2021, the company reported adjusted EPS of $1.52. This was at the low end of the original guidance range ($1.50 to $1.58), but higher than the 2020 earnings of $1.44 per share. Looking ahead, AES expects 2022 adjusted EPS to fall between $1.55 and $1.65 per share.

On the insider front, the company CFO Stephen Coughlin made a million-dollar purchase this month, picking up 47,000 shares at $21.30 each. This brings his full holding in the company to more than $1.4 million.

Covering AES for Morgan Stanley, 5-star analyst Stephen Byrd appreciates the company’s strong bent toward benefitting shareholders, writing: “We view management as being especially focused on enhancing shareholder value through a combination of attractive growth investments, monetizing assets with under-appreciated value, and becoming a pure-play ESG story through an aggressive decarbonization strategy that has resulted in significant, tangible reductions in fossil emissions.”

“AES is in our view the most attractive risk-adjusted play among our clean energy coverage universe driven by significant existing asset/business value which is now close to 100% of the stock price, one of the largest renewables/storage development businesses globally, and several positive catalysts,” Byrd added.

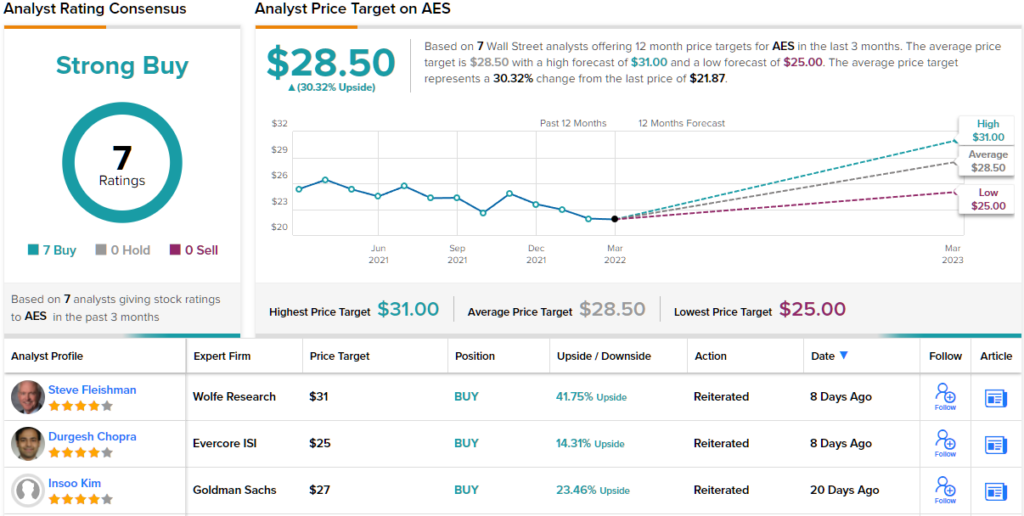

It’s not surprising, then, that Byrd gives AES shares an Overweight (i.e. Buy) rating, along with a $30.50 price target. This figure suggests room for ~39% upside in the next 12 months. (To watch Byrd’s track record, click here)

It’s clear from the unanimous Strong Buy consensus rating that Wall Street is in broad agreement on the bullish view here; 7 recent reviews all agree that this is a stock to Buy. The shares are priced at $21.87 and have an average price target of $28.50, implying ~30% one-year upside. (See AES stock analysis on TipRanks)

MiX Telematics (MIXT)

The second stock on our list is MiX Telematics, a major name in fleet management. Telematics is a technical term, for methods of monitoring cars, trucks, and other mobile assets through on-board diagnostics and/or GPS tech. MiX offers this type of fleet and mobile asset management, with offices in South Africa, the US, the UK, Australia, Mexico, Brazil, Uganda, and the UAE. The company’s worldwide network includes more than 130 fleet partners in more than 120 countries. MiX boasts over 790,000 service subscribers, and subscriptions make up 89% of the company’s revenue.

MiX’s fleet tracking services include reporting and live streams, and offers customers the ability to fine-tune vehicle fleet operations to improve fuel efficiency. The company can provide electronic logging devices, AI dashcams, journey management, and even a driver engagement app.

Last month, MiX reported its third quarter results for fiscal 2022. The company showed $36.2 million in total revenues, up 6.2% year-over-year, of which $30.3 million came from subscription services, a 4.3% y/y gain. Net subscribers grew by 20,300 during the quarter. MiX had $35.9 million in liquid assets at the end of the quarter.

Insider sentiment on MiX is positive, pushed that way by three recent ‘informative buys.’ The smallest of them was for $28,905, by EVP Catherine Lewis. A larger buy, of $280,385, was made by EVP Gert Pretorius, who bought over 1.2 million shares. The largest recent insider purchase came from Ian Jacobs, of the Board of Directors, who bought 2.5 million shares for $1.175 million.

Canaccord’s Michael Walkley is also a fan of MiX. The 5-star analyst rates the stock a Buy, along with a $22 price target, indicating confidence in a 91% upside going forward. (To watch Walkley’s track record, click here)

Walkley is optimistic about MiX’s forward prospects, and writes of the company: “MiX reported Q3/22 results better than our estimates on revenue, demonstrating its business trends continue to recover. With the impact of the global pandemic negatively impacting the oil & gas vertical combined with ongoing softness in the bus and coach industry, we believe the results demonstrate the business is starting to recover and expect steadily recovering subscription revenue growth trends through F2022 with stronger growth in F2023 and beyond. We believe the global opportunity for fleet management solutions remains strong longer term with low penetration levels, and we expect continued steady improvement in subscription growth and margins post the pandemic.”

Overall, MiX has picked up 3 recent reviews, all of which are positive – making the consensus a unanimous Strong Buy. Shares are selling for $11.52 and the $19 average price target implies ~65% upside in the coming year. (See MiX’s stock analysis at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.