Growth investing strategies, like looking for buyable growth stocks, are popular for a reason—and Dell Technologies (DELL) might just be one to consider. When done with a focus on quality and a long-term perspective, growth investing has the potential to help investors build life-changing, generational wealth.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

What do I mean by quality? I look for businesses that are firmly established within their industries. It’s easier to achieve strong revenue and earnings growth in sectors that consistently expand, which is another factor I prioritize in potential investments. I also insist on investment-grade balance sheets.

This brings me to Dell Technologies. After reviewing the company’s recent earnings report and growth catalysts, I believe it could be a worthwhile growth stock to buy now. Here’s why.

Dell Posts a Sizable Double Beat

One reason for my bullish sentiment on Dell stock is its Fiscal second quarter financial results for the period ended August 2nd. The company posted $25 billion in net revenue for the quarter, up 9.1% from the prior year. For context, that was $910 million ahead of analysts’ expectations. Strong growth in the company’s Infrastructure Solutions Group segment (e.g., data storage, AI servers, and cloud services) easily offset a slight revenue decline in the Client Solutions Group segment (i.e., workstations, PCs, and monitors).

Dell’s non-GAAP diluted EPS surged 8.6% year-over-year to $1.89 for the Fiscal second quarter, significantly surpassing the analyst consensus of $1.71. CFO Yvonne McGill noted that an AI-optimized server mix and more competitive pricing led to a 230 basis point decline in gross margin to 21.8% of revenue for the quarter. This was partially offset by a nearly 2% reduction in the share count, which led bottom-line growth to roughly match top-line growth for the quarter.

Dell Becomes an Increasingly Prominent AI Play

Dell’s outlook further supports my Buy rating on the stock. Each quarter, the company becomes more of an AI play. In the past year, the quickly growing Infrastructure Solutions Group segment rose from nearly 37% of revenue in Q2 2024 to almost 47% in Q2 2025—a nearly 10 percentage point swing. The company envisions its total addressable market expanding from $1.2 trillion in 2019 to $2.1 trillion by 2027, driven by segments like servers and storage.

On a more company-specific level, Dell is performing reasonably well. AI infrastructure shipments almost doubled quarter-over-quarter, and the company has shipped $6.5 billion in AI infrastructure over the past 12 months. Additionally, Dell’s five-quarter pipeline of prospective shipments is several multiples of its backlog. As these are converted into actual shipments, this should boost growth.

That’s why the analyst consensus is for non-GAAP diluted EPS to surge 10% in FY 2025 to $7.84, followed by a 19.4% increase to $9.36 in FY 2026. An additional 14.9% rise in non-GAAP diluted EPS to $10.75 is currently projected for FY 2027.

Dell Delivers Market-Beating Dividend Growth

On the dividend front, Dell further supports my bullish perspective. Dell’s 1.4% dividend yield is marginally higher than the 1.3% yield of the S&P 500 Index (SPX). The company’s dividend is also quite safe, with a non-GAAP diluted EPS payout ratio expected to remain in the low 20% range in FY 2025. This payout ratio arguably places Dell in a position to deliver on its targeted 10%+ annual dividend growth rate from FY 2024 through FY 2028. That would make the stock not only a respectable source of immediate income but also of strong dividend growth.

Dell Has a Healthy Balance Sheet

Dell is also a financially stable company, which provides additional support for my bullish stance. As of August 2nd, the company’s core leverage ratio improved to 1.4x. For perspective, this is a substantial improvement from Fiscal year 2020, when the core leverage ratio was 3.2x. This is why Dell holds an investment-grade BBB credit rating from S&P Global (SPGI).

Shares Offer Decent Value

Although shares of Dell have surged 83% so far in 2024, there’s still arguably a value proposition supporting my positive view of the stock. Shares are trading at a current-year P/E ratio of 16.7. For a business with a path to low double-digit annual non-GAAP diluted EPS growth for the foreseeable future, this could represent moderate undervaluation in my view.

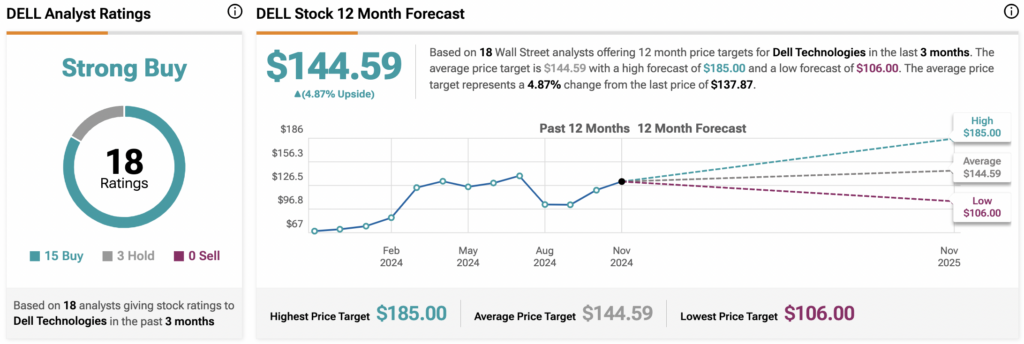

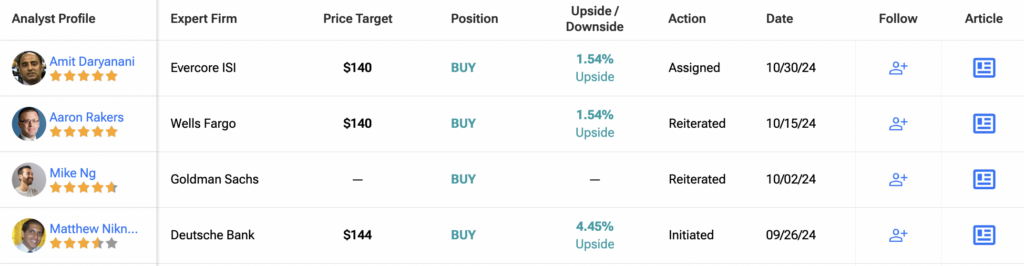

Is DELL Stock a Good Buy, According to Wall Street?

Shifting to Wall Street, analysts have a Strong Buy consensus on Dell, based on 15 Buys and three Holds. The average 12-month DELL price target of $144.59 suggests 5% upside potential.

Key Takeaway

Dell may not always steal the spotlight from its larger tech peers, but that’s exactly why I find it a compelling “growth at a reasonable price” (GARP) investment. GARP stocks blend the potential for growth with relatively modest valuations, offering a balanced approach that can mitigate some of the risks of traditional growth investing. Dell’s Infrastructure Solutions Group is thriving, likely supporting solid earnings growth for years to come. Plus, its dividend is well-covered with room for future increases, and the company has significantly reduced its leverage ratio. Given these strengths, I’m initiating coverage on Dell with a Buy rating.