There’s no stopping the stock market right now, with the trend heading almost exclusively in one direction – up. After piling on the gains since April’s tariff-related meltdown, the S&P 500 currently sits at an all-time high, having notched 31 days of record peaks this year.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Of course, the gains are being fueled by AI, a segment that is still seen in the early days of growth. According to market.us, the global AI market was valued at $391.70 billion in 2024 and is expected to grow from $542.50 billion in 2025 to roughly $10,173.05 billion by 2034, representing a CAGR (compound annual growth rate) of 38.50% over that period.

That’s a big step up and the kind of growth that chimes well with Wedbush analyst Daniel Ives’ take on what’s coming next in the AI space, with the 5-star analyst thinking another leg up is imminent.

“We believe the AI Revolution is now heading into its next stage of growth as the tidal wave of Big Tech capex spending coupled by enterprise use cases now exploding across verticals is creating a number of AI winners in the tech world,” Ives said. “The last few months we have seen a major validation moment for our AI Revolution bull thesis as the cloud stalwarts Microsoft, Amazon, and Google are leading the charge on this unprecedented spending cycle.”

But it’s not only those names that stand to benefit. Ives sees two particular stocks as well-positioned to make the most of the next AI wave. So, we’ve decided to give his choices a closer look and for the wider Street view, we also ran these tickers through the TipRanks database. Let’s dive in.

Tesla (TSLA)

The first Ives-endorsed AI name we’ll look at is Tesla, the world’s most famous EV maker. The Elon Musk-led company is a pioneer in electric vehicles, largely responsible for making EVs a mainstream concern and setting in motion a revolution in the auto industry. But Musk has always maintained that Tesla’s ambitions extend far beyond just making cars and although its revenue is still mainly derived from vehicle sales, the company is increasingly touting its AI endeavours as the key for future growth.

The company’s AI ambitions are evident in two main ventures – autonomy and robotics. Tesla’s autonomy push centers on its Robotaxi service, which launched in Austin earlier this year. The program operates within a limited area and still uses in-car safety monitors, though Tesla claims the software is nearing full autonomy. Expansion to other U.S. cities is in progress, while Tesla is also developing the Cybercab, a purpose-built vehicle without pedals or a steering wheel, slated for production before 2027.

In robotics, Tesla’s Optimus humanoid continues to evolve, now trained through human-task video imitation rather than motion capture. Recent demos showed Optimus performing coordinated movements that Musk says were fully autonomous, although that claim has been disputed. Musk has also stated that Optimus could become Tesla’s biggest product, but production remains small-scale, and leadership turnover has raised doubts the project is still more visionary than near-term reality.

Nevertheless, for Ives these initiatives represent huge potential that set the scene for outsized AI-driven growth over the coming years.

“An accelerated AI path for the company is now on the horizon and investors are underestimating the transformation underway at the company. We believe Tesla is taking major steps in advancing its AI Revolution path with autonomous and robotics front and center heading into 2026 that will be a game changer and define Tesla’s future,” the analyst explained. “We believe Tesla could reach a $2 trillion market cap early 2026 in a bull case scenario and $3 trillion by the end of 2026 as full scale volume production begins of the autonomous and robotics roadmap.”

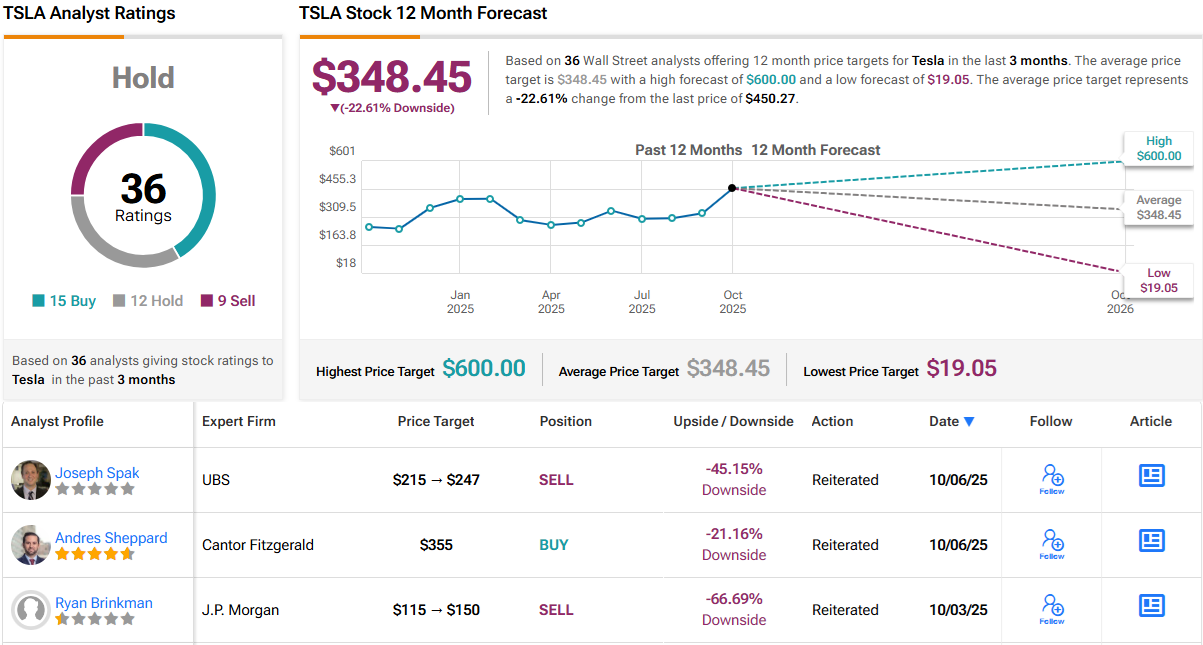

Quantifying his stance, Ives rates TSLA shares as Outperform (i.e., Buy), while his Street-high $600 price target offers 12-month upside of 33%. (To watch Ives’ track record, click here)

That’s a decidedly bullish stance, especially compared to the broader Street mood. Among the mix of 15 Buys, 12 Holds, and 9 Sells, Tesla only manages a Hold (i.e., Neutral) consensus rating. And with an average price target of $348.45, analysts collectively suggest the stock has already sprinted ~23% past where they think it should be. (See TSLA stock forecast)

Progress Software (PRGS)

From a stock market giant, we’ll transition to a far less heralded name. Progress Software is a enterprise software company that helps organizations build, deploy, and manage business applications and digital experiences. Its portfolio spans platforms for web content, data connectivity, application development, decision automation, and infrastructure monitoring, among others. In recent years, the company has repositioned itself more as a provider of infrastructure and tooling that underpins modern, data-driven operations – and AI plays a central role in that shift.

Early in the year, the company launched a managed data platform (Progress Data Cloud) to simplify enterprise data and AI operations in the cloud. Meanwhile, at the end of June, it acquired Nuclia, a specialist in agentic Retrieval-Augmented Generation (RAG) technology, in order to embed advanced, context-aware AI capabilities across its stack.

Progress is also adding AI to its UI tools to help with coding, design, and reporting, improving its content platforms with smarter personalization and search, and using AI in its file tools to speed up document handling and decision-making.

With that as backdrop, the company’s recent quarterly results showed robust growth for both the top and bottom line. In the recently released fiscal third quarter readout (August quarter), revenue reached $250 million, amounting to a 40% year-over-year increase and beating the Street’s forecast by $9.89 million. ARR (annualized recurring revenue) – a key metric for software companies – rose by 47% vs. the year ago period (in constant currency), reaching $849 million. At the other end of the spectrum, adj. EPS of $1.50 outpaced analyst expectations by $0.20.

Looking at the company’s value proposition, Wedbush’s Ives thinks the Street is underestimating the potential here.

“The company continues to balance strong expense discipline with incorporating investments into AI to drive productivity gains… We continue to believe PRGS is an underappreciated 3rd derivative AI name as the company integrates AI across its portfolio following the Nuclia acquisition while driving cost efficiencies across operations to improve its margins and cash flow overtime,” Ives opined.

That conviction supports Ives’ Outperform (i.e., Buy) rating and a $75 price target. If his thesis plays out, PRGS investors could be looking at a 61% return over the next year.

Meanwhile, the rest of the Street is gradually catching on. Based on 3 Buys and 2 Holds, PRGS earns a Moderate Buy consensus rating. The average price target sits at $67.04, which points to ~44% upside potential from current levels. (See PRGS stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.