Shares of vaccine maker Moderna (MRNA) plunged 17.9% and closed at $284.02 on November 4, after the company reported weaker-than-expected third-quarter results.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Moderna reported diluted earnings of $7.70 per share, significantly lower than analyst estimates of $9.05 per share. MRNA had posted a quarterly loss of 59 cents per share in the same quarter last year.

Furthermore, total revenue came in at $5 billion, missing Street estimates of $6.21 billion.

A major portion of Moderna’s Q3 FY21 revenue came from the commercial sales of its COVID-19 vaccine, with 208 million doses of the vaccine sold during the quarter. However, the sales were not accommodated in the comparable period quarter, resulting in a massive spike in revenue.

See Analysts’ Top Stocks on TipRanks >>

Commenting on the results, Stéphane Bancel, CEO of Moderna said, “It is promising to see the real-world evidence showing that the Moderna COVID-19 vaccine shows sustainably high, durable efficacy… Looking ahead, we are focused on advancing the many other programs in our pipeline.”

Guidance

Moderna has reduced its product sales outlook to be between $15 billion to $18 billion in FY 2021, by reducing the doses delivered in 2021, and shifting it to early 2022. The company expects to deliver a total of 700 million to 800 million doses for the full year, with deliveries affected by longer lead times for international shipments and exports.

Additionally, the company also stated that it has signed around $17 billion of advance purchase agreements (APAs) for delivery in 2022. MRNA forecasts market sales for the commercial booster to be $2 billion, subject to receipt of Biologics License Application (BLA) for boosters.

Moreover, Moderna expects to exercise options of up to $3 billion under 2022 APAs, bringing the total revenue for FY22 to fall in the range of $17 billion to $22 billion.

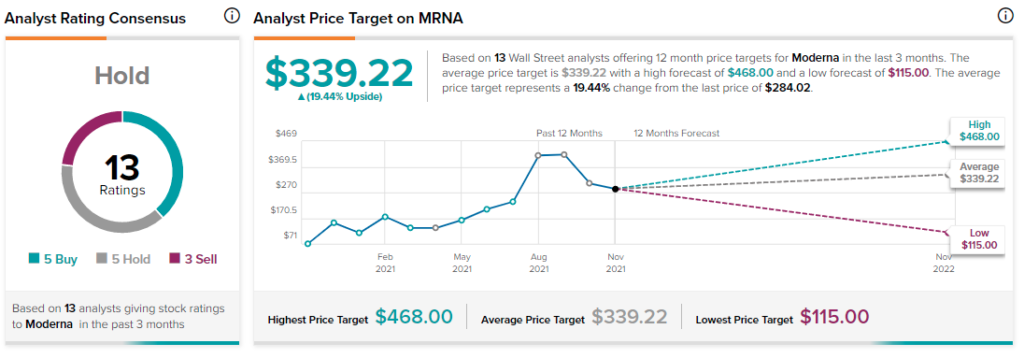

Analyst Recommendation

In response to Moderna’s quarterly performance, Brookline Capital Markets analyst Leah R. Cann reiterated a Buy rating on the stock with a price target of $468, which implies 64.8% upside potential to current levels.

Cann said, “For a company at Moderna’s stage of development, which is largely pre-approval, we primarily focus on potential future revenue to value the company. Based on our expectation that in addition to its already launched COVID-19 vaccine, Moderna will launch several of its development-stage products in the next six years, we estimate that Moderna’s total revenue will increase to $450.5 billion in 2030.”

Cann concluded, “However, we acknowledge the possibility of significant downside to our estimates due to the inherent risks in drug development. Under the worst of these cases, Moderna’s stock could have little value.”

Overall, the stock has a Hold consensus rating based on five Buys, five Holds, and three Sells. The average Moderna price target of $339.22 implies 19.4% upside potential to current levels. Shares have surged by 292% over the past year.

Related News:

Skillz Drops 10% on Quarterly Loss

Qualcomm Posts a Blowout Quarter; Shares Jump 7.5%

Roku’s Q3 Revenues & Q4 Outlook Disappoint