On April 30, 2024, Super Micro Computer (NASDAQ:SMCI) released its Fiscal Q3 results (for the quarter ended March 31). While each of the preceding quarterly results — over the past year — had contributed to the stock’s phenomenal bull run, these results were different. In fact, the stock dropped considerably. Nonetheless, I’m undeterred and expect the stock to push higher. I remain bullish on SMCI stock, noting its robust growth trajectory, commanding position within the market, and improving free cash flow over the long run.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Why Is Super Micro Computer So Important?

Super Micro Computer has become an important enabler of the artificial intelligence (AI) revolution. The San Jose-based company makes rackmount servers and graphics processing unit (GPU) servers. It also makes motherboards, chassis, ethernet switches, and adapters. And through partnerships with chipmaker Nvidia (NASDAQ:NVDA), its AI-centric servers provide optimal performance and integration for AI workloads.

The AI revolution has driven a vast amount of demand for rack-scale plug-and-play total AI solutions. These supercomputers provide customers like Amazon (NASDAQ:AMZN) and Google (NASDAQ:GOOGL) (NASDAQ:GOOG) with market-leading AI infrastructure that can drive machine learning algorithms and deep learning models, as well as data-demanding cloud storage.

The company’s first-to-market approach has been central to its success, providing server solutions that push the boundaries of what modern technology can do. Key to this is the firm’s direct liquid cooling (DLC) technology, which ensures optimal system performance while delivering up to 40% energy cost saving at data center scale. DLC is many times more efficient than conventional air cooling systems, as liquid is 23.5x more efficient in transferring heat than air.

“Strong demand for AI rack scale PnP solutions, along with our team’s ability to develop innovative DLC designs, enabled us to expand our market leadership in AI infrastructure,” Charles Liang, SMCI’s president, said in a statement.

Super Micro Computer’s Revenue Miss

Super Micro beat earnings expectations for its third quarter of FY2024. Non-GAAP EPS of $6.65 beat the consensus by $1.08. The company also raised its full-year revenue guidance and adjusted its profit outlook positively. However, after quarter-on-quarter of outperformance, investors clearly expected more in terms of sales. Total revenue for the quarter came in at $3.85 billion, underperforming the consensus by $50 million.

Liang put some of this underperformance down to supply chain constraints. “Fiscal Q3 net revenue totaled $3.85 billion, up 200% year-on-year, within our aggressive original guidance of March quarter. If not limited by some key component shortages, we could have delivered more,” Liang said in the earnings call.

While investors reacted positively in after-hours trading — the stock jumped as high as 10.4% — it slumped when the market opened. Seemingly the market had very high expectations for Super Micro or thought the stock was priced for perfection.

It’s also worth noting that the stock pulled back on April 19 after the company delivered a press release without preliminary figures. In seven of the last eight quarters, Super Micro had disclosed preliminary data before its quarterly results. These updates had often been positive, guiding above the original consensus.

Long-Run Demand for Super Micro’s Services

The recent surge in demand for AI-enabling technology appears to just be the tip of the iceberg. According to forecasts from Omdia, revenues from the cloud and data centers for the AI processor sector will reach $37.6 billion in 2026. That’s up from $6.9 billion in 2021. Omdia says that compound annual growth will be equal to 45.2% for the years 2020-26. I haven’t seen a forecast that looks further into the future, but I’d expect a strong growth rate to be sustained.

SMCI’s Valuation Remains Attractive

Super Micro trades at 32.4x forward earnings. That certainly sounds expensive. However, given long-term demand expectations and expanding margins and free cash flow following the current investments in production capacity, earnings growth is forecasted to be very strong. In fact, analysts suggest that the company’s earnings will grow by 46.7% annually over the next three to five years. In turn, this leads to a price-to-earnings-to-growth (PEG) ratio of 0.7x (a PEG ratio under 1.0x is generally seen as undervalued).

Is Super Micro Computer Stock a Buy, According to Analysts?

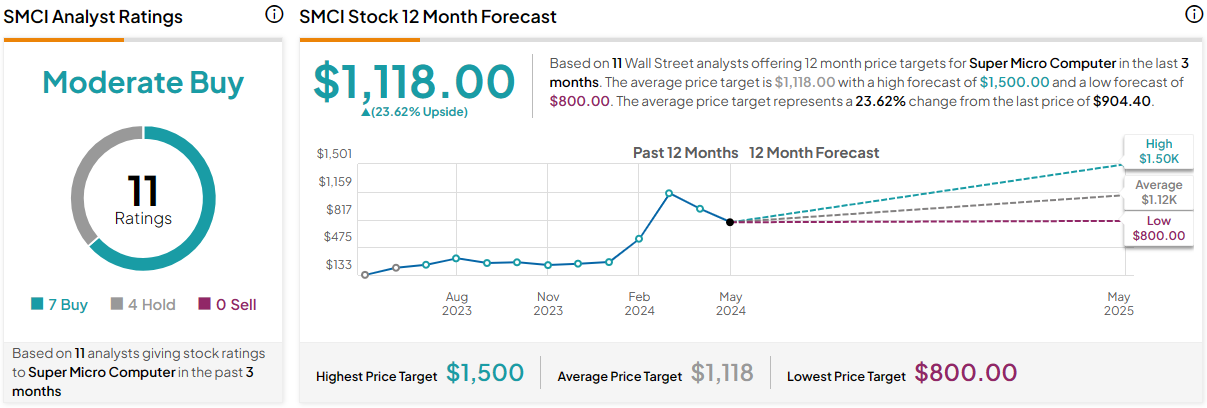

Super Micro Computer stock is a rated Moderate Buy, according to the ratings of 11 analysts offering 12-month price targets. There are currently seven Buys and four Hold ratings. The average Super Micro Computer stock price target is $1,118.00, with a high forecast of $1,500 and a low forecast of $800. The average price target represents 23.6% upside potential.

The Bottom Line on Super Micro Computer Stock

Super Micro Computer might have experienced some supply chain constraints in the previous quarter, but this doesn’t impact the long-term picture for me. The stock is trading with highly attractive multiples and is expected to grow earnings at a staggering rate over the coming three to five years. Moreover, the stock has pulled back from its highs and now has 23.6% upside potential.