Shares of United States Steel rose 4.9% on Sept. 18 as the company announced a better-than-anticipated outlook for the third quarter backed by improved business in recent months.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

United States Steel (X) stated that it expects 3Q adjusted EBITDA loss of $100 million and adjusted loss per share of $1.45. Analysts were expecting a loss per share of $1.52.

CEO David B. Burritt commented, “Improving market conditions experienced in June and July have accelerated through August and September. Strengthening steel fundamentals and our ability to respond quickly to increasing customer demand are expected to result in significantly improved adjusted EBITDA in the third quarter.”

The CEO is optimistic about the recovery that is underway in North America and Europe. Given the improved conditions, the company intends to repay about $900 million of its US ABL or asset-backed loans by the end of the quarter.

Meanwhile, U.S. Steel expects its Flat-rolled segment results to be negative in 3Q, but significantly better than 2Q. In response to an improving order book, the company restarted three blast furnaces that were temporarily idled earlier this year due to the pandemic. Currently, it expects two blast furnaces to remain temporarily idled through year-end.

The company is also experiencing improvement in its European business and says that market conditions for its Tubular business appear to have bottomed out.

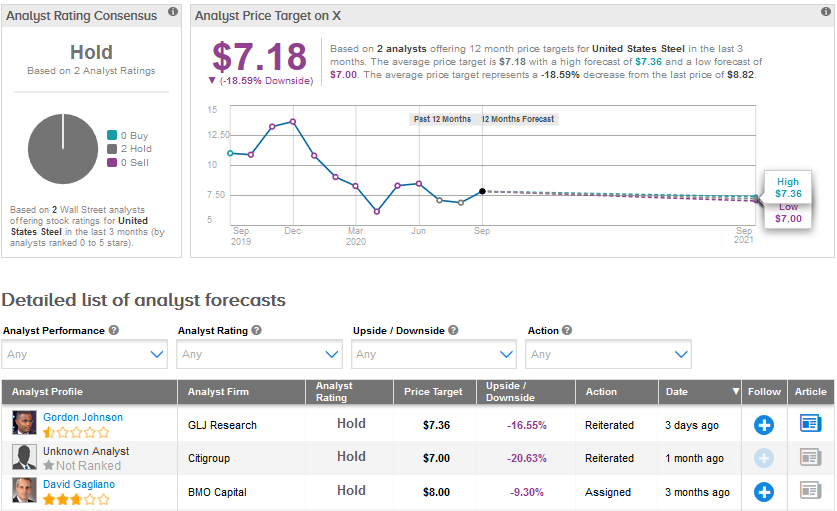

Prior to the 3Q business update, GLJ Research analyst Gordon Johnson lowered the price target to $7.36 from $13 for U.S. Steel while maintaining a Hold rating. The analyst said that U.S. steel mills have “had a few things turn in their favor” in the last few months and he sees mills being able to hike prices ahead of contract negotiation season.

While this means on a tactical level that the company’s share price could move higher in the near-term, the analyst thinks “competitive disadvantages ultimately prevail beginning late this year.” The analyst also feels that U.S. Steel has a structurally higher cost base than its peers and an over-levered balance sheet. (See X stock analysis on TipRanks)

U.S. Steel stock has declined 22.6% year-to-date and there might not be much respite for investors as the average analyst price target of $7.18 implies that a further downside of about 19% lies ahead. The stock has a Hold consensus based on two recent Hold ratings.

Related News:

Delta Upsizes Loyalty Program-Backed Debt Deal To $9B

Roku Inks NBCUniversal Deal For Peacock App, Ending Dispute

Barrick Gold Accepts Chilean Court Ruling On Pascua-Lama Project