Shares of work marketplace Upwork Inc. (UPWK) sank nearly 18% yesterday despite a robust second quarter showing as weakening metrics weighed on investor sentiment.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The stock is down about 43.8% so far this year even as the gig economy continues to gain traction.

Robust Q2 But Softening Metrics

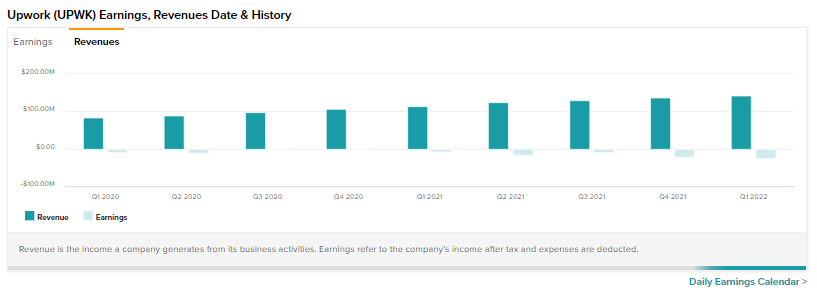

During the quarter, revenue rose 26.3% to $156.9 million, beating estimates by $7.7 million. The net loss per share at $0.04 came in narrower than the anticipated $0.04 per share. In the year-ago period, the company posted earnings of $0.03 per share versus the Street’s consensus of a net loss per share of $0.04. Additionally, the pace of top-line expansion has slowed as compared to Q2 2021.

Nonetheless, Upwork continues to gain traction. Gross service volume (GSV), at around $1 billion, grew 19% year-over-year. It signed 36 new enterprise clients in Q2, a 13% sequential growth, and expanded Enterprise revenue by 45% over the prior year period. In Q2 2021, enterprise revenue growth was 88%.

The number of active clients with the company has increased to 807,000 from 725,000 a year ago, but the pace of new additions has dropped to 11% from the year-ago figure of 27%.

Finally, the company upped its full-year 2022 top-line guidance, expecting it to be between $612 million and $617 million. This represents a 22% growth over the prior year at the midpoint. A net loss per share is anticipated to be between $0.15 and $0.17.

Website Visits Hinted at the Softening Metrics

This softening in user metrics despite the uptick in revenue could also be gleaned from the TipRanks website traffic tool. The data shows the increase in the number of total visits to the Upwork website globally increased by only 4.45% in Q2 to 71.95 million. In comparison, the number of visits had jumped by 25.78% to 68.89 million in the prior quarter.

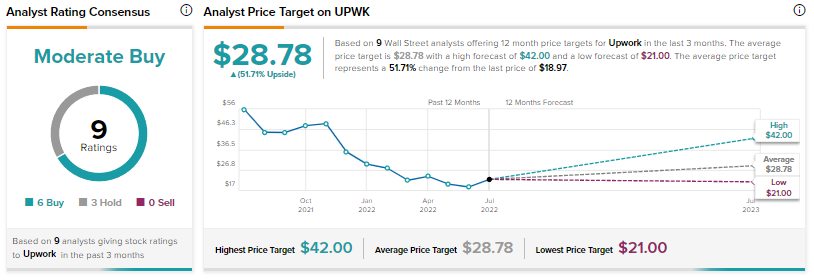

Analysts’ Take on UPWK

RBC Capital’s Brad Erickson has reiterated a Hold rating on the stock and noted that while long-term growth remains buoyant, more insight is needed over margin gains and facing up to competitive pressure from LinkedIn before taking a favorable standpoint. LinkedIn has forayed into the work marketplace and its standing as a numero uno social network for professionals already provides the platform a strong edge.

Amid this softening in metrics, Wall Street is cautiously optimistic about Upwork with a Moderate Buy consensus rating and an average price target of $28.78. This still implies a substantial potential upside of 51.71% for Upwork.

Closing Note

Upwork continues to steadily make gains as the broader trend towards a gig economy continues unabated. More green shoots on unit metrics and an ability to withstand the presence of LinkedIn may be needed before its shares start moving northwards again.

Read full Disclosure