PepsiCo Inc.’s first-quarter earnings and revenues topped consensus estimates on Thursday. The snacks and beverage company posted a 6.8% year-on-year growth in net revenues to $14.8 billion, which came in ahead of analysts’ estimates of $14.55 billion. Adjusted core EPS of $1.21 per share beat consensus estimates of $1.12.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

PepsiCo Inc’s (PEP) Chairman and CEO Ramon Laguarta said, ““We are pleased with our results for the first quarter as we successfully overcame challenges related to difficult year-over-year comparisons, uneven recoveries across many of our international markets and weather-related business disruptions in the U.S.”

The company’s organic revenues rose 2.4% year-on-year with its Frito-Lay division gaining market share in both salty snack and macro snack categories in the United States with the introduction of products like Doritos 3D Crunch and Cheetos Crunch Pop Mix.

PEP’s beverages business in the United States saw an organic increase in revenues of 2% year-on-year driven by a double-digit growth in revenues for Bubly sparkling water and ready-to-drink coffees under the Starbucks brand.

The company experienced uneven growth in international markets with China, Russia and Brazil showing organic double-digit growth in revenues in 1Q while the Indian and Mexican markets showed mid-to-low single digit growth for the quarter. (See PepsiCo Inc stock analysis on TipRanks)

PEP reiterated its non-GAAP outlook for FY21 and expects a mid-single-digit rise in organic revenue and core EPS to increase in the high-single-digits. The company expects to return around $5.9 billion to stockholders, comprising of share buybacks of $106 million and dividends of $5.8 billion. PEP has already completed its share repurchase program and does not anticipate to buyback any additional shares for the rest of FY21.

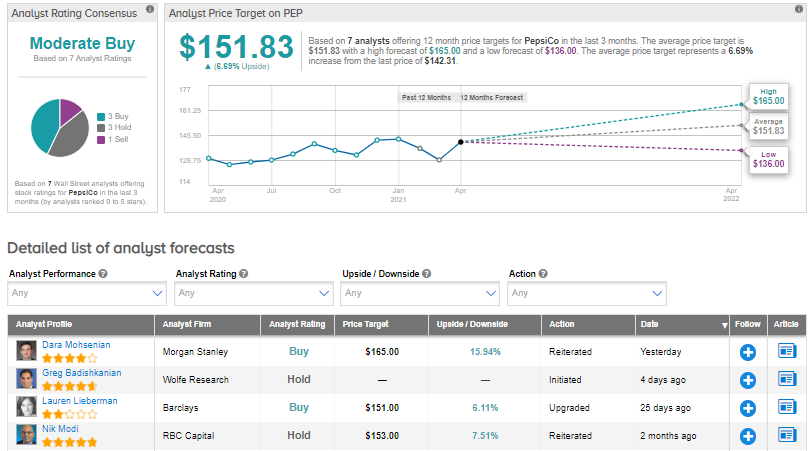

On April 12, Wolfe Research analyst Greg Badishkanian initiated coverage of PEP with a Hold rating on the stock. Badishkanian views “a lot of momentum” behind PEP’s business but believes that the company is “too defensive for the current market”.

Shares have gained 7.4% in the past month.

Consensus among analysts is a Moderate Buy based on 3 Buys, 3 Holds, and 1 Sell. The average analyst price target stands at $151.83 and implies upside potential of 6.7% to current levels.

Related News:

TSMC’s 1Q Results Beat Estimates; Street Says Hold

Kimco Snaps Up Weingarten In Deal Valued At $4B

Dell To Spin-Off 81% Stake In VMware; Shares Pop 8.5%