Exercise equipment maker Peloton (NASDAQ:PTON) likely had enough troubles already. It built out its production capacity to deal with an excess of orders that made it a pandemic darling but then lost a lot of those orders when gyms became a thing again. Now, it’s got a lot of capacity and not much to fill it with. And when Wolfe Research offered up a downgrade, it’s small wonder Peloton was down 8.29% in Wednesday’s trading.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Wolfe Research analyst Zach Morrissey, according to a Seeking Alpha report, offered word that Peloton was likely to suffer under the weight of lowered demand for longer than most were looking for. Worse yet, all those growth initiatives mentioned previously are hitting those low-demand conditions like a bus, and Wolfe Research is beginning to doubt that all that growth will do Peloton any good. That’s posing a multi-sided problem for Peloton, including shaky profitability potential as well as damaged cash flow.

Worse yet, Wolfe suggests that Peloton’s backup plan of subscription-driven streaming exercise programs likely won’t be the lynchpin of a turnaround. Why? Because the basic problem remains, the audience for said streaming programs is inherently limited as people are no longer buying the exercise equipment. Sure, there’s still that bloc of potential subscribers who bought in during the pandemic and before gyms were allowed to operate once more. But that’s a limited bloc as it is, and some of them are just returning to normal.

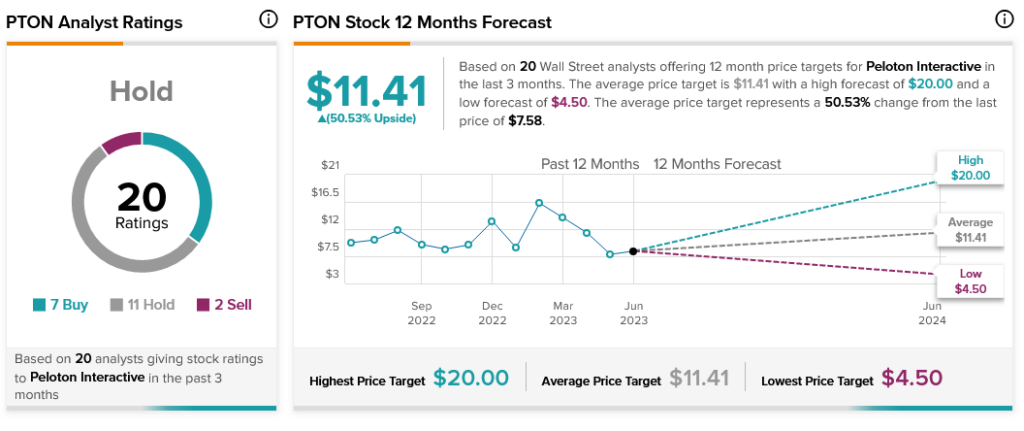

That’s left Peloton as very much a Hold, with seven Buy ratings, two Sells, and 11 Holds to its credit. However, those willing to take the gamble will find that its average price target of $11.41 per share gives Peloton stock an impressive 50.53% upside potential.