Tesla stock (NASDAQ:TSLA) notches higher after Morgan Stanley, in a recent analysis, speculated about Tesla’s potential to be a major player in the future of electric vehicle (EV) charging. By opening up its Supercharger network to other automakers and utilizing its renewable energy and storage capabilities, Tesla could be a major contender in the electric filling station industry. Analyst Adam Jonas and his team contemplated a scenario where Tesla generates its own electricity at a nearly zero marginal cost, stored onsite with stationary batteries. They played with broad estimates, such as 8% of all U.S. miles driven being electric by 2030 and a Supercharging market share of 20%. Other factors included a 4 miles/KWh efficiency and revenue charged at $0.32/KWh. By discounting projected net operating profits after tax at a 9.0% weighted average cost of capital, they estimated the value of Tesla’s charging business.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

In Morgan Stanley’s world of ‘what ifs,’ they imagine several cases. The ‘reasonable case’ plots a path with 10% of miles being EV, Tesla holding half of the Supercharging market, and enjoying a 30% net operating profit. This scenario pegs the value at $3 per share. Next up, the ‘plausible case’ imagines 20% EV miles, Tesla reigning with 70% of Supercharging and a heftier 50% net profit. Here, the stakes rise to $14 per share. In the ‘dominant case,’ Tesla rules the road with 30% of EV miles and 80% Supercharging market share. The net profit swells to 70%, making the share value $33. Finally, in the ‘monopoly case’ where Tesla is the undisputed king with half of the EV miles and the entire Supercharging market, the net profit could hit a stellar 80%, skyrocketing the share value to $78.

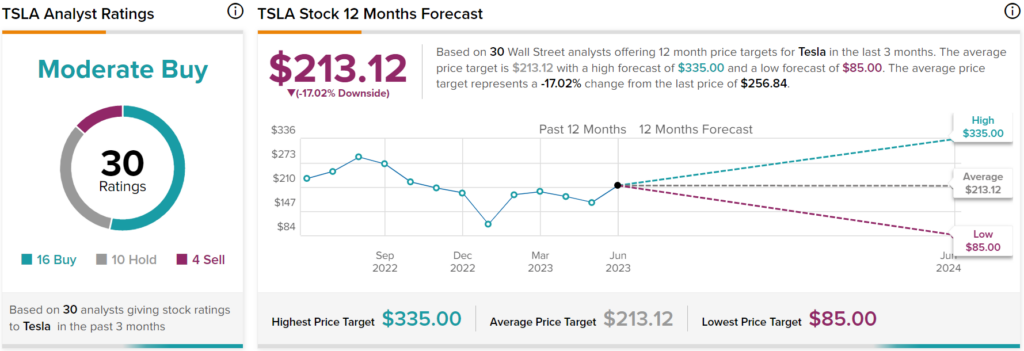

Overall, analysts have a Moderate Buy consensus rating on TSLA stock based on 16 Buys, 10 Holds, and four Sells assigned in the past three months, as indicated by the graphic above. Nevertheless, the average price target of $213.12 per share implies 17.02% downside potential.