Legendary investor Warren Buffett is known for his wisdom. One of my favorite quotes from him is: “If you don’t find a way to make money while you sleep, you will work until you die.”

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Pharmaceutical company AbbVie (ABBV) is the latest stock in my portfolio to announce a higher dividend. Accompanying its third-quarter earnings report, AbbVie declared a 5.8% increase in its quarterly dividend, taking the distribution up to $1.64 per share. Despite what I thought was a solid quarter, the stock’s valuation seems to have already priced in near-term upside. For this reason, I rate ABBV stock a Hold.

AbbVie’s Strong Financial Results

While I rate ABBV stock a Hold, there’s no denying the company reported strong third-quarter financial results. The company’s revenue increased by 3.8% from a year ago to $14.5 billion. Adjusting for unfavorable foreign currency exchanges, operational revenue grew by 4.9% during the quarter. This was fueled by strength from medications Skyrizi and Rinvoq in the immunology portfolio, Venclexta in oncology, and Botox Therapeutic and Vraylar in neuroscience. AbbVie’s adjusted earnings per share (EPS) increased 1.7% year-over-year to $3. That topped the analyst consensus by $0.08.

AbbVie’s third-quarter results look to be a preview of what’s ahead for the company. As mentioned, it is benefiting from significant momentum in its key prescription drugs. Skyrizi and Rinvoq are poised to exceed $17 billion in combined sales in 2024, which is $1.3 billion ahead of AbbVie’s initial expectations.

Skyrizi’s impressive clinical results have allowed it to achieve in-play biologic share leadership in 30 key countries in psoriatic disease. Rinvoq’s tremendous efficacy has fueled double-digit in-play patient share in the U.S. for ulcerative colitis and Crohn’s disease.

A Promising Future

Despite my Hold view, I acknowledge that AbbVie has a promising future. The company’s amazing one-two immunology punch has room to keep growing. That’s because Skyrizi’s total prescription share of Crohn’s disease is 8% globally and has room to expand. The drug is also in the early phases of its launch in the U.S. and Europe for ulcerative colitis. Given the positive feedback from gastroenterologists, it’s likely that Skyrizi will also shine in the ulcerative colitis area. Rinvoq’s positive data from its second head-to-head study versus Dupixent could help it gain more share in the atopic dermatitis market.

The rest of AbbVie’s product portfolio, including Venclexta, Botox Therapeutic, and Vraylar are no slouches either. The pharmaceutical company also possesses a pipeline of 90+ compounds or indications that position it for a variety of product launches over the next decade. This is why the analyst consensus is that earnings per share (EPS) will rise by 10.9% in 2025 to $12.11. A further 11.6% increase in EPS is expected in 2026.

AbbVie’s Dividend

The last positive thing I can say about AbbVie is that its dividend is strong and growing. The 3.2% dividend yield on ABBV stock dwarfs the 1.3% average yield among stocks listed on the benchmark S&P 500 index (SPX). The stock also provides shareholders with excellent dividend growth. In the last five years, AbbVie’s quarterly dividend per share has compounded by 39%, representing a 6.8% compound annual growth rate (CAGR).

Looking ahead, mid-single-digit annual dividend growth should continue to be the norm for ABBV stock. This is because AbbVie’s dividend payout ratio is poised to register growth in the mid-50% range in 2025. That payout ratio strikes a great balance between returning capital to shareholders and leaving enough capital to execute share repurchases, repay debt, and complete acquisitions.

In its latest earnings call, AbbVie executives reiterated that the company is going to pay down $7 billion of debt in 2024. That puts the company on pace to attain its targeted net leverage ratio of 2x by the end of 2026. This financial fortitude explains why S&P Global (SPGI) maintains an A- credit rating and a stable outlook on AbbVie.

The Valuation’s High

Now we come to the main reason why I rate ABBV stock a Hold, its valuation. AbbVie is undeniably a strong business. But the valuation has gotten extreme, especially after a 7% rally in the share price since the company’s third-quarter print. AbbVie’s forward price-to-earnings (P/E) ratio of 16.7 is above its 10-year average of 13.2.

Even accounting for the boom years of Humira drug sales skewing earnings higher and the P/E ratio lower, this seems to be excessive to me. Realistically, I think that a valuation multiple of between 14 and 15 would be fair for AbbVie.

Is ABBV Stock a Buy?

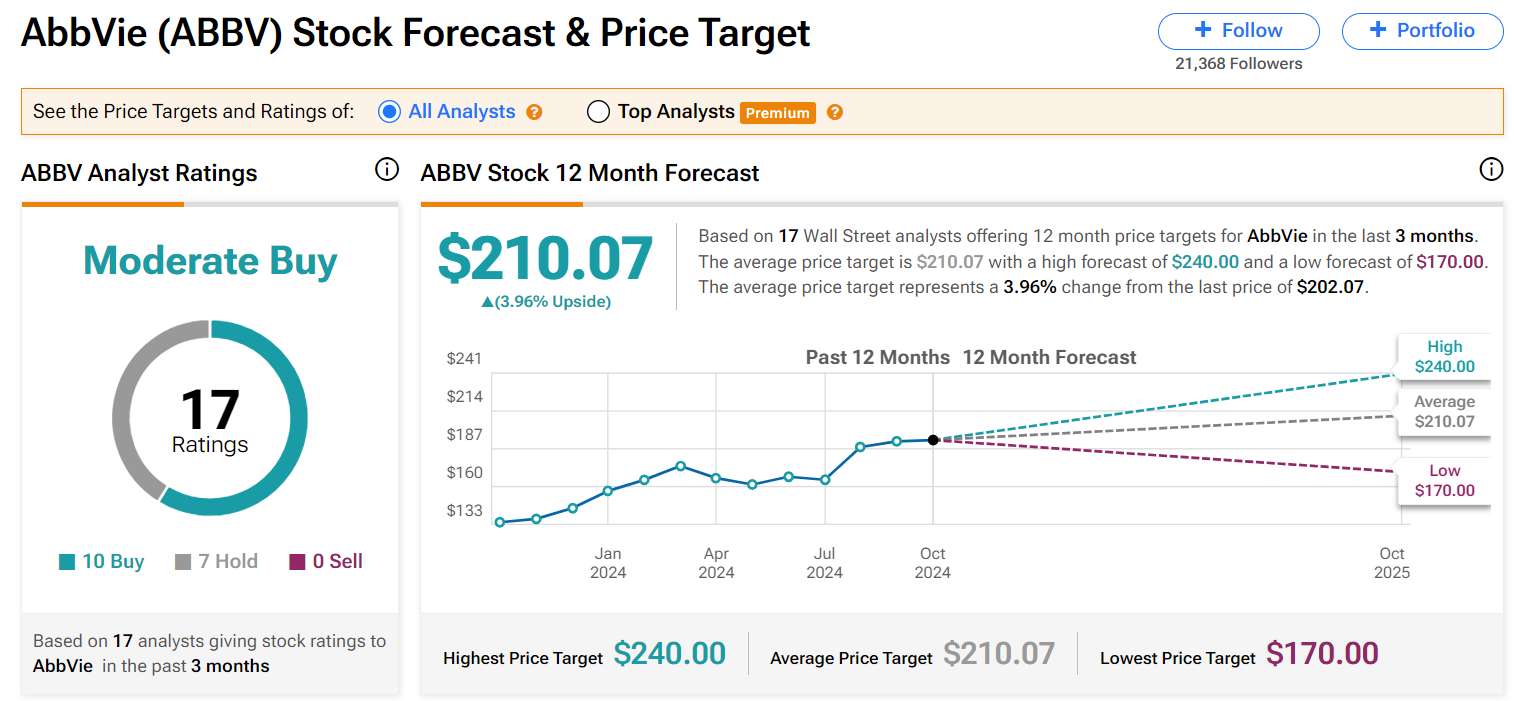

Turning to Wall Street, analysts have a Moderate Buy consensus rating on AbbVie stock. Out of 17 analyst ratings in the past three months, 10 have assigned Buys and seven have assigned Holds. There are no Sell ratings on the stock. The average ABBV price target of $210.07 implies 3.96% upside from current levels.

Read more analyst ratings on ABBV stock

Conclusion

AbbVie is thriving as a business. The company’s most important drugs are gaining market share and look poised to keep growing sales. AbbVie’s dividend is sustainable, and the balance sheet is impressive. Unfortunately, the valuation of the stock is running high currently, which is why I rate it a Hold at present levels.