Earlier today, Loblaw Companies (TSE: L) (LBLCF) reported its Q2-2022 earnings results for the quarter ended June 18, 2022. Sales reached C$12.85 billion, a 2.9% year-over-year increase, just short of the C$12.98 billion consensus estimate. Meanwhile, adjusted net earnings came in at C$566 million, a 22% increase. Diluted adjusted earnings per share increased 25.2% to C$1.69, beating estimates that called for C$1.61 per share.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

EPS likely grew more than net earnings because of the reduced number of shares outstanding compared to last year; in Q2, Loblaw bought back 5.4 million shares for C$607 million. The company plans to use much of its free cash flow to repurchase shares, going forward. Speaking of which, Loblaw’s free cash flow for its Retail segment reached C$840 million.

In addition, sales from the Retail Segment increased 2.8%, and the segment’s adjusted gross margin increased 50 basis points year-over-year, showing that Loblaw is navigating inflation headwinds relatively well. However, the E-Commerce segment saw a 17.5% decline as a result of hard comparables due to last year’s lockdowns.

The strongest growth was seen from the Financial Services segment, which grew revenues by 9.2%. However, Financial Services saw a loss before taxes of C$86 million, C$114 million worse than the same quarter last year.

Looking forward to the rest of the year, Loblaw expects Retail earnings growth to outpace sales growth and full-year adjusted earnings per common share to grow by a mid-to-high teens percentage.

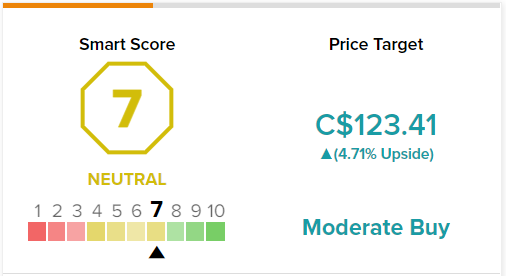

Wall Street’s Take on Loblaw Stock

Turning to Wall Street, Loblaw stock has a Moderate Buy consensus rating based on three Buys and two Holds assigned in the past three months. The average Loblaw stock price target of C$123.41 implies about 5% upside potential. Analyst price targets range from a high of C$133.00 to a low of C$116.00.

One of the Buy ratings came seven days ago from Irene Nattel, a top analyst at RBC (TSE: RY) Capital, ranked #477 out of 21,000 overall experts tracked by TipRanks. Nattel’s price target of C$133 implies 13.1% upside potential from current levels.

Loblaw’s Respectable Smart Score Rating

On TipRanks, Loblaw has a 7 out of 10 Smart Score rating. This is on the high end of a “neutral” rating, meaning that there’s a decent chance of the stock outperforming the overall market, going forward.

Conclusion: Loblaw Continues Its Strong Financial Performance

Loblaw had strong Q2-2022 results, and adjusted EPS beat analysts’ estimates by 5%, while revenue only missed estimates by 1%. The company continues to generate strong free cash flow and will use this cash flow to repurchase shares. Also, its increased gross margin highlights its ability to handle inflationary pressures and supply-chain issues.

Nonetheless, the stock finished down 3.8% today. This is perhaps because investors didn’t like the slight revenue miss, or because Loblaw has already rallied ~15% this year, giving it less upside potential. Indeed, analysts collectively expect mid-single-digit upside potential. Still, Loblaw has been a reliable performer over the years and is a stock to consider.