The new year began with the gear stuck in neutral for Tesla (NASDAQ:TSLA) shares. The EV leader beat Street expectations when it disclosed Q4 deliveries on Tuesday, although that failed to move the needle as far as the stock was concerned.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The company delivered 484,507 vehicles, amounting to a 20% year-over-year increase and an 11% sequential improvement whilst outpacing the Street’s call for 483,000 deliveries. For the full-year, deliveries increased by 38% y/y to 1.81 million, thereby, meeting the company’s guide. Production in the quarter reached 494,989 vehicles bringing the year’s total to 1.85 million vehicles, a 35% increase vs. last year.

The focus now turns to the Q4 results, which Tesla will announce on January 24, when all eyes will be on the margin profile. Tesla has managed to keep volumes up due to a series of price cuts taken throughout last year, but margins have suffered as a result.

That is set to be the case in Q4, says Bernstein analyst Toni Sacconaghi. “Auto gross margins ex-credits are a key question,” he notes. “We model 15.7% vs consensus of 17.8% but see potential downside given the impact of price cuts in September and October as well as significant discounting of ‘inventory’ models in the quarter.”

As for 2024, Sacconaghi paints a bleak picture for Tesla, expecting the company to record lower margins and to disappoint on volumes. The analyst is below consensus on both deliveries, calling for 2.15 million vs. the Street’s 2.2 million, and on EPS ($2.59 compared to $3.31).

“We do not believe that Tesla can further cut prices enough to drive sufficient demand elasticity without potentially becoming FCF negative,” Sacconaghi went on to say.

However, despite FY23 earnings dropping from approximately $6 a year ago to around $2.60, TSLA stock more than doubled in 2023. This signals that real-world performance does not necessarily get reflected in the stock price. So, can Tesla pull off the same feat again?

Sacconaghi is skeptical. Since the analyst thinks the company will find it hard to increase deliveries by 20% in 2024 (and 2025) whilst believing FY24 margins and EPS will be “materially below consensus amid required ongoing cost cuts,” Sacconaghi’s view is that investors will begin to “increasingly question the company’s growth narrative.”

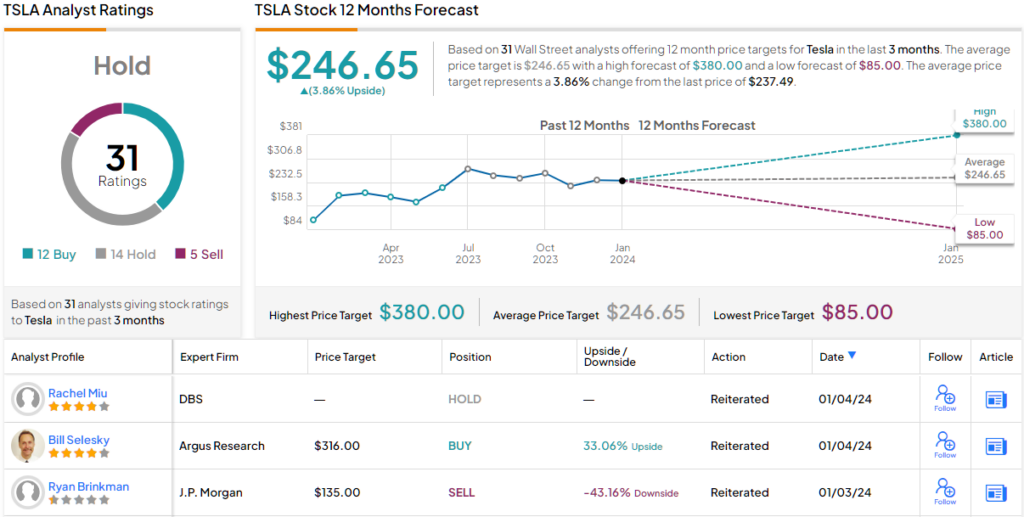

So, bottom-line, Sacconaghi remains one of the Street’s most prominent TSLA bears, reiterating an Underperform (i.e., Sell) rating. If Sacconaghi’s price target of $150 is met over the next 12 months, investors could face major losses of ~37%. (To watch Sacconaghi’s track record, click here)

Amongst Sacconaghi’s colleagues, 4 join him in the bear camp, and with an additional 12 Buys and 14 Holds, TSLA stock claims a Hold consensus rating. At $246.65, the average target suggests the shares have a modest upside of ~4%. (See TSLA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.