Consumer spending – and consumer credit – are the long-term drivers of the US economy. So it’s not surprising that the Federal Reserve notes that aggregated consumer credit card balances finished 2023 at a record high level of $1.13 trillion, up $50 billion in Q4 alone. This is a double-edged sword, as the current high interest rate regime makes this credit more expensive – but the increase in credit card usage also suggests that consumer spending remains strong.

And that strength may soon get a boost. Visa (NYSE:V) and Mastercard (NYSE:MA), the world’s two largest credit card issuing and processing companies, have recently settled a class action lawsuit that could provide consumers with an incentive to swipe their cards more often. The suit was an antitrust action against allegedly excessive card swipe fees, and the settlement may run to the tens of billions of dollars. As part of the settlement, both companies have agreed to limit the card swipe fees charged to merchants – a savings that could be passed on to customers.

For the card companies, the settlement promises to end the litigation without hitting revenues too hard – they make most of their money from the interest charged to card users. This opens up a potential boon for Visa and Mastercard, who may see costs go down while profits go up, and Piper Sandler analyst Arvind Ramnani is pounding the table for both big names, recommending that investors buy in now.

According to the TipRanks database, Visa and Mastercard shares also get Strong Buy ratings from the rest of the Street. Let’s take a closer look.

Visa

First up is Visa, the largest company among the world’s credit card issuers. A few ‘vital stats’ will show the magnitude of Visa’s market position. The company has more than 4.3 billion branded cards in circulation globally, across some 200 countries. The cards are issued by more than 14,500 financial institutions and are accepted at more than 130 million merchant locations. Visa processes approximately $15 trillion in annual transaction volume. All of this provides a solid foundation for the stock, and Visa has a market cap valuation of $563 billion.

In business since 1958, Visa has been a leader in the credit card segment since the industry’s beginning. The company has expanded to become one of the stock market’s blue-chip stalwarts. The company generated almost $30 billion in revenue in 2022, and more than $32.6 billion in 2023. It’s one of the market’s most durable companies, and shares in V have shown a steady long-term gain.

The company’s revenues and earnings both show a modest upward trend over the past several years. In the last financial release, covering fiscal 2Q24, Visa’s top line of $8.8 billion was up 10% year-over-year and cleared expectations by $180 million. The bottom line figure was $2.51 per share by non-GAAP measures, based on a non-GAAP net income of $5.1 billion. This EPS was 8 cents per share better than had been anticipated. Visa finished the fiscal quarter, on March 31 of this year, with deep pockets, reporting $20.8 billion in cash and liquid assets on hand – after returning $3.8 billion to shareholders through a combination of dividend payments and stock buybacks.

For analyst Arvind Ramnani, setting out the Piper Sandler take on Visa, the key points boil down to that steady long-term growth and the company’s sheer scale.

“We believe that Visa should be able to grow revenues by 10.7%, driven by multiple growth drivers, including 10.4% growth in Data Processing, 9.5% in Services, and 10.7% International. This is supported by its foundational offering in 1) Annual aggregate transaction volume of ~$15T, with a vast growing TAM of over $250 trillion; 2) New Flows which captures new sources of money movement for consumers, businesses and governments – an in our view will be an important vector for growth; 3) Value Added Services, which serve as an important lever to deepen its client relationships by offering innovative solutions. Further, we believe that Visa can sustain operating margin expansion (modeling +140 bps in FY25) through its scale, continued execution, and efficiencies/margin uplift from new/emerging tech,” Ramnani opined.

Summing up his stance on V, Ramnani gives Visa stock an Overweight (i.e. Buy) rating with a $322 price target that suggests a ~15% share appreciation for the next 12 months. (To watch Ramnani’s track record, click here)

Overall, the Strong Buy analyst consensus rating on Visa shares is based on 24 recent analyst reviews, with a 20 to 4 breakdown favoring Buys over Holds. The stock is selling for $280.21 and its average target price of $315.15 implies a one-year upside potential of ~12%. (See Visa stock forecast)

Mastercard

Now we’ll turn to Mastercard, the industry’s other giant company. Mastercard boasts a market cap of $425 billion, and there are approximately 3 billion Mastercard-issued cards in circulation worldwide. The company’s annual revenue came to $18.88 billion in 2021, rose to $22.24 billion in 2022, and hit $25.09 billion last year.

Mastercard lends its branding to cards issued by a wide range of financial institutions, and then acts as the payment processor for its branded cards. The company processed $9 trillion in gross dollar volume last year, and has already seen $2.3 trillion in gross dollar volume during the first quarter of this year. This represents a 10% increase from the prior-year period. The company’s cross-border volume, a measure of international transactions, was up 18% y/y in 1Q24.

Looking at the headline results from Q1, Mastercard saw quarterly revenue of $6.3 billion, up 10% year-over-year. The top line just skated over the forecast, beating it by $10 million. The company realized a net income of $3.1 billion in the quarter, or $3.31 per share, by non-GAAP reckoning. This compared favorably to the $2.80 EPS from 1Q23, and beat the forecast by 7 cents per share. Mastercard had nearly $7.3 billion in cash and cash equivalents available at the end of the quarter, and paid out $2.616 million to shareholders during Q1, through both repurchases and dividends.

Turning again to Ramnani’s view, we find the Piper Sandler analyst predicting continued growth for Mastercard, as the company grows into a large addressable market.

“In our view, Mastercard should be able to deliver revenue growth of 11.0% this year and 12.7% in FY25, driven by 9.5%/13.5% Payment Network revenue growth (~62% of revenues), and Value-added Services and Solutions growth of 13.7%/11.5% (~38% of revenues) in FY24/ FY25. Underlying growth drivers include a massive untapped opportunity for consumer payments; Mastercard’s aggregate transaction volume of $9T in annual volume, with a vast TAM of over $250 trillion across domestic, cross-border, transaction processing, and value added services revenue channels,” Ramnani wrote.

“Further,” Ramnani adds, “we expect Mastercard can sustain margin expansion (currently modeling +20bps in FY24 and +80bps in FY25) as the company continues to expand, disrupting cash as a preferred method of transacting, and as it grows into new service and tech offerings.”

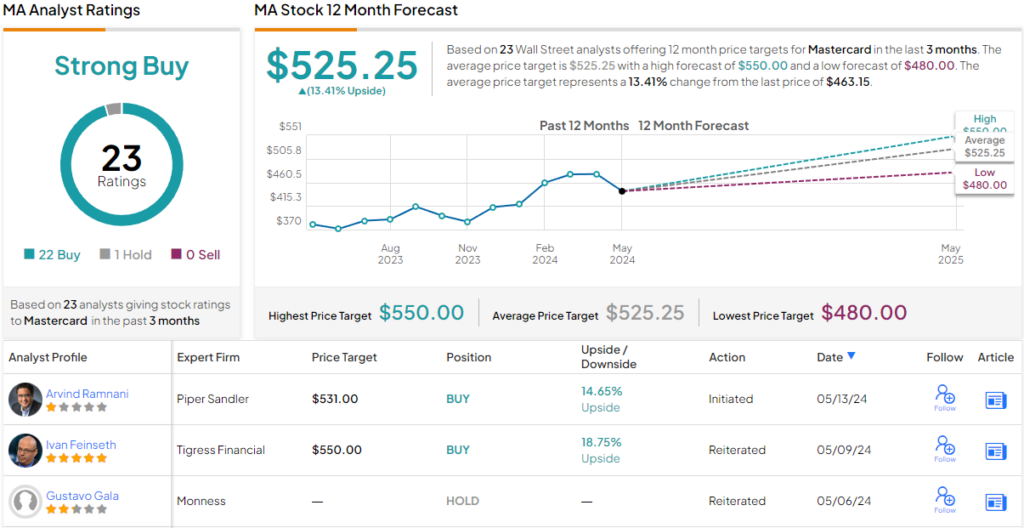

Quantifying these comments, the Ramnani puts an Overweight (i.e. Buy) rating on MA shares, along with a $531 price target that points toward a gain of nearly 15% on the one-year horizon.

All in all, the consensus view from the Street on Mastercard is a Strong Buy, based on 23 recent analyst reviews that feature a lopsided split of 22 Buys to 1 Hold. The shares have a current trading price of $463.05 and an average target price of $525.25, together suggesting a ~13% potential upside by this time next year. (See Mastercard stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.