With markets hitting new highs and stock prices going up, up, up – value investors are seeking companies that have flown under the radar. Down 45% in the past year, Titan Machinery (NASDAQ:TITN) stock is one such opportunity. After embarking on an ambitious acquisition spree, the company is poised for strong growth, provided it can achieve greater operational efficiency. It is a compelling value play that warrants investors’ attention.

Titanic M&A Growth

Titan Machinery owns and operates a network of full-service agricultural and construction equipment stores across the United States and Europe. The firm offers new and used equipment, largely from the CNH Industrial family of brands, along with products from other manufacturers.

Over the past two years, Titan Machinery has strategically expanded its revenue stream through seven significant acquisitions, amassing approximately $670 million in annualized revenue. While integrating these acquisitions is a complex task, it holds immense potential for the company’s future. These acquisitions are currently impacting the company’s operating expenses. That said, if the company can successfully integrate these new assets and reallocate resources to ensure operational efficiency, it could pave the way for robust financial results in the future.

The industry has been experiencing consistent growth, which is expected to continue through 2024, despite companies in this space still grappling with supply chain disruptions, inventory shortages, and persisting talent shortages in both high- and low-skilled positions.

Recent Results

Titan Machinery’s most recent earnings report for Q3 FY2024 offered a mixed bag. Revenue increased 3.78% to $694.1 million but missed analysts’ estimates of $727.2 million. Earnings per share (EPS) of $1.32 declined 27.47% year-over-year and missed expectations of $1.53.

The bottom line was impacted by an 8% rise in operating expenses to $92.1 million. This growth was predominantly driven by the company’s strategic acquisitions over the past year and a rise in variable costs related to increased sales performance.

Street estimates for the upcoming quarter are EPS of $1.02 on revenue of $734.99 million.

Value or Value Trap?

TITN stock has been trending down over the past year. It trades towards the lower end of its 52-week range of $21.44-$47.87, and below the 20-day and 50-day moving averages of $25.94 and $26.38, demonstrating negative price momentum.

However, from a valuation perspective, the price decline has driven the stock into deep value territory. The P/E of 5.5x is well below sector (Industrials) and industry (Industrial Distribution) averages of 17.8x and 23.7x, respectively. The same pattern can be seen across the other relative value metrics and enterprise ratios (like P/S, P/B, and EV/EBITDA).

In general, the challenge with value stocks is they trade at a discount to fair value for a reason. There is something the market does like about them. You can buy a value stock only to watch it get even cheaper (and then go out of business). TITN could continue to decline or bump along sideways from here, or the company could successfully execute on integrating its acquisitions, making this a prime entry point for a longer-term value stock.

Is TITN a Buy, Hold, or Sell?

Analysts covering the stock have been bullish, citing the upside potential of achieving operational efficiencies and greater scale. However, based on industry trends, they have tempered their near-term expectations.

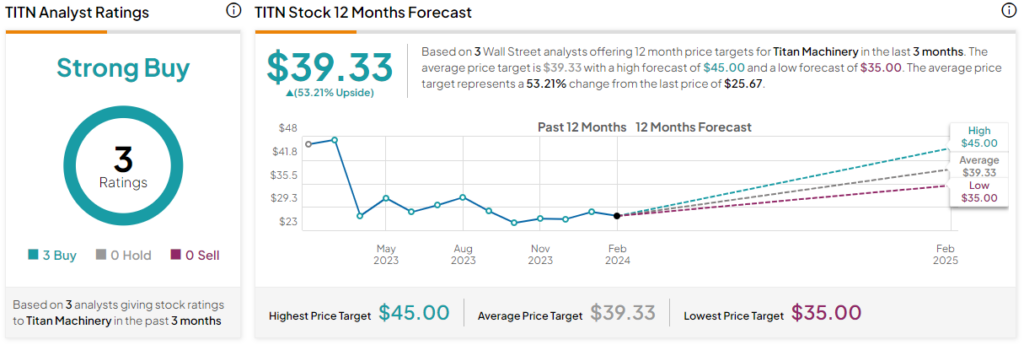

TipRanks lists TITN as a Strong Buy based on three Buy ratings in the past three months. The average price target for Titan Machinery stock is $39.33, with a range of $35-$45. This price target represents a 53.21% upside from current levels.

Bottom Line

Titan Machinery’s aggressive growth strategy through strategic acquisitions has positioned the firm for potentially strong growth. These acquisitions have caused a surge in operating expenses and posed significant integration challenges. Yet, improvements in operational efficiencies and the continued trend of positive revenue growth could yield promising financial results. The stock’s current price represents a prime entry point for long-term value investors if Titan successfully integrates its acquisitions.