Love them or hate them, but either way, cars are here to stay. And the current moment is a unique time for automobile buffs. The industry is undergoing a shift, analogous to the original adoption of motor vehicles, as the internal combustion engine gives way to electric drivetrains.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

This shift is occurring concurrently with another significant change: China is expanding its substantial lead over the US as the world’s largest auto market. In 2022, the country saw 23.24 million new vehicle registrations, compared to 13.73 million in the US, and in 2023, the Asian giant took the global lead as the world’s largest vehicle export point of origin.

These facts will naturally draw investors to look at China’s electric vehicles (EVs), and Goldman Sachs analyst Tina Hou follows that thought, and then some. Watching the Chinese EV space, she takes a critical eye, writing, “Against a continuously competitive pricing and tightening funding environment into 2024, we believe OEMs that are able to generate positive profit and cash flow with each vehicle sale will be better positioned in the market to sustain continued R&D investment and, in turn, launch more competitive products into the market.”

Against this backdrop, Hou has taken a deep dive ‘under the hood’ with two leaders in the Chinese EV market and come up with conclusions on these major names, tapping one as the best EV stock to buy. Is it Li Auto (NASDAQ:LI) or NIO (NYSE:NIO)? Let’s take a closer look.

Li Auto

First up is Li Auto, a leader in the Chinese EV sector – and a company that has achieved something of a hat trick in the past year, with solid 12-month growth in revenues, earnings, and share price. Li has managed this the old-fashioned way, by increasing sales in its chief EV lines. The company has several models of EV available in the Chinese market; these include three SUV models, the Li7, Li8, and Li9, and the company is scheduled to launch the Li MEGA this coming March.

Li put its first vehicle into regular production and onto the sales floors back in 2019. Since then, the company has expanded. Its several models feature extended range, always an attractive feature for EVs, and are backed up by a solid service network. As of the end of 2023, Li’s network included 467 retail stores operating in 140 cities across China. The company’s service segment includes 360 service centers and body/paint shops, located in 209 cities.

On the last day of 2023, Li released its December delivery updates. The results should impress industry watchers. Li reported 50,353 vehicle deliveries for the month, exceeding the monthly target and growing 137% year-over-year. The Q4 deliveries came to 131,805, up 184% year-over-year, and the full-year 2023 deliveries were up 182% year-over-year, to reach 376,030. Li’s total deliveries, of all models, have now passed 600K, the highest number among China’s EV makers. This past December marked the ninth month in a row that Li has broken its monthly sales record.

That’s production. On the financial side, Li last reported earnings for 3Q23. The company had a top line of US$4.75 billion, up an impressive 271% year-over-year, and some US$170 million above the forecast. The company’s non-GAAP EPS was listed as 45 cents per diluted share, and the GAAP EPS, at 37 cents per ADS, beat the forecast by 12 cents. Shares in Li Auto are up 63% over the past 12 months.

Solid financials and growing delivery numbers assuaged investor doubts about the Li MEGA, whose launch was delayed from December to March. The MEGA is described as a family-size multi-purpose vehicle, capable of traveling 500 kilometers on a single charge. Deliveries are also scheduled to begin this coming March.

For Goldman’s analyst Hou, this adds up to a company worth another look. She notes the auto maker’s upcoming line-up, and its potential to expand the sales/support network, writing, “We believe the company will have the strongest model pipeline of 5 new launches (4 BEV/1 EREV vs. 3 existing EREV models) and strongest sales network expansion of 400 stores (415 existing stores vs. 994/859/760 for Mercedes/Audi/BMW) in 2024E. We expect the competitive positioning of BEV models and deepening sales network to drive another leg of growth for Li Auto.”

Hou goes on to outline why investors should take a bullish line here: “With continued scale economics and operating leverage, we expect Li Auto to deliver the fastest earnings growth with top-tier free cash flow generation among our China auto OEM coverage. In terms of valuation, Li Auto is currently trading at more than 1-stdev below its historical average 12-month forward P/S and P/E multiples.”

In Hou’s view, all of this adds up to a Buy rating on LI, and her price target, standing at $52.90, implies ~55% share appreciation for the next 12 months. (To watch Hou’s track record, click here)

It’s clear from the analyst consensus that Wall Street is with the bulls on this one. LI has 5 recent positive reviews, giving the stock a unanimous Strong Buy consensus rating. Shares are priced at $34.16, and the $53.58 average target price is slightly more bullish than Hou’s, and suggests a 57% upside potential on the one-year horizon. (See LI stock forecast)

Nio, Inc.

The second stock we’ll look at is Nio, one of the strongest of Li’s competitors in the Chinese EV sector. Nio, like Li, was an early entrant in China’s electric vehicle scene and began moving regular production-line vehicles into delivery in June of 2019. Currently, Nio has 8 electric vehicles on the market, including a mid-sized sedan and both 5- and 6-seat SUV models.

While many of Nio’s vehicle models are designed for family use, the company released its latest model in December, the ET9, a luxury 4-seater sedan described by the company as an ‘executive flagship.’

In addition to its lineup of vehicles, Nio has also emerged as a leader in vehicle ‘accessory’ technologies. The company pioneered Battery-as-a-Service (BaaS), allowing vehicle owners and drivers to swap out batteries at service stations rather than spending hours plugged in at a charging unit. Nio is also working on autonomous driving technologies, including developing an ADaaS option, or Autonomous Driving-as-a-Service. These technologies, which will also encompass driver assistance, aim to improve road safety for vehicle operators, other drivers, and pedestrians alike.

As the New Year opened, Nio released its delivery numbers for December 2023, for 4Q23, and for the full year 2023. At each level, the company showed solid year-over-year increases in vehicle deliveries. For December, the company delivered 18,012 vehicles, a 13.9% year-over-year increase; for Q4, the deliveries totaled 50,045, up 25% year-over-year; and for 2023, Nio deliveries reached 160,038, an increase of 30.7% over the previous year. Overall, since commencing vehicle deliveries to customers, Nio’s total deliveries numbered 449,594 vehicles as of December 31, 2023.

In its last reported quarterly financial results, for 3Q23, Nio showed a top line of US$2.61 billion, up 46.6% year-over-year, although missing the forecast by US$50 million. The company reported a 31 cent loss per ADS; while a loss per share, this was 5 cents narrower than had been expected.

Despite Nio’s strong technology and product line, and its relatively long time putting vehicles on the market, Nio stock shares are down over the past year. The shares have lost 22% in the last 12 months.

Turning to Tina Hou, and her outlook for Goldman Sachs, we find her taking a cautious stance toward the stock. Hou writes of Nio, “As an early mover in China’s NEV industry, we see strengths (1) Nio’s premium brand recognition by the market with high consumer satisfaction and (2) margin tailwinds from battery price decline and at the same time, we see concerns (1) soft growth momentum due to relatively fewer new product launches vs. peers in 2024 and (2) operating expense control and cash flow management. As such, we are Neutral on Nio (ADR/H share).”

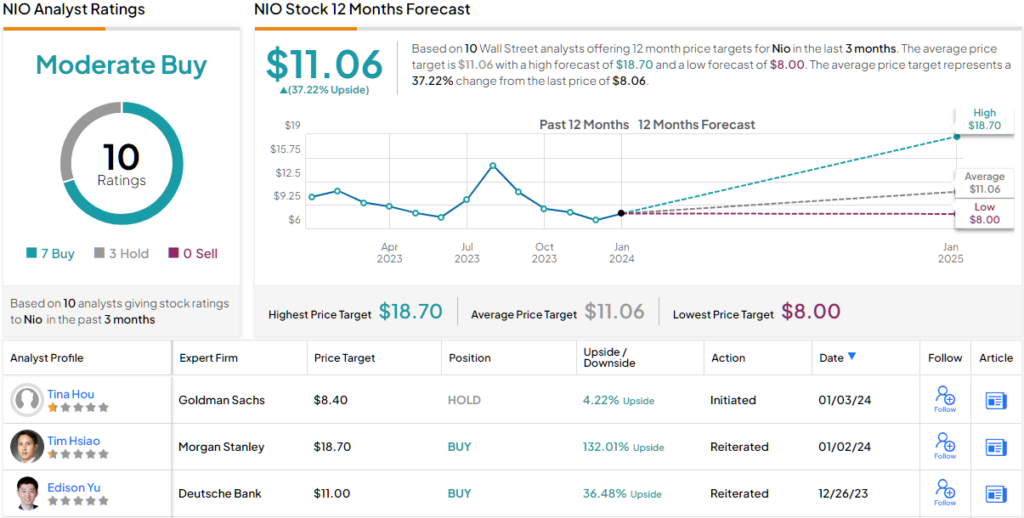

Quantifying these comments, Hou gives NIO a Hold rating, and her price target of $8.40 indicates room for a modest 4.22% upside in the next 12 months.

While Hou is cautious, the Street is still willing to buy in on NIO. The stock has 10 recent analyst reviews, including 7 to Buy against 3 to Hold, for a Moderate Buy consensus rating. The shares have an $11.06 average target price, pointing toward a 37% one-year upside potential from the current trading price of $8.06. (See Nio stock forecast)

After digging into the data, it’s clear that Goldman Sachs is pointing out Li Auto as the Chinese EV stock to buy, edging out its peer competitor Nio.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.