Steris has agreed to snap up peer Cantel Medical Corp in a cash and stock deal valued at $3.6 billion, in what marks another consolidation move in the healthcare sector.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Under the terms of the agreement, Steris (STE) has offered to pay $84.66 per Cantel common share, based on Steris’ closing share price of $200.46 on Jan. 11. Cantel stockholders will get about $16.93 in cash and 0.33787 of a Steris ordinary share for each Cantel share they own. Cantel shares closed at $83.87 on Jan. 12.

The deal translates into a total enterprise value of about $4.6 billion, including Cantel’s net debt and convertible notes. The transaction has been unanimously approved by the Boards of Directors of both companies.

Cantel (CMD) is a global provider of infection prevention products and services primarily to endoscopy and dental customers. Meanwhile, Steris sells sterilization equipment, surgical tables and other products to hospitals and laboratories.

Steris intends to fund the cash portion of the deal and repay a significant amount of Cantel’s existing debt with $2 billion of new debt for which it has secured bridge financing. The transaction is expected to close by the end of June 30, subject to regulatory approvals and the approval by Cantel shareholders.

“We have long appreciated Cantel, which is a natural complement and extension to Steris’ product and service offerings, global reach and customers,” said Steris CEO Walt Rosebrough. “Our companies share a similar focus on infection prevention across a range of healthcare customers. Combined, we will offer a broader set of customers a more diversified selection of infection prevention and procedural products and services. We firmly believe we will create greater value for our customers and shareholders together.”

Additionally, the companies expect to generate $110 million in annualized pre-tax cost synergies by the fourth fiscal year following the close, with approximately 50% achieved in the first two years. Cost synergies are expected to be primarily driven by cost reductions in redundant public company and back-office overhead, commercial integration, product manufacturing, and service operations.

Oppenheimer analyst Michael Matson believes that the deal makes both strategic and financial sense. However, he reiterated a Hold rating on STE, adding that shares should trade in line with its current P/E multiple of ~27x his CY 2022E EPS estimate.

“The deal allows STE to significantly expand its gastrointestinal (GI) presence and to expand into the adjacent dental market,” Matson wrote in a note to investors. “The COVID-19 pandemic has resulted in an increased focus on infection prevention, which we expect to serve as a tailwind for CMD’s business over the longer-term.”

The analyst estimates the acquisition could drive adjusted EPS accretion of ~7% in CY22, ~10% in CY23, and ~11% in CY24. (See STE stock analysis on TipRanks)

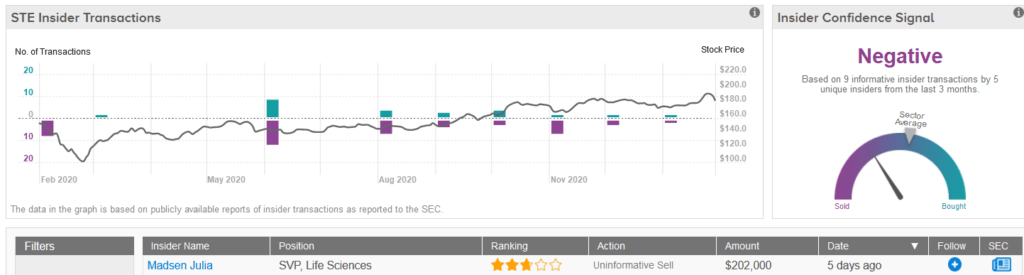

What’s more, TipRanks data shows that corporate insiders sold STE shares worth $3.9 million over the past three months.

Related News:

Bristol-Myers To Buy Back Another $2B In Stock

Truist Financial To Resume $2B Share Buyback In 1Q; Shares Rise 3%

Chemung Financial Approves New Share Buyback Program; Street Says Hold