ArcelorMittal (NYSE:MT) (GB:0RP9) is a global steel company headquartered in Luxembourg, Europe. The company produces various kinds of steel products and has some vertical integration with its iron ore mines in Brazil, Bosnia, Canada, Liberia, Mexico, South Africa, and Ukraine. I’m bullish on ArcelorMittal because of its historically low valuation, at 0.47x price-to-tangible-book value, and its ability to produce ample profits through the cycle.

ArcelorMittal’s Industry

Steelmaking is a capital-intensive business where demand often booms in expansions and wanes in recessions. Both the private sector and governments increase and decrease their spending on infrastructure. Some other steelmaking end markets are also quite cyclical, namely construction, manufacturing, automotive, military, aerospace, home appliances, bulk shipping, and energy generation (oil extraction, pipelines, windmills, etc.). Thus, ArcelorMittal is a cyclical company.

What Makes ArcelorMittal Unique?

Thankfully, ArcelorMittal has some diversification and advantages. The company isn’t too heavily reliant on any one country’s economy, it has numerous end markets, and it produces some of its own raw material through its iron ore mines. This makes ArcelorMittal anti-fragile compared to many of its competitors, for example, those who are reliant on one country, one industry, and one government’s steel tariffs.

In its 2023 annual report, the company discussed its geographic diversification, saying, “ArcelorMittal’s steel-making operations have a high degree of geographic diversification. In 2023, approximately 39% of its crude steel was produced in the Americas, approximately 50% was produced in Europe, and approximately 11% was produced in other countries, such as South Africa and Ukraine.”

This geographic diversification also gives the company exposure to fast-growing emerging markets like South America, India, Africa, the CIS (Commonwealth of Independent States), and Southeast Asia.

MT Stock: Trading at Half Its Tangible Book Value

Despite having a relatively strong balance sheet (net debt of just $3 billion, which isn’t much relative to its earnings potential), MT stock trades at just 0.47x its tangible book value (the value of the physical assets owned by the shareholders). For reference, this is close to what the company traded at during the Great Financial Crisis (GFC) of 2008. Recently, in 2018 and 2021, the company traded at 1x its tangible book value. Prior to the GFC, the company traded at 2-3x its tangible book value.

This low valuation seems unjustified, given the company’s ability to produce free cash flow and earnings through the cycle. The past decade wasn’t a particularly good one for steel companies, but ArcelorMittal still averaged $2.45 billion of net income. I think the company’s normalized earnings are higher than that. The money supply has grown substantially over the past decade, and ArcelorMittal’s returns on assets were substantially higher on average in the decade from 1998-2008.

The State of the Global Economy

If we look at the state of the global economy, steel demand has been falling in China, Europe has experienced 15 years of stagnation, and South America has been in turmoil for 15 years. Really, the only major economy that’s been booming has been the United States.

And the U.S. still has a long way to go in terms of improving its infrastructure and manufacturing capabilities, which will require more steel, in my opinion. While steel prices are currently healthy, it’s difficult to argue that the global economy is overheated.

The market seems to be pricing in a terrible recession for global steelmakers, but even if we get it, I think the next decade of steel production will be better than the last. The one glaring exception would be China, in my view, which seems to have dramatically overbuilt. Thankfully for the United States and some of ArcelorMittal’s other markets, tariffs are in place to prevent Chinese steelmakers from dumping product at low prices.

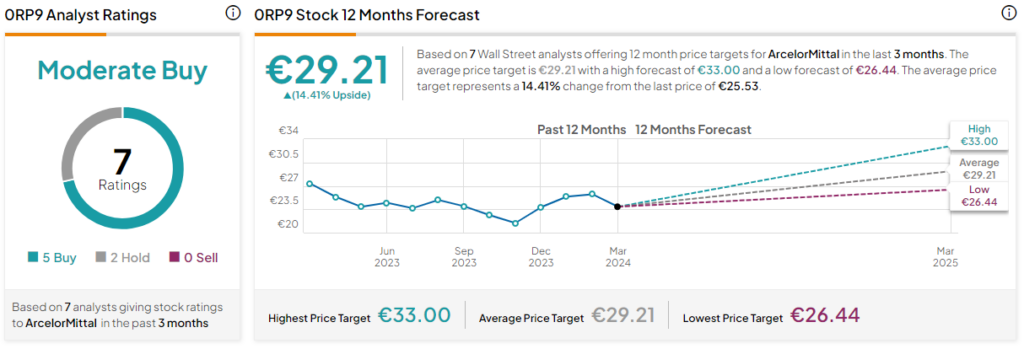

Is MT Stock a Buy, According to Analysts?

Currently, only one analyst covers the New York-listed MT shares. However, in Europe, five out of seven analysts covering MT give it a Buy rating, two rate it a Hold, and zero rate it a Sell, resulting in a Moderate Buy consensus rating.

The average ArcelorMittal stock price target for the shares listed in London is €29.21, implying upside potential of 14.4%. Analyst price targets range from a low of €26.44 per share to a high of €33 per share.

The Bottom Line on MT Stock

ArcelorMittal stock appears to be undervalued based on its valuation multiple relative to its tangible book value and average earnings. I think the company is anti-fragile, given its global diversification, relatively strong balance sheet, and integrated iron ore mines. The company has a definite growth opportunity with emerging economies like Southeast Asia, Africa, and South America.

The next decade could be better for this steelmaker. It has earned higher returns on its assets in the past, and two of its main markets (South America and Europe) have struggled economically since 2008. I think there’s definite turnaround potential for ArcelorMittal at 0.47x price-to-tangible-book value.