Are the Magnificent 7 tech stocks still magnificent? That’s the big question now for investors. These tech giants led the charge in last year’s stock market boom, but some are hitting roadblocks this year. While they nearly doubled the NASDAQ’s 54% growth in 2023, it appears that several of them have now topped out.

But it’s not the end of the road for the Mag 7. Rather, it serves as a reminder for investors to exercise caution and conduct thorough research before making any moves. These companies boast impressive advantages, from their dominant market positions to their deep financial reserves and stellar product offerings. There’s no denying why they rose to the top. And while some may be slowing down, others are still rising – suggesting there are still solid opportunities in the mega-cap tech sector.

Watching the tech giants for the investment research firm Maxim, Tom Forte, a 5-star analyst rated in the top 2% of the Street’s stock pros, has looked under the hood at both Amazon (NASDAQ:AMZN) and Apple (NASDAQ:AAPL), two of the Magnificent 7 names. His analysis leads to a clear conclusion on which of these shares is the superior stock to buy. Let’s delve deeper.

Amazon

We’ll start with Amazon, a company that wears several hats. It holds the title of the world’s largest online retailer and functions as a tech firm deeply immersed in AI, cloud computing, and online services. Furthermore, Amazon stands as a giant by many measures, boasting a market cap of $1.89 trillion.

Retail remains Amazon’s core business. The company can deliver most products to customers within one or two days. In support of this, Amazon has built a network of physical logistic centers, known as ‘fulfillment centers,’ capable of processing orders rapidly for global delivery. In calendar year 2023, the company achieved a total revenue of $574.8 billion.

Amazon may be the world’s leading e-commerce company, but that is not the whole story. The company has taken its online approach and applied it to a wide variety of customer services, including the cloud computing service AWS, and going on to home automation, ebooks, TV streaming, online gaming, and even grocery orders. On that last note, Amazon will soon be making its Dash Cart technology, currently online at Whole Foods and Amazon Fresh stores, available to select third-party grocery retailers.

Turning to AI, Amazon has made substantial investments in the generative AI firm Anthropic. The investments total $4 billion, and Anthropic, with Amazon’s backing, is working on generative AI technology. Amazon’s own Bedrock generative AI technology, a serverless platform, is being used by BrainBox in the development and launch of a virtual building assistant. These examples are just the tip of the iceberg; AI has become the next big deal in tech, and Amazon is making sure to position itself in the front row.

We’ll see Amazon’s next quarterly report, for 1Q24, at the end of this month; the Street is expecting to see $142.59 billion at the top line. Looking back at 4Q23, we find that Amazon reported $170 billion in quarterly revenue, for 14% year-over-year growth – and beating the expectations by $3.74 billion. The cloud computing segment, AWS, was a strong contributor to the total, with 13% y/y growth and a $24.2 billion share of the revenue total. International sales led the revenue growth, increasing by 17% year-over-year to reach $40.2 billion. The company reported net income of $10.6 billion, or $1 per share, at the bottom line.

Analyst Forte notes that Amazon has, in recent years, been following the vision of a new CEO – and that this path is proving successful. He writes of the company, “Since becoming CEO in July 2021, CEO, President, and Director Andy Jassy has done a remarkable job of developing and implementing his vision for the future… Collectively, Mr. Jassy’s emphasis on services and improving margins could result in a re-rating for its stock. It already trades at a meaningful P/E premium versus its big-tech peers. The big opportunities are to close the gap on its peers on an EV/Sales and EV/EBITDA basis, were it trades at significant discounts. With an increasing amount of sales derived from higher-margin services and less from lower-margin retail sales (including, potentially, from de-emphasizing grocery) this could enable the company to chip away at those large valuation gaps.”

Summing up, Forte comes down to a bullish statement: “For our part, we are valuing the company at 17.5x EV/EBITDA (compared with its current 15.0 multiple) on the expectation it will close the gap against its big-tech peers (26.7x average) by adding incremental revenue at higher margins.”

To this end, Forte rates AMZN shares a Buy, and his $218 price target implies a potential upside of 20% on the one-year time horizon. (To watch Forte’s track record, click here)

Overall, there are 41 recent analyst reviews of Amazon stock on file, and they are unanimous – this is a Strong Buy stock. The shares are priced at $181.28, and the $212.21 average price target suggests the stock has a one-year upside potential of 17%. (See AMZN stock forecast)

Apple

Next up is Apple, another of the Magnificent 7 tech mega-caps, and the second-largest publicly traded firm on Wall Street. Apple was the first publicly traded company to reach the trillion-dollar market cap mark, the first to reach two trillion, and then the first to reach three trillion. The stock has had its ups and downs, and the company currently boasts a market cap of $2.61 trillion. In the company’s fiscal year 2023, which ended last September, Apple saw a total of $383 billion in revenue and registered a net income of almost $97 billion.

Apple earned its success, its perch at the pinnacle of the tech world, through the development, production, and marketing of ‘stuff that people like.’ From the company’s early PCs, to its development of the Mac line of computers, and later to its iPhones and iPads, Apple has excelled in putting high-end tech products on the market, with a winning combination of style and function.

Recently, however, Apple has been facing some headwinds. The company has become highly dependent on its iPhone sales; this was clear in the financial statement for fiscal 1Q24, which showed the iPhone segment making up more than 58% of the company’s total net sales.

The high dependence on the iPhone line would likely be less of a problem than it is if Apple weren’t also becoming highly dependent on China as both a supplier and a market. The company sources a large percentage of its parts and components from China, and weakening Chinese demand for smartphones has also been putting pressure on Apple. The company saw a decline in Chinese sales earlier this year, as much as 24%, according to some industry reports. Apple’s fiscal 1Q24 reports showed that the company’s overall sales in China slowed by almost 13% during the quarter. We should note here that Apple’s Chinese sales made up more than 17% of the company’s total revenue during Q1.

Zooming out a bit, we find that Apple reported $119.6 billion at the top line in fiscal 1Q24. Despite the headwinds, this was up a modest 2% year-over-year and came in $1.34 billion over the forecast. The company’s $2.18 EPS was 7 cents better than expected. The various worries have taken root with investors, though, and AAPL shares are down ~13% year-to-date.

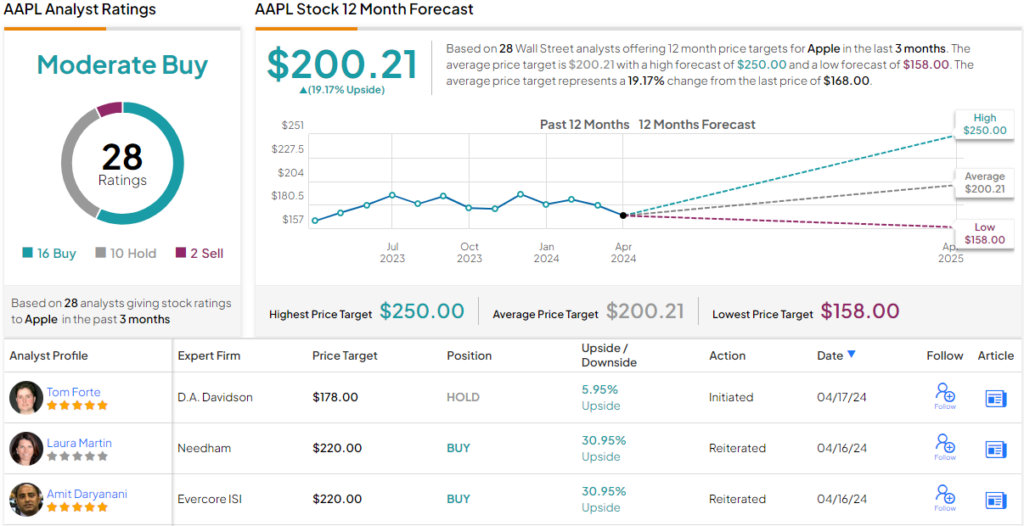

Top analyst Tom Forte, in his coverage of Apple, acknowledges the company’s strengths but sees the current conditions as less than propitious, saying, “Challenges that limit upside, in our view are: 1) Apple is too dependent on China, from a sales (18.9% in FY23) and supply-chain standpoint; 2) it is overweight a single product, the iPhone, when it comes to its near-term operating results (52.3% in FY23); 3) we are monitoring a list of items that could also contribute to a prolonged dead-money period for the stock, including antitrust/regulation, a demand imbalance for consumer electronics, and competition.”

To this end, Forte rates Apple shares a Hold, along with a $178 price target, suggesting a modest upside of 6% for this year.

Overall, Apple gets a Moderate Buy rating from the Street, a view based on 28 recommendations that include 16 Buy recommendations, 10 Holds, and 2 Sells. Apple stock is currently trading at $168 and its $200.21 average price target points toward a one-year gain of 19%. (See Apple stock forecast)

After looking into the data, and considering the analyst’s positions, it’s clear that Maxim’s Tom Forte sees Amazon as the better Magnificent 7 stock to buy right now.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.