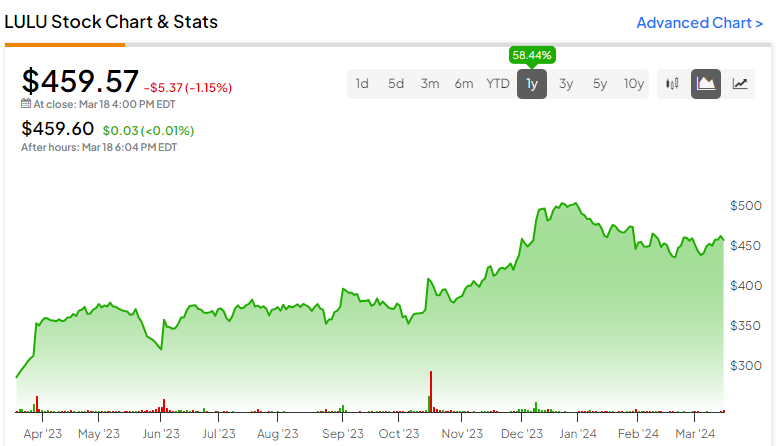

Lululemon (NASDAQ:LULU) is set to release its Q4 earnings report after Thursday’s closing bell. Famous for its high-quality yoga and fitness apparel, Lululemon stock has recorded a 58% gain over the past year. This performance is a testament to investors’ optimistic outlook regarding its growth prospects. Despite valuation concerns at current levels, Lululemon’s growth momentum, brand value, and prospects for continuous expansion could bolster the stock’s bullish sentiment. Thus, I am bullish on the stock.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Q4 Results to Build on Strong Momentum

Lululemon is set to post its Q4 results after this Thursday’s trading session, with numbers likely to build on the strong momentum experienced in previous quarters. Particularly, Lululemon impressed investors in its most recent Q3 results, posting vigorous growth across the board. New store openings took place at an aggressive rate while growing traction in existing locations further boosted the top line. In the meantime, improving unit economics boosted margins, raising future earnings growth expectations.

Let’s take a deeper look.

Aggressive Store Openings, Same-Store Sales Growth Drive Revenue Momentum

In the third quarter, Lululemon posted net revenue growth of 19% to $2.2 billion, driven by aggressive new store openings and increased foot traffic in its existing locations.

In particular, Lululemon’s square footage expanded from 2,390 in Q3 2022 to 2,797 in Q3 2023, an increase of 17%. This was, in turn, the result of the company opening 63 net new stores from last year’s period to a total of 686 locations. In the meantime, top-line revenue was boosted by comparable sales growth, which came in at 13%. This was, in turn, driven by same-store sales growth of 9% and direct-to-consumer net revenue growth of 18%.

Anecdotally, I made a delightful stop at a Lululemon boutique in Hong Kong to pick up gifts for my loved ones. Besides being shocked by Hong Kong’s spending culture (a subject worthy of its own discussion), I found myself pleasantly surprised by how packed the store was. The line at the checkout stretched for about five minutes. It certainly reflected the vibrant numbers seen in Lululemon’s numbers.

Improving Unit Economics Boosts Earnings Growth Momentum

With Lululemon’s same-store sales growing, the company’s unit economics improved once again. Rising sales against fixed overhead costs, such as rent, naturally result in economies of scale. Thus, Lululemon’s adjusted operating income margin expanded by 80 basis points to 19.8%.

The notable increase in revenues, coupled with a noteworthy margin expansion, led to adjusted earnings per share landing at $2.53 for the quarter. This pushed the first-nine-months adjusted earnings per share to $7.49, up 32% compared to last year’s $5.67.

What to Expect in Q4

After a strong Q3 characterized by strong revenue growth and even more vibrant earnings growth, the company’s growth is expected to remain robust in Q4. Management’s guidance forecasts Q4 net revenue of between $3.135 billion and $3.170 billion, which suggests growth between 13% and 14%. Further, Wall Street’s consensus estimates for the quarter point to adjusted earnings per share of $5.02, suggesting a year-over-year increase of 14.1%.

Is LULU Stock Overvalued?

To assess whether Lululemon stock is a Buy before its Q4 report, it’s crucial to consider its valuation. Given that shares have rallied by about 58% over the past year, it’s only natural to assume that Lululemon could be overvalued at its current levels. That said, I believe that Lululemon’s brand value, growth prospects in international markets, and the possibility of expansion into additional product categories justify its forward P/E of about 34x.

Specifically, the net revenue growth of 19% I mentioned earlier can be broken down to an increase of 12% in North America and an increase of 49% internationally. I guess this incredible international growth also matches my experience in Hong Kong. In any case, it certainly implies that the company has notable potential outside of the U.S. Even if we assume that international growth gradually decelerates, double-digit growth rates abroad are likely to be a multi-year, if not multi-decade, trend.

Additionally, the company can leverage its brand strength to diversify into new product categories, thus extending its trajectory of growth. A prime example is the company’s venture into the footwear industry in 2022. Today, the company has even penetrated the coats and jackets market, with more new categories gradually appearing in stores and online.

In that sense, I find the stock’s forward valuation to be reasonable. Assuming one doesn’t care too much about how the market’s post-earnings reaction and the stock’s short-term movement in general, I believe that Lululemon’s long-term investment case remains compelling. Thus, the stock could be a decent Buy before its Q4 results get released.

Is LULU Stock a Buy, According to Analysts?

Turning to Wall Street, Lululemon has a Moderate Buy consensus rating based on 15 Buys, three Holds, and two Sells assigned in the past three months. At $516.16, the average Lululemon stock price target implies 12.31% upside potential.

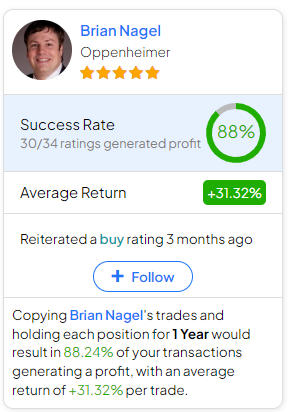

If you’re seeking guidance on which analyst to track when it comes to trading LULU stock, the most accurate analyst covering the stock (on a one-year timeframe) is Brian Nagel from Oppenheimer, with an average return of 31.32% per rating and an 88% success rate. Click on the image below to learn more.

The Takeaway

Based on Lululemon’s previous results and management’s guidance, the company’s impending Q4 results stand to build upon the ongoing momentum. With new stores opening at an aggressive rate and existing stores gaining increased traction, revenue growth is set to remain in the double digits. Simultaneously, as unit economics improve, earnings growth is poised to land at an even faster pace.

While this year’s tremendous share price might deter some investors from considering the stock, I believe that the valuation remains fair when considering Lululemon’s growth potential and overall qualities. Thus, those planning to hold shares for the long term could find that buying Lululemon stock before earnings is a worthwhile trade—especially assuming the company beats consensus estimates, which it usually does.