Lockheed Martin 3Q earnings from continuing operation of $6.25 per share rose 10.4% from the year-ago quarter, surpassing analysts’ expectations $6.07. The fighter jet manufacturer’s bottom-line results mainly benefited from sales which grew 8.7% to $16.5 billion and beat the Street consensus of $16.2 billion. Despite the quarterly beat, shares closed 3% lower.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Lockheed Martin (LMT) said that it recorded revenue growth across all its segments. Sales across Aeronautics, Missiles and Fire Control, Rotary and Mission Systems, and Space divisions grew 8.1%, 14.2%, 7.8%, and 6.1%, respectively.

The company boosted its full-year 2020 sales outlook to $65 billion from the previous guidance range of $63.50-$65 billion. Moreover, the company raised its earnings guidance range from $23.75-$24.05 to $24.45 per share. (See LMT stock analysis on TipRanks).

“In the third quarter, our dedicated workforce and resilient supply chain continued to support our customers’ vital national security missions, overcoming the challenges of the pandemic,” said Lockheed Martin’s CEO James Taiclet. “As a result, we delivered strong results across our key financial metrics and we expect to build on this success through the remainder of the year.”

Following its quarterly results, Cowen & Co. analyst Cai Rumohr reiterated his Buy rating as well as a price target of $410 (10.2% upside potential). In a note to investors on Oct. 20, Rumohr wrote, “LMT’s continuing sales/EPS beats, 2020 hikes, and foreign order potential extend prospects for MSD (Management Systems Designers) gains; and its healthy cash flow & flexibility allow continuing HSD (Horizontal Situational Display) dividend hikes. Scarcity value merits its 13.6x 2021 TEV/EBITDAP (Total Enterprise Value/Earnings before income tax, depreciation, interest, amortization and pre-opening expenses less net cash interest expense).”

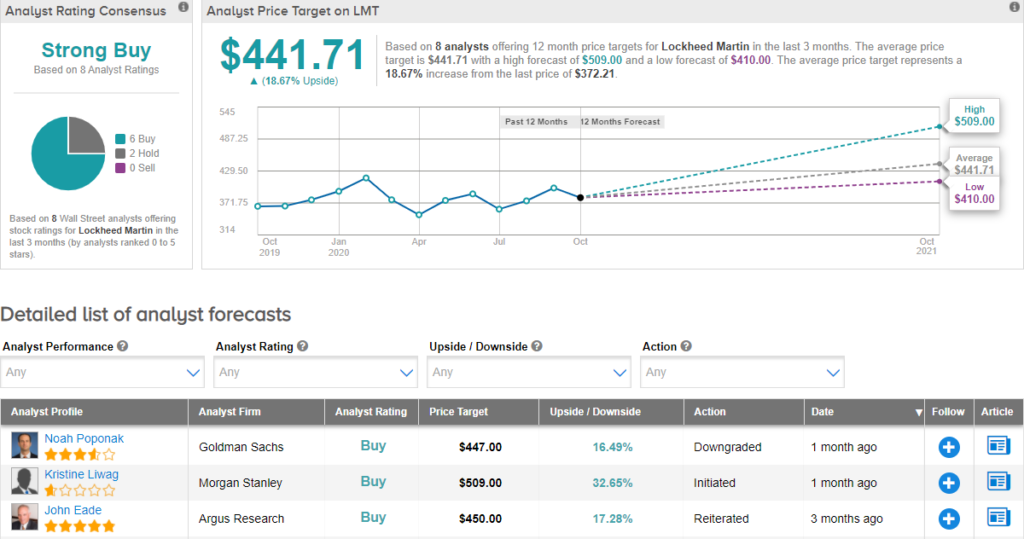

Currently, the Street is bullish on the stock. The Strong Buy analyst consensus is based on 6 Buys and 2 Holds. The average price target of $441.71 implies upside potential of about 18.7% to current levels. Shares have plunged by about 4.4% year-to-date.

Related News:

Simmons’ 3Q EPS Beats Estimates; Analyst Sticks To Buy

Crown Holdings Posts 3Q Profit Win, Initiates Dividend Pay

Zions Beats 3Q Profit; Street Says Hold