Chinese video streaming platform iQIYI (IQ) has announced that its Q1 GAAP EPS of -$0.56 fell short of Street estimates by $0.02 due to an advertising pullback. Online advertising services revenue for the first quarter was RMB 1.5 billion, down 27% year-over-year, primarily due to the challenging macroeconomic environment in China related to the virus situation.

However, revenue of $1.1B reflected year-over-year growth of 9% and topped Street forecasts by $80M. Shares are currently sinking 4% in Tuesday’s pre-market trading.

Operating loss was RMB2.2B ($316.6 million) and operating loss margin was 29%, compared to RMB2 billion and operating loss margin of 29% in the same period in 2019.

The number of total subscribing members surged to 118.9 million as of March 31, 2020, 99.2% of whom were paying subscribing members. This compares to 96.8 million of total subscribing members at the end of March 2019, up 23% year over year.

“We delivered solid results during the first quarter despite very challenging environment caused by the COVID-19 outbreak,” commented Dr. Yu Gong, CEO of iQIYI. “The advertising industry faced huge headwinds as the pandemic caused setbacks in many industries, which, in turn, adversely impacted our advertising business. As a result, our overall advertising revenues softened during the first quarter.”

Looking forward, he expects Q2 and the full year will still be under pressure. “Q2 ad revenues could see slightly sequential recovery but will be down year-over-year, especially now that some of our variety shows will likely be pushed out to Q3 or even Q4 as their production process was delayed due to the pandemic” Dr. Yu Gong explained.

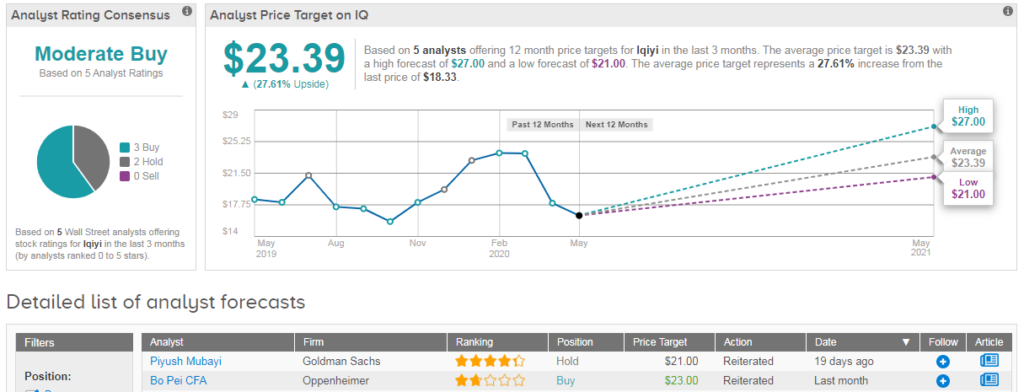

iQIYI scores a cautiously optimistic Moderate Buy Street consensus, with 3 recent buy rating and 2 hold ratings. The $23 average analyst price target indicates 27% upside potential, with the stock down 13% year-to-date. (See IQ stock analysis on TipRanks).

“We believe IQ will continue to produce high-quality content and double its subscriber base in five years” comments Oppenheimer analyst Bo Pei, who has a buy rating on the stock. The analyst notes that IQ is still early in overseas markets, and sees expansion in Southeast Asia as another potential growth driver.

Related News:

Baidu Pops 8% After-Hours On Strong Earnings Beat

Uber Pops More Than 6% On Second Round Of Layoffs, Site Closures

Ray Dalio Picks Up These 3 “Strong Buy” Stocks