Weingarten Realty Investors delivered better-than-expected results in the fourth-quarter and announced a dividend hike for its shareholders. Shares of the real estate investment trust company closed 3.7% higher on Feb. 22.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Weingarten Realty’s (WRI) 4Q revenues declined 6.2% to $112.1 million year-over-year, but topped the Street’s estimates of $106.2 million. The company’s earnings plunged about 69% year-over-year to $0.18 per share, but exceeded the consensus estimates of $0.10 per share.

Weingarten Realty’s core funds from operations (FFO) dropped to $0.43 per share from the $0.53 per share posted during the same period a year ago. The company said that the decline in FFO was due to “reduced revenue from tenants converted to cash basis accounting, fallouts, abatements and higher bad debt expense/uncollectible revenue.”

Cash collections of rent and billable expense recoveries totalled 94% in 4Q, an improvement from 93% in 3Q, reflecting the company’s “transformed portfolio of quality properties.”

During the quarter, the company announced a 66.7% hike in its quarterly dividend to $0.30 per share from $0.18. The new quarterly dividend will be paid on March 16 to shareholders of record as of March 9. The annual dividend of $1.2 per share now reflects a dividend yield of 4.6%.

Weingarten Realty’s CEO Drew Alexander said, “Uncertainty remains, but solid cash collection metrics, a very stable base of essential tenants and the acceleration of leasing activity makes us cautiously optimistic about 2021.” (See Weingarten Realty stock analysis on TipRanks).

As for 2021, the company expects earnings in the range of $0.68-$0.81 per share and core FFO in the range of $1.65-$1.75 per share. Analysts were looking for FFO of $1.76 per share.

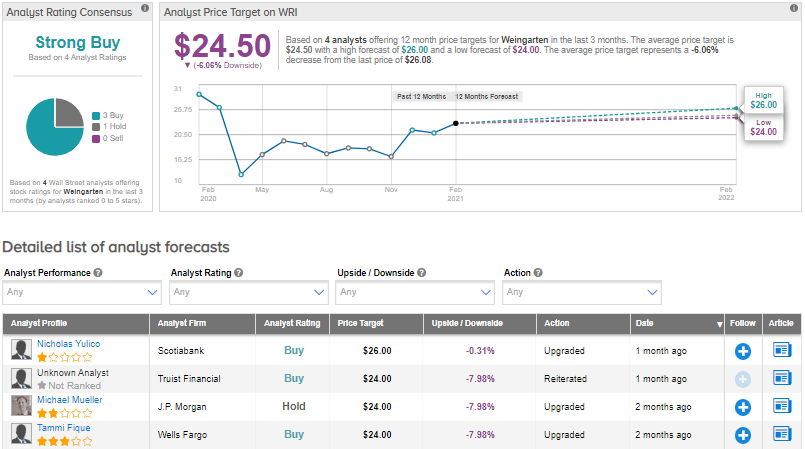

Earlier on Dec. 10, Wells Fargo analyst Tammi Fique upgraded the stock to Buy from Hold and lifted the stock’s price target to $24 (about 8% downside potential) from $19, citing the company’s valuations and fundamentals.

Overall, the rest of the Street has a bullish outlook on the stock, with a Strong Buy consensus rating based on 3 Buys and 1 Hold. The average analyst price target of $24.50 implies downside potential of about 6.1% to current levels. Shares have declined by about 11.1% over the past year.

Related News:

Palo Alto Drops Pre-Market On Dim 3Q Profit Outlook; Street Says Buy

Ingersoll Rand Gains On 4Q Earnings Beat; Street Sees 23% Upside

Kimco Realty Shores Up Dividend By 6.3%; Street Is Bullish