The recently reported results of China’s e-commerce giant Alibaba (HK:9988) disappointed investors, as the company missed revenue and profit estimates for the fiscal third quarter. Even the announcement of a $25 billion increase to the company’s share repurchase plan through March 2027 failed to boost investor sentiment. Amid the ongoing pressures, analysts patiently await a turnaround, with Alibaba taking several initiatives to boost its core businesses.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Alibaba’s Recent Results

Alibaba’s revenue grew 5% year-over-year to RMB260.3 billion in 2023, lagging analysts’ consensus expectation of RMB261.3 billion. Net profit declined 69% to RMB14.43 billion due to unfavourable mark-to-market changes related to the company’s equity investments and impairments associated with its Youku video streaming service and Sun Art supermarket chain.

Alibaba faced multiple headwinds last year, including macroeconomic challenges and heightened competition from PDD Holdings’ (NASDAQ:PDD) Pinduoduo and TikTok-owner ByteDance. Moreover, the company cancelled the highly-anticipated spin-off of its cloud computing business.

Alibaba formed six business groups in 2023 and said that it would pursue an initial public offering for some of the units. However, the company now thinks that the ongoing market conditions are challenging and do not “reflect the true intrinsic values of these businesses.”

Alibaba’s CEO, Eddie Wu, stated that the company’s top priority is to revamp the growth of its core businesses, which are e-commerce and cloud computing. The company also aims to boost its investments to enhance users’ experience and drive growth of the Taobao and Tmall Group.

Is Alibaba a Buy, Sell, or Hold?

Following the results, DBS analyst Tsz Wang Tam reiterated a Buy rating on Alibaba with a price target of HK$133. Tam expects the Taobao and Tmall division’s revenue to slowly rise in the next few quarters, supported by increased order frequency, gross merchandise value, and take rate.

Further, Tam believes that Alibaba’s International business will be the key growth segment for the company in the medium term.

Likewise, UOB Kay Hian analyst Julia Pan Meng Yao reiterated a Buy rating on 9988 shares with a price target of HK$100. However, the analyst noted that investors are now worried about the subdued e-commerce top-line growth, soft cloud revenue growth of 3%, and pressure on margins due to the company’s significant investments.

Meanwhile, Mizuho analyst James Lee thinks that while the $25 new buyback plan is encouraging, Alibaba’s business transition could take some time. Lee reaffirmed a Buy rating on Alibaba stock but lowered the price target for the company’s U.S.-listed shares to $95 from $100.

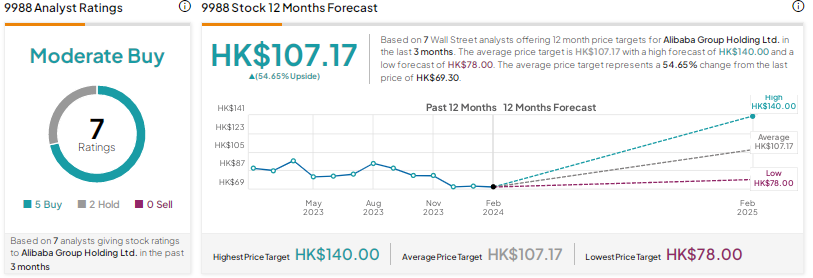

Overall, with five Buys and two Holds, 9988 stock earns a Moderate Buy consensus rating. The Alibaba share price target of HK$107.17 implies about 55% upside potential. Shares are down 33% over the past year.

Conclusion

Alibaba’s recent results reflected weakness in the company’s e-commerce business due to increased competition and macro pressures. Moreover, the lacklustre growth of the Cloud unit is concerning. While the company is trying to reignite its business, analysts expect the turnaround to take time. Nonetheless, most analysts remain bullish on Alibaba’s long-term growth potential.