Shares of enterprise work management platform Smartsheet (NYSE:SMAR) dropped 10.7% in Thursday’s after-hours trading. The company delivered better-than-expected Q4 Fiscal Year 2024 financial results. However, its Q1 FY2025 revenue outlook fell short of expectations, dragging its stock lower.

Smartsheet stock has dropped nearly 16% year-to-date, underperforming the S&P 500’s (SPX) over 8% gain.

Smartsheet Exceeds Analysts’ Q4 Estimates

Smartsheet delivered total revenue of $256.9 million in Q4, up 21% year over year. This compares favorably to the analyst’s estimate of $255.2 million. The year-over-year growth reflects strength in its Subscription revenue, which increased 23% year over year. However, the Professional services revenue declined 4% year over year during the fourth quarter.

What stood out is that the company’s annualized recurring revenue surpassed $1 billion in the fourth quarter. The company highlighted that the strong demand from its enterprise customers supported the recurring revenue.

Thanks to the strong sales, Smartsheet delivered adjusted earnings of $0.34 per share compared to $0.07 in the prior-year quarter. Further, its EPS exceeded analysts’ average estimate of $0.18.

Q1 Outlook Misses Expectations

SMAR expects its top line to be between $257 million and $259 million in Q1 of FY2025, up 17-18% year over year. However, it fell short of analysts’ estimate of $263.6 million.

As for FY2025, Smartsheet projects its revenue to be between $1.113 billion and $1.118 billion, representing 16% to 17% growth.

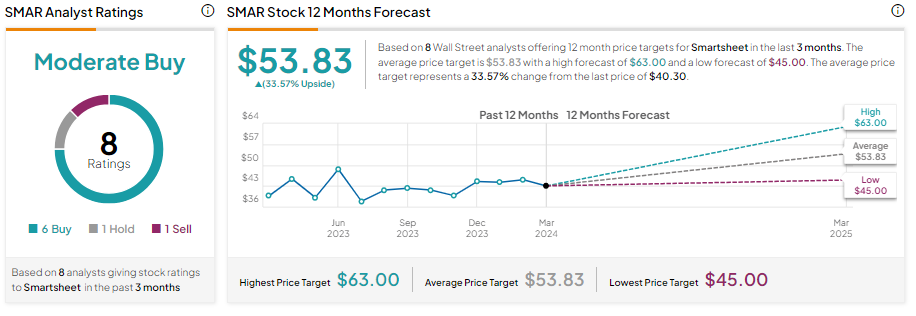

Will Smartsheet Stock Go Up?

Analysts’ average price target on SMAR stock is 53.83, suggesting a decent upside potential of 33.57% over the next 12 months. Smartsheet is unifying its go-to-market operations and focusing on product and innovation to drive future growth. Further, the company sees a significant opportunity to win additional market share through its Artificial Intelligence (AI)-enhanced collaborative workflow solutions.

Currently, the stock has a Moderate Buy consensus rating, reflecting six Buy, one Hold, and one Sell recommendations.