Investors grew weary of Lam Research (NASDAQ:LRCX) after the company reported a mixed forecast for its next earnings report. Indeed, Lam Research projects second-quarter sales of $3.7 billion, give or take $300 million, and gross margins of 45.5% to 47.5%. In addition, earnings per share are predicted to be $6.78, plus or minus $0.75. Shares of the company declined by over 6% in Thursday’s trading. Nevertheless, Wall Street analysts came out to back the company.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

In a note to investors, Citi analyst Atif Malik attributed the reduced guidance to a decline in the equipment market. The analyst, who has a Buy rating and $800 price target on Lam Research, said he expects the margins to normalize by next year.

Meanwhile, Deutsche Bank analyst Sidney Ho pointed to China as the possible catalyst for an improvement in the company’s revenue. Indeed, he does not expect the new export regulations to have any “material impacts” on the company. Ho did note that it is important to keep an eye on the worries over operational costs and gross margins for Fiscal Year 2024, as they may have an effect on earnings per share.

Goldman Sachs analyst Toshiya Hari also joined in on defending Lam Research. Hari described the margin reset for 2024 as a “clearing event.” He clarified that the company’s efforts in backside power distribution, EUV dry resist, improved packaging, and gate-all-around transistors should pay off over the medium to long term.

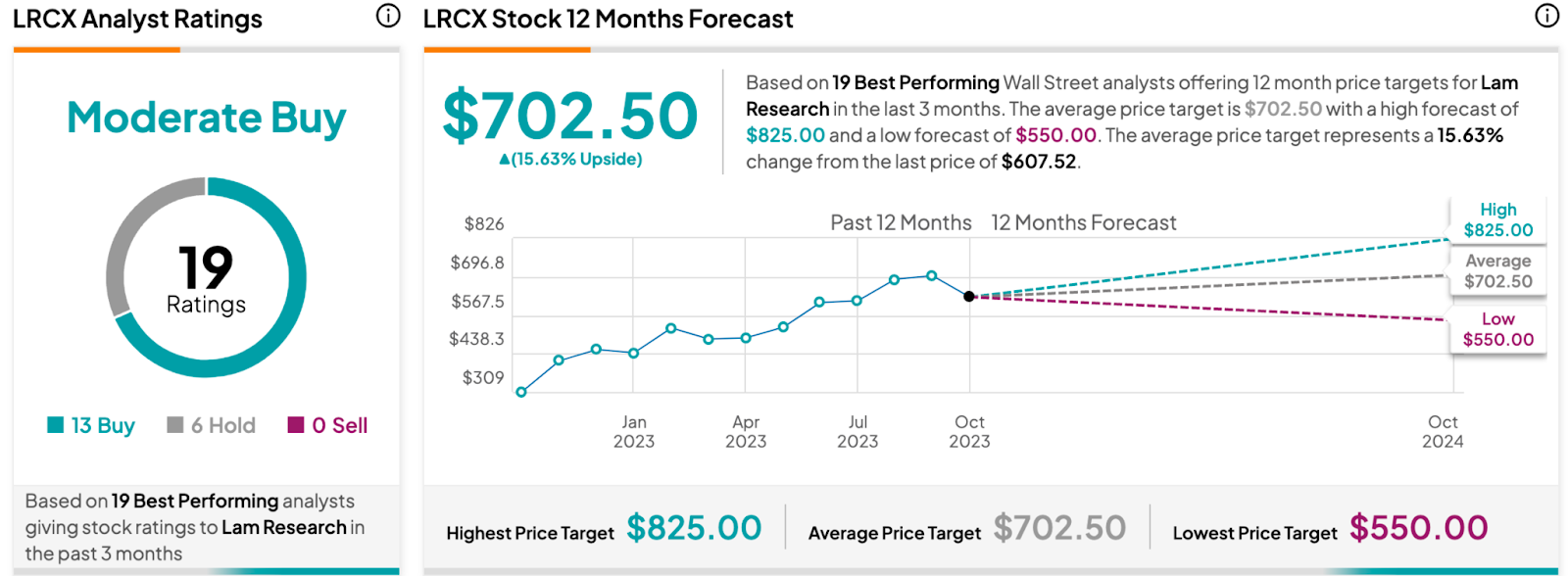

What is the Future of Lam Research Stock?

Turning to Wall Street, analysts have a Moderate Buy consensus rating on LRCX stock based on 13 Buys, six Holds, and zero Sells assigned in the past three months, as indicated by the graphic above. Furthermore, the average LRCX price target of $702.50 per share implies 15.63% upside potential.