Every investor’s primary goal should be winning, and the key to success lies in finding the stocks poised to benefit from major trends. In today’s digital economy, two sectors stand out: semiconductors and artificial intelligence. Semiconductors are indispensable, powering everything from computers and tablets to cars and ovens. Meanwhile, AI, the latest breakthrough technology, is rapidly transforming the tech industry and revolutionizing how we interact with machines, unfolding before our eyes in real-time.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Grand View Research projects the AI industry to grow at a compound annual growth rate (CAGR) of over 36% through 2030, with its current market value exceeding $200 billion. Numbers like those tell us where we’re likely to find the best stock choices: among the semiconductor chip companies, particularly those dealing in AI.

Oppenheimer’s Rick Schafer, watching the tech scene, follows this thesis in some of his recent stock picks. The analyst, who is rated by TipRanks at #5 overall on Wall Street, has singled out two AI chip stocks, Nvidia (NASDAQ:NVDA) and Intel (NASDAQ:INTC), for closer consideration. He gives them a deep dive, and is not shy about choosing one as the superior AI stock to buy. Here are the details.

Nvidia

Nvidia is one of the true giants of the tech world. With its market cap of $2.58 trillion, the company is the world’s third-largest publicly traded firm. The company has built itself to this solid position primarily on its dominance of the market for AI-capable, high-capacity processing chips.

These chips have been part of Nvidia’s portfolio for decades. The company is known for inventing the GPU chips that are the ancestors of today’s leading AI and data center processors. First developed for the video gaming niche, the technology proved adaptable and now underlies a wide range of server stack, data center, and AI uses, all fields that rely on high processing speeds and capacities to permit rapid computing.

Earlier this year, Nvidia’s share price reached an all-time high, surpassing $1,100. In response, the company implemented a 10-to-1 stock split in June, bringing the share price down to ~$110. Despite further gains pushing it near $135 by mid-July, the stock has been on a downward trend since then.

Several factors have impacted Nvidia’s share price. Market sentiment has turned cautious, with growing concerns about potential recession indicators. Tech stocks, which have driven recent market gains and are sometimes perceived as overvalued, have consequently faced a pullback. Specific to Nvidia, the company recently announced a three-month delay in the release of its anticipated Blackwell B200 series chips. While Nvidia assures that production ramp-up is on schedule, deliveries are now expected early next year. This delay, despite significant pre-orders from major AI developers like Microsoft, has unsettled investors.

At the same time, Nvidia’s popular H100 chip lines continue to show strong sales, and are expected to pick up the slack during the delay period.

Nvidia will report its fiscal 2Q25 results later this month, and is expected to report revenues of $28.54 billion – an increase of 111% year-over-year – and a non-GAAP bottom line of 64 cents per share.

Despite the recent delay, Schafer remains firmly bullish on Nvidia, believing the stock is well-positioned for continued growth.

“Recent reports indicate NVDA notified MSFT of delays in upcoming Blackwell production ramp, now expected 1Q (vs. prior 4Q)… In our view, impact likely minimal and short-lived (1-2Qs) as current-gen Hopper (30-40% lower ASP) life cycle likely extends to plug the gap… NVDA’s competitive position remains sound, and we don’t expect any share loss from a minor delay. Growing pains to be expected with >5x increase in DC sales Y/Y and shift to annual release cadence. We see NVDA as best positioned in AI, benefiting from full stack AI hardware/software solutions,” Schafer opined.

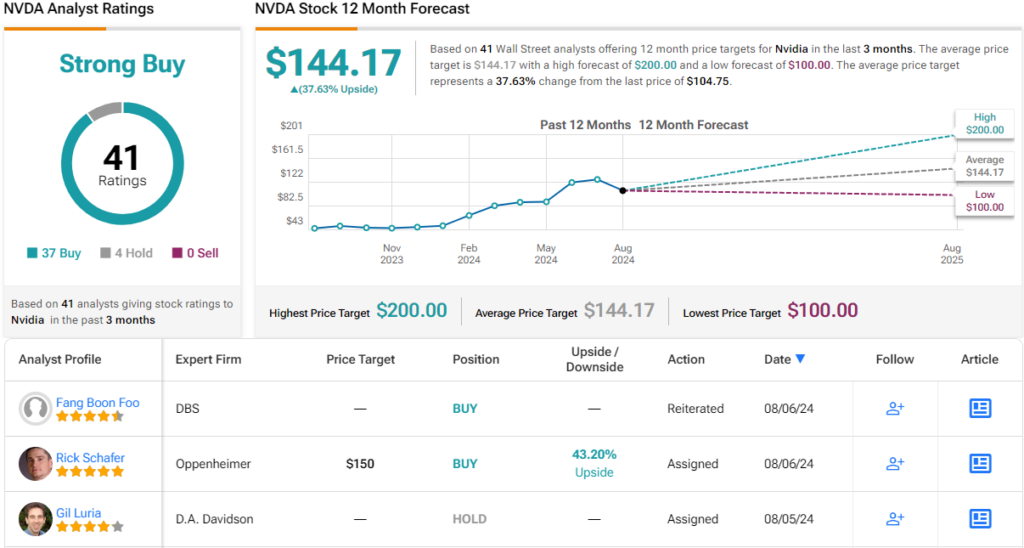

These comments support Schafer’s Outperform (i.e. Buy) rating on NVDA shares, while his price target of $150 implies a one-year potential upside of more than 43%. (To watch Schafer’s track record, click here)

Overall, Nvidia’s stock gets a Strong Buy rating from Wall Street, based on 41 recent analyst reviews that include 37 Buys to just 4 Holds. The shares are priced at $104.75 and their $144.17 average price target points toward a gain of nearly 38% in the year ahead. (See NVDA stock forecast)

Intel

Next up is Intel, a name you’ll almost certainly recognize from the little stickers on the front of your home computer or laptop. Intel’s iCore series chips have long been market leaders in the PC processor segment and are considered the industry standard. That segment leadership has helped support Intel in recent years, even as AI has moved to the forefront of the tech world. While Intel is no longer among the top ten chip makers by market cap, the company still ranks #4 by revenue – and in the last four quarters generated over $55 billion in sales.

Intel wants to remain a leader, however, and that will require a shift in its development and product lines toward AI-capable chipsets – and without losing its strong hold on PC processors. The company has begun to release new AI-capable products, including PC chips capable of supporting AI personal computer applications. Intel brings an important advantage to this projected shift, in that the company is one of the few major chip firms that also handles its own production – and so it has greater control over product lines and lead times and is used to producing semiconductors at an industrial scale and quality.

In addition, Intel has been making a strong commitment to foundry construction. The Federal CHIPS Act made large-scale subsidization available in the chip industry, and Intel has tapped into that to the tune of $8.5 billion. This is supplemented by Federally backed loans totaling $11 billion. This is money on a grand scale, and Intel is using it to build and launch foundry projects in the US – with an emphasis on producing AI-capable CPUs.

Shifts like this are not cheap, and the price is not always measured directly by earnings. In its 2Q24 report, Intel missed on revenues and earnings. The top line of $12.83 billion was down almost a full percent from the prior year and came $150 million short of expectations, while the bottom-line non-GAAP EPS figure of 2 cents per share was 8 cents less than the forecasts. The company shares tumbled as a result, and are still rebounding; INTC is down more than 31% since the earnings release.

Oppenheimer’s Schafer sums up the investor reticence on Intel in clear prose, saying of the company, “After aggressive capital builds, management is pivoting to shore up profitability announcing COGS/Opex/Capex reductions to save $10B in 2025. Headcount reducing by 15%. Share loss and structural shift from traditional CPU-centric compute to AI-accelerated continues to weigh on INTC. Node/foundry investments pressure margins. We remain sidelined as turnaround efforts take root.”

That sideline position equals a Perform (i.e. Hold) rating from the top analyst, and he declines to put a price target on Intel stock until he sees how these tea leaves fall.

The Street in general agrees with the Hold on this stock, as shown by the 31 recent analyst reviews that break down to 1 Buy, 25 Holds, and 5 Sells – a Hold consensus. But the analyst might as well have said “buy” — because, on average, they think the stock, currently at $19.71, could zoom ahead to $27.82 within a year, delivering 41% profits to new investors. (See INTC stock forecast)

For top-ranked analyst Rick Schafer, the choice is clear: Buy Nvidia. It’s clearly the superior AI stock choice at this time.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.