WeWork (NYSE:WE) stock declined nearly 17% in pre-market trading as of the last check after the company cited “substantial doubt” over its future survival. WeWork, which is backed by Japanese firm SoftBank, provides coworking spaces, including physical and virtual shared spaces. The company reported its second quarter Fiscal 2023 results on August 8, after the market closed. WE shares have lost 85% so far in 2023.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Here’s Why WeWork Doubts Its Survival

WeWork warned of its continuity as a “going concern” should the company not be able to mitigate the current headwinds. The company is facing increased member churn, excess supply of commercial real estate, heated competition in the flexible office space, and concerns stemming from macroeconomic uncertainties. The company stated that these factors collectively have resulted in a “slight decline” in memberships.

Additionally, WeWork is burdened with liquidity issues caused by growing company losses and projected cash needs. If the company can improve its finances and profitability by the next year, WeWork might still have a chance to continue as an operational entity.

To meet its obligations, WeWork is faced with a multitude of tasks. The company needs to renegotiate its lease terms favorably as well as boost revenue by increasing new sales and retaining existing members. Plus, the company will need to control costs and limit capital expenditures, while also raising additional capital via debt/equity issuance and asset sales.

Details of WeWork’s Q2FY23 Results

WeWork reported a diluted loss of $0.21 per share, worse than analysts’ expected loss of $0.12 per share. Meanwhile, quarterly revenue came in at $844 million, up 3.6% year-over-year but lower than the consensus of $850.15 million.

WeWork’s physical occupancy for the quarter stood at 72%, marking an improvement over the prior-year quarter’s occupancy of 70% but 1% lower than Q1’s occupancy.

As of the quarter’s end, WeWork’s consolidated real estate portfolio equated to 610 locations across 33 countries. Meanwhile, physical memberships fell 3% year-over-year to 512,000. Even so, average revenue per physical member increased by 4% to $502 in Q2.

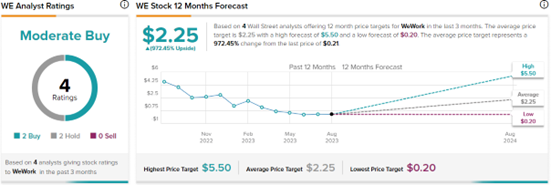

Is it Good to Buy WeWork Stock?

Analysts and the company itself have grave concerns regarding WeWork’s stock trajectory. On TipRanks, WE stock has a Moderate Buy consensus rating based on two Buys versus two Hold ratings.

These ratings were given before the Q2 print and related cautionary statements by the company. The analyst’s views are subject to change following the news. The current average WeWork price target of $2.25 implies 972.5% upside potential from current levels.