It’s hard to stand by Warner Bros. Discovery (NASDAQ:WBD) as the company’s shares continue to lose value month after month. Maybe you’re in the mood to be a hero and buy some seemingly cheap shares, but please be careful. I am neutral on WBD stock because Warner Bros. Discovery’s recently posted results weren’t all bad, but there are some red flags to be aware of.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Warner Bros. Discovery is a media and entertainment giant that provides a variety of content, including streaming content. It’s an increasingly crowded market, and Warner Bros. Discovery has to compete against Netflix (NASDAQ:NFLX) and Walt Disney (NYSE:DIS), among others.

That’s a tall order, and the investing community doesn’t seem convinced that Warner Bros. Discovery can withstand the competition. Yet, the proof is in the pudding, as they say, so let’s delve into Warner Bros. Discovery’s data and see if there’s a bullish argument in favor of WBD stock.

Cost Cutting Is “Not a Strategy” for Warner Bros. Discovery

First, I’ll start off with a positive point from Warner Bros. Discovery’s fourth-quarter 2023 financial results. Specifically, the company managed to reduce its costs of revenues (excluding depreciation and amortization) from $6.954 billion in 2022’s fourth quarter to $5.896 billion in Q4 2023.

In other words, it appears that Warner Bros. Discovery successfully cut its costs on a year-over-year basis. That’s commendable, but should this convince anyone to buy WBD stock now?

LightShed Partners analyst Rich Greenfield doesn’t seem to think so. He delivered some tough talk concerning Warner Bros. Discovery’s management, saying, “It’s hard to pay meaningfully for a company if they do not believe that there is future revenue and earnings growth.”

What about Warner Bros. Discovery’s apparently successful cost-reduction efforts, though? In response to this, Greenfield doesn’t seem too impressed. He contended, “You can cut and certainly generate cash on the short-term, but cost cutting is not a long-term strategy.”

I tend to concur with what Greenfield is saying here. Warner Bros. Discovery needs to generate robust revenue and not just reduce its expenditures. So, did the company rake in enough quarterly revenue to impress investors today?

Warner Bros. Discovery Swings and Misses

The answer is no, unfortunately. Warner Bros. Discovery generated $10.284 billion in Q4-2023 revenue, down from $11.008 billion in the year-earlier quarter. This result also fell short of Wall Street’s call for $10.34 billion in revenue.

Turning to the bottom-line results, there’s a good-news-and-bad-news situation. The good news is that Warner Bros. Discovery’s net loss “available to” the company narrowed from $2.101 billion ($0.86 per share) in Q4 2022 to $400 million ($0.16 per share) in 2023’s fourth quarter.

The bad news, however, is that analysts had expected Warner Bros. Discovery to narrow its loss to $0.11 per share. Hence, Warner Bros. Discovery missed Wall Street’s top-line and bottom-line consensus estimates.

In its earnings report, Warner Bros. Discovery pointed out some problematic data points. On a year-over-year basis, the company’s “Content revenue decreased 20% ex-FX” in Q4 2023. Moreover, Warner Bros. Discovery’s “Studios revenues decreased 18% ex-FX.”

If you really want to step back and look at the big picture, check out Warner Bros. Discovery’s quarterly EPS track record. The company now has three consecutive quarterly EPS misses when compared to Wall Street’s consensus estimates. Besides, Warner Bros. Discovery has had more EPS misses than beats and more unprofitable quarters than profitable ones during the past couple of years.

For what it’s worth, Warner Bros. Discovery President and CEO David Zaslav claims to have an “attack plan for 2024.” This includes “the roll-out of Max in key international markets, a more robust creative pipeline across our film and TV studios, and further progress against our long-range financial goals.”

That’s all fine and well, but today’s stock traders evidently weren’t impressed with Zaslav’s “attack plan.” They sent Warner Bros. Discovery stock down about 10% today as an expression of their discontent with the company.

Is WBD Stock a Buy, According to Analysts?

On TipRanks, WBD comes in as a Moderate Buy based on five Buys, five Holds, and one Sell rating assigned by analysts in the past three months. The average Warner Bros. Discovery price target is $13.94, implying 61.9% upside potential.

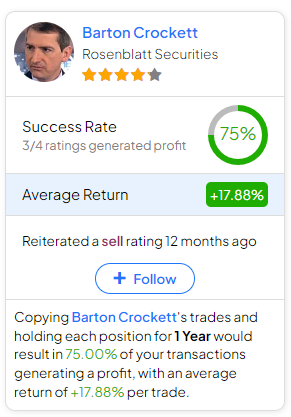

If you’re wondering which analyst you should follow if you want to buy and sell WBD stock, the most accurate analyst covering the stock (on a one-year timeframe) is Barton Crockett of Rosenblatt Securities, with an average return of 17.88% per rating and a 75% success rate. Click on the image below to learn more.

Conclusion: Should You Consider WBD Stock?

Maybe Zaslav’s “attack plan” will help Warner Bros. Discovery turn a corner in 2024. This remains to be seen, though. For now, investors should weigh Warner Bros. Discovery’s actual results, which haven’t been stellar.

To put it another way, Warner Bros. Discovery remains a “show-me” story until the company improves its earnings track record. Therefore, while the situation isn’t hopeless, I’m staying neutral on WBD stock and am not currently considering a share position.