IBM (IBM) is going into its earnings report after a strong rally this year. The big question is whether software strength can keep pushing the stock higher. The stock has surged 30% this year, outpacing the Nasdaq Composite’s 19% gain. Investors are looking for evidence in the report that IBM’s software growth still has room to run.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Wall Street expects IBM to post $16.1 billion in revenue and $2.45 per share in adjusted earnings for the September quarter. Looking ahead, consensus calls for $19.2 billion in revenue and $4.33 EPS for the December period.

A clean beat and upbeat tone on recurring software growth could extend the rally. However, a miss or vague commentary might remind investors how quickly expectations can shift when sentiment runs hot.

Analysts Highlight Software and Red Hat Growth

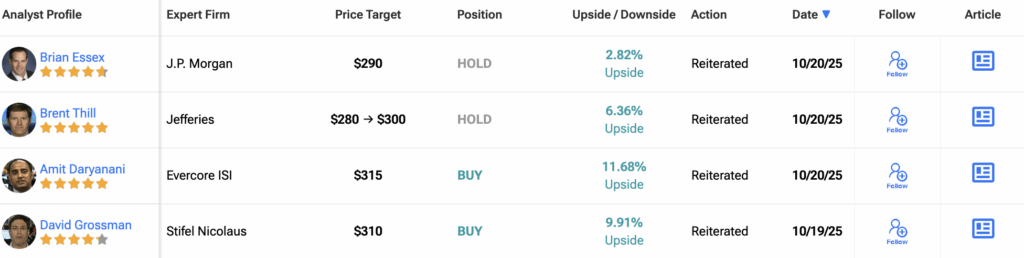

Jefferies analyst Brent Thill reaffirmed a Hold rating and lifted his price target to $300 from $280, citing software momentum and execution strength.

“While some of the software upside is priced in with the recent stock rally, we think IBM can grind higher if fundamentals strengthen in 2H,” Thill wrote.

IBM’s Red Hat business remains a key driver, powering hybrid cloud adoption through its OpenShift platform. Meanwhile, automation services are helping enterprise clients modernize workloads and improve efficiency.

If IBM offers solid data on customer retention and subscription growth, investors are likely to reward that transparency.

Guidance and Cash Flow Remain in Focus

IBM’s full-year outlook calls for at least 5% revenue growth in constant currency and over $13.5 billion in free cash flow. Investors will be looking for either a raise in guidance or confirmation that these targets remain firmly intact.

Additionally, strong cash generation continues to be IBM’s safety net. It allows management to fund buybacks, dividends, and targeted acquisitions that strengthen the software portfolio. Even steady guidance could reassure markets that IBM’s rally is grounded in fundamentals, not just enthusiasm.

What to Watch after the Print

After such a sharp rally, IBM’s valuation now demands proof. The key questions all point back to execution. Can software growth remain steady and broad-based? Are Red Hat and automation scaling fast enough to justify the premium investors are paying? And will improving mix and efficiency finally show up as operating leverage in 2026? A clean set of answers would reinforce confidence that IBM’s turnaround is real and durable. But if progress looks uneven, the stock could pause while fundamentals catch up to expectations.

Is IBM a Good Stock to Buy?

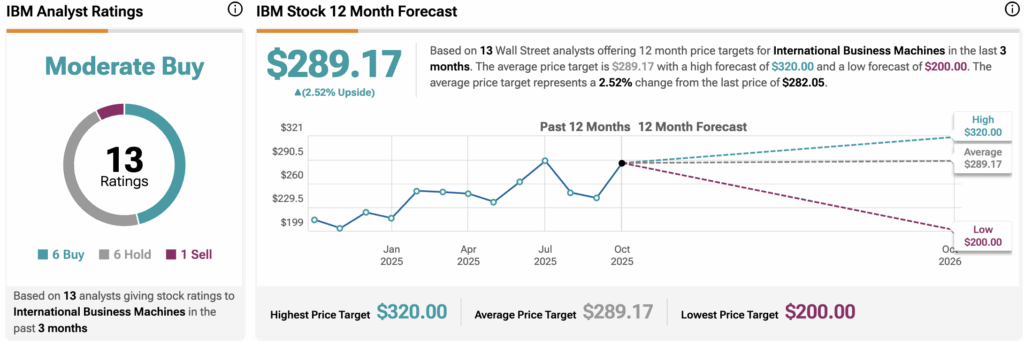

Currently, Wall Street maintains a Moderate Buy consensus on IBM stock, based on 13 analyst ratings over the past three months. The breakdown includes six Buy calls, six Holds, and one Sell recommendation.

The average 12-month IBM stock price target sits at $289.17, implying a modest 2.5% upside from current levels.