Carnival (CCL) is a global travel company with a portfolio of nine cruise lines. Amid the COVID-19 pandemic, Carnival’s operations took a hit with a substantial pileup of debt. Carnival’s recent third-quarter business update provided a slew of positives for the company. The stock is already up 74.4% over the past 12 months.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

A gradual global reopening as economies recover from the pandemic bodes well for Carnival. Let’s take a look at the major developments at Carnival and understand what has changed in its key risk factors that investors should know. (See Carnival stock charts on TipRanks)

In the third quarter, Carnival witnessed cash flow positive voyages, and this trend is expected to continue with eight of its nine brands having resumed guest operations as part of a gradual return to service. Additionally, during the quarter, booking volumes for all future cruises remained higher than the first quarter.

Its third-quarter revenue of $546 million was 1,661.3% higher year-over-year but lagged analysts’ estimates by $248.8 million. While adjusted net loss came in at $2 billion for the quarter, the company noted that its liquidity of $7.8 billion was sufficient to return to full cruise operations.

Moreover, through debt management initiatives, Carnival has decreased future annual interest expenses by over $250 million per year, and has also completed cumulative debt principal payment extensions of approximately $4 billion, which bodes well for its future liquidity position.

Carnival President and CEO Arnold Donald, “Even with the unusually short booking window and capacity limitations, the brand achieved occupancy of ~70%, which speaks to the strong underlying demand for our core product.

“Our booked position for the second half of 2022 is at a new historical high, including our seasonally strong third quarter with all our ships planned to be in operation, despite reduced marketing spending.”

On September 29, Stifel Nicolaus analyst Steven Wieczynski reiterated a Buy rating on the stock with a price target of $39.

As Carnival reintroduces marketing activities, the analyst expects strong booking/pricing pattern trend to continue strengthening. Additionally, Wieczynski expects Carnival to emerge from the COVID-19 pandemic as a leaner and more efficient company.

The stock has a Hold consensus based on three Buys, two Holds and three Sells. The average Carnival price target of $28.04 implies 8.4% upside potential for the stock.

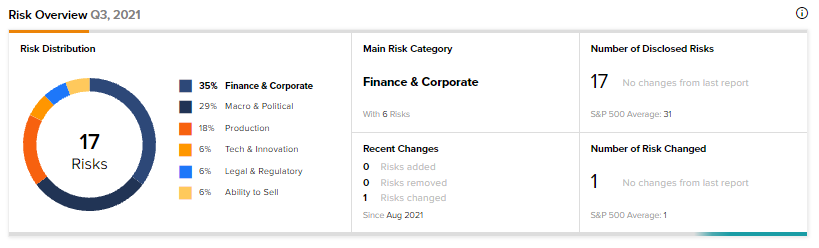

Risk Factors

According to the new Tipranks’ Risk Factors tool, Carnival’s main risk category is Finance & Corporate, which accounts for 35% of the total 17 risks identified. On October 1, the company changed one key risk factor under the Macro & Political risk category.

Carnival highlights that the COVID-19 pandemic is expected to continue to have a substantial impact on its financials and operations. This, in turn, affects the company’s ability to receive acceptable financing.

This impact from the pandemic, and its effect on people’s ability or desire to travel, is expected to continue to impact Carnival.

Related News:

ING Groep Unveils €1.7B Share Buyback Program

Bed Bath & Beyond Crashes 22% on Disappointing Q2 Results

Merck to Acquire Acceleron Pharma for $11.5B