The question frequently raised on Wall Street revolves around whether Tesla (NASDAQ:TSLA) should be classified as an automotive company or as a technology company.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Morgan Stanley’s Adam Jonas has a convenient solution to that issue. Essentially, why should you have to choose between the two?

“In our discussions, many investors still debate the merits of Tesla as ‘more than an auto company,’ the analyst said. “In our opinion, Tesla is definitely an auto company. It is also an AI company. Think ‘and’ not ‘or.’”

Jonas’ comments come at a time of uncertainty for the EV leader. Given growing competition and no new high-volume products set for release in 2024, it’s hardly surprising that investors are cautious on it prospects. Jonas also thinks challenges lie ahead for Tesla’s core auto business next year with the potential for gross auto margin to “test 10%” and the possibility the core OP (operating profit) margin will “flip to negative (for a quarter) in the year ahead.”

Yet, the important bit to note above is that Jonas is referring specifically to the “core auto business.” And as mentioned, in Jonas’ opinion, Tesla is “far more than an auto company.”

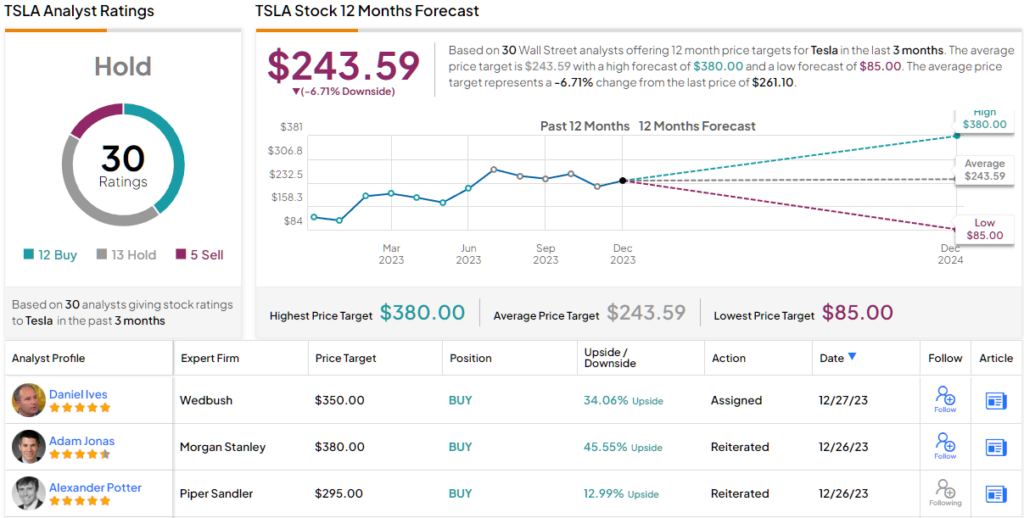

“Of our $380 price target, our valuation of the ‘core’ auto business is $86/share, leaving 77% of our target derived by Network Services, Mobility, 3rd-party battery/FSD licensing, Energy and Insurance,” the analyst explained.

In fact, while Jonas thinks the coming year will represent a struggle for the auto side of the business, there are potentially non-auto catalysts that could have a positive impact. These include Tesla’s AI day (possibly in 1H24) that will be “an important catalyst to introduce and develop new adjacencies for Tesla’s technologies.” That should feature Optimus – the Tesla Bot – that caters to the $30 trillion global labor market and uses the same software architecture as FSD (full self-driving).

The factors that propelled AWS to constitute 70% of Amazon’s overall EBIT could also be at play for Tesla. This has the potential to create opportunities in previously untapped markets beyond the conventional model of just selling vehicles. The catalyst for that? Dojo, Tesla’s custom supercomputing effort the company has been working on for the last 5 years.

Edge AI could also play its part, whereby next gen “software-defined vehicles” might erode the distinctions between the automotive industry and the mobile device market. “Can a car key do more than just open a door? Can a part of the car ‘stay with you?” asks Jonas. “Tesla vehicles are roboticized edge computers.”

So, down to business, what does this all mean for investors? Jonas reiterated an Overweight (i.e., Buy) rating on TSLA, backed by the aforementioned Street-high $380 price target. There’s potential upside of 45% from current levels. (To watch Jonas’ track record, click here)

Not all on the Street, however, are quite as bullish as Jonas. On balance, the stock claims a Hold consensus rating based on a mix of 12 Buys, 13 Holds and 5 Sells. Moreover, the average target stands at $243.59, implying shares will trend ~7% lower over the coming year. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.