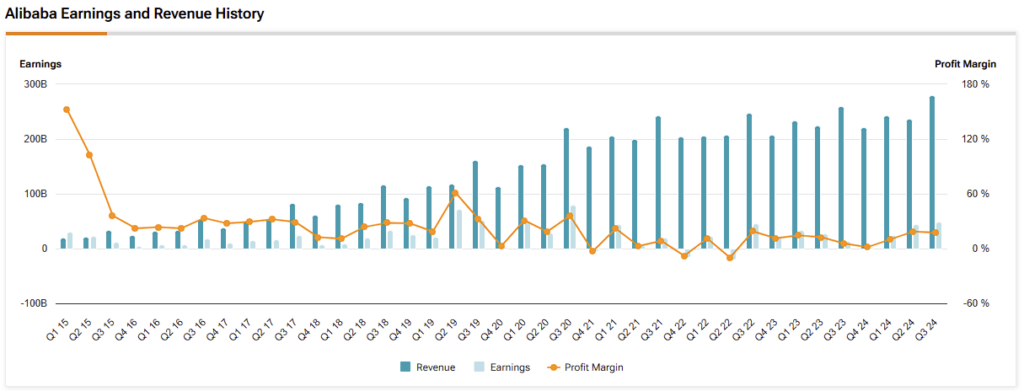

Alibaba Group (BABA) shares dropped following its Q4 and full-year fiscal 2025 results, but the market’s quick reaction masks the company’s strong year-end momentum driven by booming cloud growth, solid e-commerce performance, and triple-digit AI product gains. Despite the pullback, BABA remains attractively valued and supports hefty share buybacks, leaving me quite bullish on its future prospects.

Protect Your Portfolio Against Market Uncertainty

- Discover companies with rock-solid fundamentals in TipRanks' Smart Value Newsletter.

- Receive undervalued stocks, resilient to market uncertainty, delivered straight to your inbox.

Cloud Business Soars with AI Demand

One of the clear standouts in Alibaba’s report was its Cloud Intelligence Group, which grew revenue by 18% year-over-year to $4.2 billion. The surge was driven primarily by public cloud adoption and the rapid expansion of AI use cases. Importantly, Alibaba saw broad-based demand not just from internet-native sectors like autonomous driving and online education, but also from more traditional industries such as manufacturing and animal farming, which are now migrating workloads to the cloud in order to deploy AI tools.

The momentum is translating into real profitability. Adjusted EBITA for the Cloud segment rose 69% year-over-year, boosted by a shift toward high-margin services and greater operating efficiency. Alibaba is clearly doubling down on this trend. In April, it launched the Qwen3 model family, featuring both dense and Mixture-of-Experts architectures, optimized for enterprise use cases.

With over 300 million downloads and more than 100,000 derivative models globally, Qwen has become the world’s largest open-source model ecosystem. Combined with enterprise adoption of GPU leasing and tools like PolarDB (now used by ICBC), Alibaba’s cloud-AI flywheel looks primed to spin faster from here.

E-Commerce Stays Resilient

On the e-commerce front, Alibaba continued proving its strength in domestic and international markets. Taobao and Tmall, its core commerce platforms, posted 12% year-over-year growth in customer management revenue (CMR), a key indicator of monetization and advertiser demand. According to some of management’s comments made during the earnings call, the 11.11 Global Shopping Festival supported record monthly active users, while merchant tools like platform coupons and Quanzhantui helped drive improved inventory turnover and ad efficiency.

Alibaba’s membership ecosystem is also deepening. The number of 88VIP members, which comprises its highest-spending consumer tier, rose by double digits year-over-year, surpassing 50 million. With improved user experience and engagement features, this group is now contributing higher ARPU on a cohort basis, providing a sticky and increasingly profitable user base.

Internationally, the Alibaba International Digital Commerce Group (AIDC) saw revenue jump 22% to $4.6 billion, led by strong performance from cross-border segments like AliExpress and Trendyol. The company continues to focus on enhancing operating efficiency and diversifying its regional playbook. For instance, the AliExpress Choice program is seeing improved unit economics, while localized merchant tools are driving better platform monetization in key markets across Europe and the Gulf.

A Bargain Stock with Shareholder Love

Following its post-earnings pullback, BABA now trades at just 12x forward earnings, which makes it an attractive entry point for a business posting consistent top-line growth and strengthening margins across key verticals. Backing that up is a fortress balance sheet with $24.8 billion in net cash, giving the company flexibility to invest in growth while returning capital to shareholders.

In particular, during the year, Alibaba repurchased $11.9 billion worth of shares, cutting its outstanding share count by 5.1%. Another $22 billion remains authorized for buybacks. Notably, Alibaba has already retired about 16.3% of its outstanding shares since early 2022, when aggressive repurchases started taking place.

For the first time, the company will pay a two-part dividend totaling $2 per ADS—$1.05 as a regular annual dividend and $0.95 as a special dividend funded by the sale of non-core assets like Sun Art and Intime. Combined, the $4.6 billion in payouts highlights a shareholder-friendly posture that investors should appreciate.

Is Alibaba Stock a Buy Right Now?

Despite the stock’s post-earnings sell-off, Wall Street appears very optimistic about Alibaba. BABA stock retains a Strong Buy consensus rating, with 16 analysts unanimously rating the stock a buy. Not a single analyst is neutral or bearish. Alibaba’s average stock price target of $167 indicates an upside potential of ~33% over the coming twelve months.

BABA Eyes Long-Term Growth Despite Short-Term Volatility

Despite the recent dip in its stock, Alibaba’s fundamentals have never been stronger. Cloud and AI drive significant revenue and profits, while e-commerce remains steady with new monetization tools gaining traction.

The open-sourcing of Qwen3 gives Alibaba a strategic edge in an emerging space. With substantial ongoing capital returns, Alibaba presents a compelling investment opportunity as it heads into FY2026 with strong momentum. However, patience is key, as the stock has historically faced prolonged periods of pressure—this is a long-term value play, not a quick win.