Altair Believes the Sale Process Was Poorly Timed and Flawed and that There is No Imperative to Sell the Company

Protect Your Portfolio Against Market Uncertainty

- Discover companies with rock-solid fundamentals in TipRanks' Smart Value Newsletter.

- Receive undervalued stocks, resilient to market uncertainty, delivered straight to your inbox.

Proposed Transaction with Vista Significantly Undervalues the Company

Sends Open Letter to Fellow Avalara Shareholders

SANTA ROSA, Calif., Sept. 8, 2022 /PRNewswire/ — Altair US, LLC (“Altair” or “we”), a pre-IPO angel investor in Avalara, Inc. (NYSE: AVLR) (the “Company” or “Avalara”) and one of the Company’s largest shareholders, today announced its strong opposition to the sale of Avalara to Vista Equity Partners (“Vista”). Altair also released an open letter to fellow Avalara shareholders explaining why Altair will vote against the transaction.

“Altair is extremely disappointed that the Avalara Board of Directors decided to throw in the towel amid modest headwinds and sell this rapidly growing and successful company at this volatile time in the capital markets and global economy, especially after running a limited and flawed sale process,” said Richard H. Bailey, Managing Director of Altair US. Mr. Bailey continued, “Most importantly, the negotiated price does not come close to compensating Avalara’s owners for the Company’s huge potential. We are enthusiastic about the Company’s prospects and, like other Avalara investors, are willing to weather temporary headwinds to gain the benefit of the Company’s extremely bright future.”

The full text of Altair’s letter to its fellow Avalara shareholders is below:

September 8, 2022

Dear Fellow Avalara Shareholders:

Altair US, LLC (“Altair” or “we”) is a longstanding investor in Avalara, Inc. (“Avalara” or the “Company”) (NYSE: AVLR). We first invested in the Company in 2004 as one of its earliest outside shareholders, and we purchased additional shares in all but one private investment round prior to the Company’s initial public offering. Today, we beneficially own approximately 1.0% of Avalara’s outstanding shares, making us one of the Company’s largest and longest-tenured shareholders.

We believe strongly in Avalara’s opportunity to create significantly more value for shareholders. Tax compliance is critical for all businesses, but despite increasing complexity and risk of exposure, many businesses continue to calculate taxes and file returns manually. We believe Avalara, by providing simple, automated transactional tax solutions in a market with limited competition, has a clear and long runway to continue to compound growth for many years, regardless of macroeconomic conditions. Avalara, in short, is a fundamentally sound business, with a resilient business model, strong partnerships with leading companies and a compelling opportunity to be a part of every transaction in the world.1

As Ross Tennenbaum, Avalara’s Chief Financial Officer, said this May:

“We’re addressing a large, low-penetrated market where we are a leader in the space, with competitive moats and a differentiated business strategy. We are positioning to capture a leader share of our market opportunity.”2

And again, as recently as June 28, Mr. Tennenbaum expressed great enthusiasm for the prospects of Avalara:

“We remain in the early days of penetration in a big market and still believe we are a growth story where we can sustain strong growth for a number of years as we build a multibillion-dollar revenue company. We also believe we can do that with significant margin improvement.”3

Avalara’s leadership team has taken great pains to explain that despite the difficult global economic environment, Avalara is positioned to succeed, stating that the Company is “a long and strong growth compounder and well-positioned to grow in good and in challenging times.”4

It is dumbfounding to us that the Avalara Board of Directors (the “Board”) would have chosen now to sell the Company. The management team has expressed confidence in the future, despite an uncertain macroeconomic environment that would surely cause any potential buyer to pause. Meanwhile, capital markets are volatile, private equity funds are proceeding very cautiously and the debt financing market for large buyouts, like that of Avalara, limits the ability of private equity firms to pay reasonable multiples. On top of this, the Company is on the verge of achieving operating profitability for the first time,5 which we believe will make it more attractive to a larger and different set of buyers. In light of these circumstances, this was simply the wrong time for the Board to look for a buyer for Avalara.

Worse yet, the Board’s chosen sale “process” was deeply flawed and limited, suffering from being a spur-of-the-moment frolic, driven by inbound inquiries and the desires of buyers, rather than having been carefully designed and timed to create demand and competitive tension.

Unsurprisingly, the flawed process resulted in a “negotiated” price that is inadequate to compensate Avalara’s current shareholders for giving up their claim on the future earnings of this attractive business. And while the Board and management may be personally satisfied with this deal (which will put more than $60 million6 in their pockets), along with the Company’s financial advisor, Goldman Sachs (which stands to earn a handsome transaction fee of $75 million7), longstanding Avalara shareholders are not being fairly compensated for their commitment to the Company and their investment in its future potential.

The Company’s promise is readily apparent. Avalara is delivering double-digit revenue growth quarter-after-quarter and year-after-year, is on the verge of achieving operating profitability,8 has approximately $1.5 billion in cash reserves to weather any short-term challenges9 and has a commanding and protected leadership position in an attractive industry.10

All of this, then, raises a fundamental question: Why sell the Company now? We are concerned that the Board’s decision-making process has been influenced by two parties with an enormous economic interest in seeing the Company sold: Avalara management, which stands to realize more than $60 million from the transaction11 (and which otherwise must navigate a more complex macroeconomic environment than it has seen recently) and the Company’s financial advisor, Goldman Sachs, which will be rewarded with a fee of $75 million for identifying a deal12 and which has longstanding and lucrative relationships with the buyers and their affiliates (from which Goldman Sachs has realized more than $120 million in fees over the last two years alone).13 These conflicts of interest raise the important question whether Avalara’s Board received any truly independent, objective input regarding the timing and merits of the proposed transaction. On whom did the Board rely?

We will be voting against the deal.

Only one party made a final proposal to buy Avalara, despite the fact that Avalara is a company with very attractive long-term fundamentals and a “competitive moat.”14 This unfortunate and suboptimal outcome was the result, in our view, of a poorly timed and flawed sale process.

Macroeconomic factors like rising interest rates, inflation, supply chain disruptions and concerns over consumer spending have created significant economic dislocation and uncertainty in 2022. Avalara has certainly not been immune to these challenges. During the first quarter of 2022, sales and marketing capacity constraints led to slower than expected growth in new bookings and upsell bookings, and the Company’s international business faced some weakness attributable to a decrease in contract pricing with a large marketplace partner.

At the same time, volatile capital markets have lowered equity valuations and made financing of large buyout transactions difficult. The Russell 3000 was down 20% during the first half of 2022, its worst start to the year ever.15 For technology companies, these issues have been compounded by the normalization of growth and post-pandemic demand, rattling investor confidence in the sector. Not surprisingly, Avalara’s stock price was down approximately 23% during the first quarter of 2022 given these economic uncertainties and the “risk off” capital markets environment.

While Avalara’s share price declined as investors pulled back from higher-risk assets, there were no signs that the Company’s long-term prospects were fundamentally impaired. As noted above, in May and June, the Company’s executive officers continued to express great confidence in the Company’s prospects and batted away concerns that the economic slowdown would have much impact on the Company in the mid- to longer-term. Notably, on the May earnings call, for example, Mr. Tennenbaum said that Avalara’s broad customer diversity helps “insulate the [Company] from shock to e-commerce and the broader economy” and that its international business remains “a huge opportunity and green space” going forward.16

The Company’s projections also reflect management’s confidence that the short-term economic disruptions would have only a marginal impact on the mid- and long-term prospects of the business. While the Company’s “May Projections” forecasted a Non-GAAP Operating Loss of $11 million in 2022 and Non-GAAP Operating Income of $55 million in 2023, the Company’s updated “July Projections” show the Company breaking even in 2022 (an improvement) and a Non-GAAP Operating income of $52 million in 2023.17

Faced with uncertain economic times – but ones the executive team was confident the Company would weather successfully18 – a depressed stock market and a volatile financing market, it is incomprehensible that the Board would have thought the timing was optimal to maximize the value of the Company in a sale.

On closer inspection, it appears that this misguided idea didn’t even originate with the Avalara Board. Instead, the Board appears to have been enthralled that various private equity parties – undoubtedly acting at an opportunistic time for them, as depressed and volatile public equity markets made valuations more attractive to potential acquirers – had approached the Company in March and April about a potential buyout. And as flattering as it undoubtedly was to be the subject of inbound inquiries, we believe there was no imperative for the Board to undertake a sale process amid a temporarily strained economic environment coupled with inhospitable financing markets.

By July, as proposals for Avalara were due under the Board’s process, high-yield corporate bond spreads to treasury yields had widened more than 200 basis points from January, significantly affecting the availability of financing and the cost of debt for any buyout. Notably, the number of announced private equity buyouts in the $5 billion to $10 billion range in Q2 was down more than 40% from a year earlier19 because of the turmoil in the economy and financing markets.20

There is no doubt that the Board’s timing for conducting the once-and-only sale of Avalara impacted the number of proposals and the competitive nature of the “auction.” Several potentially interested parties withdrew from the process, specifically citing unfavorable market conditions21 and an uncertain macroeconomic environment.22 Even Vista itself did not initially submit a proposal due in part to difficulty securing financing because of the “deterioration in the financial markets”23 and then came back with a lower indication of interest than what it had originally proposed, in part because of “the deterioration in the financial markets.”24

Most companies interested in examining a sale determined that Q2 was not the time to be negotiating a deal. Indeed, that sophisticated private equity firms with strong track records in the sector did not have the conviction to make a proposal (or could not obtain enough or inexpensive enough financing to make a proposal) for Avalara should not have been a surprise to the Board, given the general market conditions and widely acknowledged dislocation in the buyout market.

The surprise, instead, is that the Board ignored these glaring signs of bad timing and proceeded to sell the Company anyway.

Having launched a sale process in the middle of market turmoil, the Board should have expected that no bidder would provide an indication of interest that matched the Board’s view of intrinsic value. That is exactly what happened. In fact, no bidder was even able to submit a final bid on the Board’s timeline because of the lack of certainty regarding Avalara’s near-term business outlook and the inability to finance an attractive proposal.

When the deadline for making proposals came and went without the Company receiving any final proposals, the Board on July 16 rightly “decided to terminate the potential sale process.”25 That was the smartest thing this Board did during this “sale” process.

Unfortunately, it was not a decision that lasted.

Instead, the Board eagerly re-engaged with Vista when Vista came back to the table with a price that was almost 10% below its initial indication of interest. The Board’s engagement on that basis undoubtedly signaled to Vista the Board’s irrational desire to complete a deal and its weak negotiating position. Vista from then on had the upper hand and was able to negotiate a deal very much in its favor.

And while this unusual negotiating move – agreeing to re-engage with a bidder at a significantly lower price to accommodate temporary financial market dislocation – may have been the most obvious and egregious process flaw that irreparably tainted the sale process, it certainly was not the only one.

From the start, the Company’s financial advisor, Goldman Sachs, failed to conduct a robust sale process. It initiated contact with just three potential buyers. The few other firms in the process had all been engaging with the Company for several months about providing growth capital for the Company’s promising international expansion opportunities. Later, when a rumor of a sales process appeared in the media, and Goldman fielded additional in-bound interest from “a variety of parties,”26 Goldman appeared to pay little attention to those potential buyers and sources of financing; in fact, as far as we can tell, no substantive discussions took place with any of these parties.

The Board’s process, essentially, was to interact with the limited number of firms that had indicated some interest in a transaction with the Company in March and April, and to make outbound phone calls to just three additional firms. We believe this process was woefully inadequate, especially in the face of challenging market conditions. Compounding this deficient process was the Board’s willingness to accept a “no-shop” provision, severely limiting the Company’s ability to solicit or encourage other proposals once the deal was announced.

In fact, it’s not unreasonable to infer that Vista was the preferred buyer all along. Goldman has longstanding ties to Vista, after all, including by earning more than $80 million27 in fees during the last two years from Vista and its affiliates and portfolio companies. It is also not lost on us that Avalara director Marcela Martin serves on a board of a Vista-controlled company with four Vista professionals, including the Vista partner that was responsible for the Avalara deal. And Avalara director Rajeev Singh has also served on the board of a company that Vista acquired. Perhaps Vista was the “logical” and “known” buyer and served as an easy way for Goldman to earn a $75 million transaction fee and for the Company’s senior leadership team to reap an enormous payday while side-stepping a more challenging operating environment, even if the sale price was not optimal for shareholders.

However, whether Vista was the preferred party all along, or not, it should have been obvious to this Board that, between Goldman’s lucrative relationship with Vista and its outsized success fee for this transaction, Goldman was predictably going to recommend a transaction and that nearly any available transaction would be good enough.

The egregious conflicts of interest that incentivized management and Goldman to advocate for the transaction raise serious and troubling questions as to whether the Board followed a reasonable and prudent process. Avalara management stands to receive a $60 million payday as a result of the deal28 (not including the $2.7 million the non-employee directors will receive29). Two of the Company’s directors are serving or have served on the boards of Vista affiliates. Goldman has a close working relationship with Vista and its affiliates, for which it received approximately $80 million in fees over the past two years (not including another $43 million from Vista equity holders and their affiliates30), and stands to receive $70 million contingent upon closing of the transaction31 (plus a net gain of an estimated $5 million with respect to capped call transactions32). These gross conflicts of interest and the absence of truly independent financial advice made for a biased and flawed process which, unsurprisingly, led to a great deal for Vista and Goldman but a disappointing outcome for Avalara shareholders.

The Board could very easily have obtained a second opinion from an independent financial advisor – a firm without a strong financial incentive for getting a deal done or maintaining a mutually beneficial relationship with the would-be buyer. So, why didn’t the Board engage a second, unconflicted financial advisor to objectively review the timing, process and terms of this important transaction? We suspect the Board was concerned that any such independent financial advisor would question the suboptimal timing and flawed approach used by this Board and Goldman to arrive at the deal.

And the price.

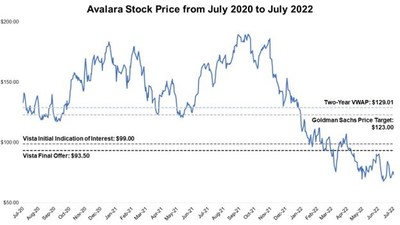

The Board’s inexplicable haste to sell the Company could perhaps be excused had the ill-designed and poorly executed sale process nevertheless maximized value for Avalara shareholders. The negotiated transaction, at $93.50 per share, falls far short.

1 Source: FactSet. (NYSE: AVLR) Data as of July 6, 2022, the last trading day prior to media reports speculating on the proposed merger. “Vista Initial Indication of Interest” calculated as the midpoint of the range of $97.00 and $101.00 per share of Avalara common stock as disclosed on page 39 of Avalara’s Preliminary Proxy Statement.

Several sell-side analysts and the investors they cover33 openly expressed doubt about the deal price:

- “Given Avalara’s leading position in the large and underpenetrated market for tax compliance automation software, our initial view is that the proposed transaction price is somewhat underwhelming.” (William Blair, August 8, 2022)

- We do wonder if they could do better than the current implied valuation… [We] wouldn’t be surprised [if] a modestly higher price is ultimately achieved for shareholders.” (Needham)

- “There has been a lack of enthusiasm from our investor conversations this morning… We believe the [near-term] outlook likely pushed the needle towards taking a deal at a multiple that could prove conservative over the [long-term] and may have been a bit lower than what some investors were hoping for.” (Evercore ISI)

- “[W]e are a little surprised at AVLR’s willingness to sell at $93.50 given its recently laid out medium-term targets ($250 million of FCF by CY 25) and an aspirational goal of reaching $3 billion in revenue.” (Raymond James)

In addition to analyst and investor sentiment, there are five objective measures of value that all suggest the deal price is inadequate and that a fair deal would be priced well over $110 per share:

- Analyst price targets. Prior to the announcement of the transaction, sell-side analysts had a mean price target for Avalara of more than $117 per share. Price targets had been at or above $100 since June 2019, when the Company’s LTM revenue was less than half of what it is today. The day before the deal was announced, Goldman’s own analyst covering Avalara had a price target of $123 per share (a 32% premium over the deal price). Typically, change-in-control transactions occur above the median sell-side price targets. Among the comparable transactions selected by Goldman for its fairness opinion, for example, the deal price represented an average of a 15% premium34 to the mean target price the day before the announcement of the transaction.35 For Avalara, the transaction value represented a 20% discount to the mean sell-side price target.

- Historical valuation multiples. Throughout Avalara’s time as a public company, it has traded at a median enterprise value multiple to the next-twelve months projected revenue of 12.9x. Since the beginning of 2020, when the Company’s growth accelerated due to pandemic-driven shifts in customer demand patterns, it has traded at an even higher multiple: 16.5x the next twelve-months forecasted revenue. The proposed transaction is valued at just 8.1x forecasted revenue, a substantial discount to the Company’s historical valuation.

- Indications of interest from private equity firms before the dramatic increase in financing costs. Members of Avalara’s senior management team began receiving inbound interest from private equity firms in March and April 2022. During that time, Avalara was trading at or above $90 per share. Even a modest sale premium of 25% – which is in-line with comparable transactions and which the private equity firms were likely prepared to pay, otherwise they would not have reached out – would put a transaction price for Avalara well above $110 per share.36

- Premiums in a bear market. Avalara’s total shareholder return during the one-year period prior to the transaction announcement was -44%, compared to an average of +19% for the comparable transactions examined by Goldman.37 One should expect companies trading at near-term highs would receive smaller premiums, not larger ones, than companies that have traded down in a risk-off market environment. And yet, the premium offered for Avalara is lower than the median of the premiums in the comparable deals.

- Premiums to an adjusted unaffected price. Goldman’s fairness opinion claims the “undisturbed” price of Avalara’s shares was the closing price on July 6, the day before rumors of a buyout surfaced. And perhaps Avalara’s stock rallied thereafter in part because of the deal rumor. But, from July 6 to August 5 – the last trading day before the announcement of the transaction – the comparable public companies38 traded up during the widespread market rally of July (that surely would have also increased Avalara’s stock price) by an average of 13%.39 Avalara would likely have matched this performance even in the absence of the deal rumor. And so, we estimate that the Company’s true “undisturbed” price (July 5 plus peer company returns) is $83.15 per share, not the $73.54 used by Goldman. Applying the median one-day premium of comparable transactions40 to the true undisturbed price yields a price for Avalara of over $103 per share.

We are proud to have owned Avalara for nearly twenty years. And based on the Company’s strong competitive position and promising future, we are perfectly content to continue to own Avalara as an independent entity for years to come. We understand there has been a deceleration in revenue growth for the first time in Avalara’s history as a public company. But the Company’s modestly slower revenue growth over one or two quarters is not a fundamental business issue, nor do we believe that it will persist.

The Board, in the face of this macroeconomic adversity unrelated to the market for tax compliance software, should have insisted that the Company execute through the economic trough, with a plan to emerge stronger and create value in the future. If the Company is to be sold, it should be sold from a position of strength, in a robust financing market and only after a well-run, competitive process. This is not that time.

The proposed transaction is instead the product of bad timing and a flawed process. The price reflects pessimism and transient market dynamics and not the Company’s intrinsic value. We are convinced that, in the near-term, Avalara can deliver value to shareholders far in excess of the $93.50 per share that Vista is offering, and in the longer-term, Avalara can compound that value as it executes its profitable growth strategy.

In our view, there is no reason to sell the Company now, and certainly not at this price. We therefore oppose the transaction.

We look forward to expressing our views about the best path forward to generate maximum long-term value at Avalara.

Sincerely,

//s//

Richard H. Bailey

Managing Director

Altair US, LLC

CERTAIN INFORMATION CONCERNING THE PARTICIPANTS

In connection with the proposed acquisition of Avalara, Inc. (the “Company”) (NYSE: AVLR) by affiliates of Vista Equity Partners Management, LLC (the “Merger”), the Company entered into an Agreement and Plan of Merger, dated as of August 8, 2022, with Lava Intermediate, Inc., a Delaware corporation (“Parent”), and Lava Merger Sub, Inc., a Washington corporation and wholly owned subsidiary of Parent (the “Merger Agreement”). The Participants (as defined below) intend to file a definitive proxy statement and accompanying proxy card with the SEC to be used to solicit proxies for votes (the “Proxy Solicitation”) opposing the adoption of the Merger Agreement at the special meeting of shareholders (the “Special Meeting”) and regarding other proposals that may come before the Special Meeting. The Participants in the Proxy Solicitation are anticipated to be Altair US, LLC, a Delaware limited liability company (“Altair US”), and Richard Bailey (collectively, the “Participants”), the Manager of Altair US. As of the date hereof, each of the Participants may be deemed to beneficially own, in the aggregate, 850,892 shares of common stock of the Company.

THE PARTICIPANTS STRONGLY ADVISE ALL SHAREHOLDERS OF THE COMPANY TO READ THE PROXY STATEMENT AND OTHER PROXY MATERIALS AS THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. SUCH PROXY MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. IN ADDITION, THE PARTICIPANTS IN THIS PROXY SOLICITATION WILL PROVIDE COPIES OF THE PROXY STATEMENT WITHOUT CHARGE, WHEN AVAILABLE, UPON REQUEST. REQUESTS FOR COPIES SHOULD BE DIRECTED TO SROWLAND@SHAREHOLDERSDESERVEBETTER.COM.

Altair is a family office.

Investor and Media Contact

Stanley Rowland

Phone: (925) 708-5611

srowland@ShareholdersDeserveBetter.com

1 CEO Scott McFarlane, Avalara 2022 Analyst Day, June 28, 2022 (“First, we have a clear and unified vision to be part of every transaction in the world. And I am more confident than ever we can achieve this vision.”).

2 CFO Ross Tennenbaum, Q1 2022 Earnings Call, May 6, 2022.

3 CFO Ross Tennenbaum, Avalara 2022 Analyst Day, June 28, 2022.

4 CEO Scott McFarlane, Q1 2022 Earnings Call, May 6, 2022.

5 See Avalara Preliminary Proxy Statement, filed with the SEC on August 24, 2022, at 64, which shows Non-GAAP Operating Income at break-even in 2022 and $52 million in 2023, with Non-GAAP Operating Income projected to approximately double in each of the subsequent two years.

6 Avalara Preliminary Proxy Statement, filed with the SEC on August 24, 2022 at 70.

7 Id. at 62.

8 See supra at Footnote 5.

9 See Avalara’s Form 10-Q for the quarter ended June 30, 2022, filed with the SEC on August 9, 2022, which shows cash and cash equivalents of $1.46 billion.

10 CEO Scott McFarlane, Avalara 2022 Analyst Day, June 28, 2022 (“[W]e have created three competitive moats: Our partner moat; our content moat; and our platform moat that should insulate us from competition and have more recently become offensive weapons in our pursuit of gaining market share.”).

11 Avalara Preliminary Proxy Statement, filed with the SEC on August 24, 2022 at 70.

12 Id. at 62.

13 Id. at 60.

14 CFO Ross Tennenbaum, Q1 2022 Earnings Call, May 6, 2022.

15 Source: FactSet.

16 Avalara Q1 2022 Earnings Call, May 5, 2022.

17 Avalara Preliminary Proxy Statement, filed with the SEC on August 24, 2022, at 63-64.

18 In May, the Board approved mid-term projections indicating that Avalara could achieve operating profitability as soon as 2023 for the first time. See Avalara Preliminary Proxy Statement, filed with the SEC on August 24, 2022 at page 63.

19 Source: Bloomberg.

20 Source: Aaron Kirchfeld and Michelle F. Davis, “Dealmakers Buckle Up as Records Give Way to Ruptures in M&A,” Bloomberg, June 30, 2022 (“Buyout firms, whose spending had been trending up year-on-year as recently as May, are all of a sudden finding it harder to secure the leveraged loans required to get big deals done.”).

21 Avalara Preliminary Proxy Statement, filed with the SEC on August 24, 2022, at 39 (“Party G informed Goldman Sachs that they had determined not to explore a potential transaction involving Avalara because of challenging market conditions,” while “Party C informed members of Avalara’s senior management that they would not submit an indication of interest because of market conditions…”).

22 Id. at 41.

23 Id.

24 Id. at 49.

25 Id. at 41.

26 Id. at 40.

27 Id. at 60.

28 Id. at 68.

29 Id. at 68.

30 Id. at 60.

31 Id. at 62.

32 Id. at 62.

33 Permission to use analyst quotes neither sought nor obtained.

34 Source: FactSet. Data refers to weighted average based on disclosed transaction value.

35 Source: FactSet and Company filings. Comparable transactions refer to those in the “Selected Transactions Analysis” of the Company’s financial advisor and include Ping Identity (Thoma Bravo), Zendesk (Permira & H&F), SailPoint (Thoma Bravo), Datto (Kaseya / Insight), Anaplan (Thoma Bravo), Mandiant (Google), Medallia (Thoma Bravo), Proofpoint (Thoma Bravo), Pluralsight (Vista), Slack (Salesforce), Tableau (Salesforce), Ultimate Software (Hellman & Friedman), Apptio (Vista), SendGrid (Twilio), Adaptive Insights (Workday), MuleSoft (Salesforce), Netsuite (Oracle), Demandware (Salesforce), Marketo (Vista), Cvent (Vista), Solarwinds (Thoma Bravo), Concur (SAP) and Sourcefire (Cisco).

36 Source. FactSet. See supra at Footnote 35 for a list of comparable transactions.

37 Source: FactSet. Data refers to weighted average based on disclosed transaction value.

38 “Comparable public companies” refer to those in the “Selected Public Company Comparables Analysis” of the Company’s financial advisor and include Alteryx, BigCommerce Holdings, BlackLine, Coupa Software, Datadog, Elastic, HubSpot, MongoDB, Okta, PagerDuty, Paylocity, Shopify, Smartsheet and Zscaler.

39 Source: FactSet. Data from July 6, 2022 to August 5, 2022. Data refers to weighted average based on market value at the beginning of the measurement period.

40 See supra at Footnote 35 for a list of comparable transactions.

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/one-of-avalaras-earliest-and-largest-investors-opposes-sale-of-company-to-vista-equity-partners-301620292.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/one-of-avalaras-earliest-and-largest-investors-opposes-sale-of-company-to-vista-equity-partners-301620292.html

SOURCE Altair US, LLC