IBM Corp. (IBM) reported better-than-estimated profit in the second quarter driven by sales of its cloud computing business sending shares up almost 5% in extended market trading on Monday.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

The stock surged to $132.25 in Monday’s after-market trading. IBM’s total revenue in the second quarter dropped 5.4% to $18.12 billion year-on-year, coming in above analysts’ estimates of $17.72 billion. Adjusting for the impact from currency and divested businesses, revenue slipped 1.9%. Meanwhile total cloud revenue surged 30% to $6.3 billion in the reported quarter.

Excluding items, the company earned $2.18 per share, exceeding analysts’ expectations for $2.07 per share. IBM’s focus of investment has been its hybrid cloud transition and AI as clients modernize their businesses and need to enhance their work-at-home capabilities in today’s COVID-19 environment.

“Our clients see the value of IBM’s hybrid cloud platform, based on open technologies, at a time of unprecedented business disruption,” said IBM CEO Arvind Krishna. “We are committed to building, with a growing ecosystem of partners, an enduring hybrid cloud platform that will serve as a powerful catalyst for innovation for our clients and the world.”

IBM ended the second quarter with $14.3 billion of cash on hand which includes marketable securities, up $5.2 billion from year-end 2019. Debt, including global financing debt of $21.9 billion, totaled $64.7 billion. The company returned $1.5 billion to shareholders in dividends.

“Our prudent financial management in these turbulent times enabled us to expand our gross profit margin, generate strong free cash flow and improve our liquidity position,” said IBM CFO James Kavanaugh. “We have the financial flexibility to continue to invest in our business and return value to our shareholders through our dividend policy.”

Shares in IBM, which have climbed 6% in the past 5 days, are still down 5.7% year-to-date.

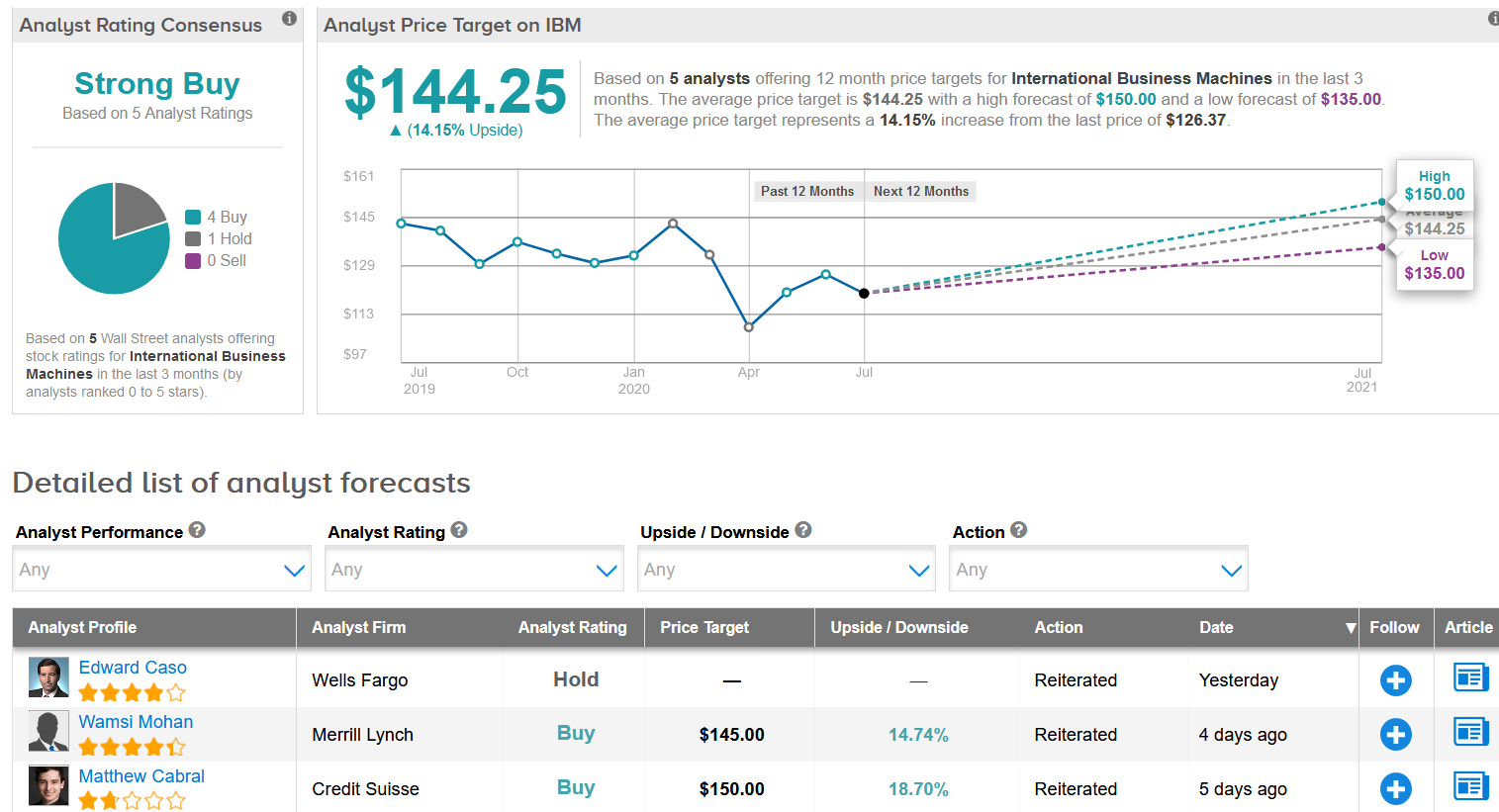

Merrill Lynch analyst Wamsi Mohan reiterated a Buy rating on the stock with a $145 price target, saying that the company benefits from the transition to a hybrid cloud.

“We expect COVID-19 impact to pressure Global Technology Services (GTS) revenues but expect margins to start to improve following the Q1 restructuring charge,” Mohan wrote in a note to investors. “However, while near term trends will be scrutinized, we think the more important catalyst will be an update from CEO Arvind Krishna at a later point in 2H20.”

The analyst believes that IBM remains attractive with a 5% dividend yield and as he expects the CEO to potentially articulate his vision to drive growth some time this year.

“A refocus on growth and investments should drive a positive rerating in the valuation multiple,” he added.

Turning now to the rest of the Street, analysts share Mohan’s bullish outlook. The Strong Buy consensus breaks down into 4 Buy ratings versus 1 Hold rating. The $144.25 average price target suggests shares have 14% upside potential in the coming 12 months. (See IBM stock analysis on TipRanks).

Related News:

Apple iPhone SE Boosts Q2, But Unlikely To Cannibalize 5G Sales – Report

Ebay On Cusp Of Selling Classified-Ads Unit To Adevinta – Report

Amazon Exports From India-Based Sellers Crosses $2B Mark – Report