Tesla (NASDAQ:TSLA) investors just can’t seem to catch a break.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

Just as hopes were buoyed by Elon Musk’s announcement of an upcoming Tesla “robotaxi” launch, shares of the electric car pioneer got hammered when the U.S. Department of Labor reported that inflation is running hotter than projected, dashing investor hopes of a stock market-inflating round of Fed interest rate cuts.

Of course, it doesn’t help that Wall Street analysts continue to cut price targets on Tesla, throwing cold water on any investor enthusiasm for the stock. The latest of these price target cuts just came out from Piper Sandler, where analyst Alexander Potter has cut his valuation for Tesla stock to $205 a share.

Potter cites several reasons for his PT cut. First and foremost is of course Tesla’s admission, last week, that its Q1 deliveries were only 386,810, below analyst forecasts and an 8.5% decline year over year. But second is Potter’s worry that this is not a singular bump in the road for Tesla, but rather indicative of weak demand for the company’s EVs over the rest of 2024, and 2025 as well.

“Growth is slowing,” says Potter, “and there’s no quick fix,” with Tesla blaming everything from high interest rates to seasonality of demand, to factory downtime depressing sales – and Potter suggesting that “EV skepticism, coupled with Chinese competition and an aging product portfolio” are also weighing on demand. As a result, Potter predicts Tesla will miss its deliveries target for 2024 as a whole, in addition to missing in Q1 in particular, delivering fewer than 1.8 million electric cars this year, a 0.5% decline from 2023. Worse, because Tesla has been cutting prices on the cars it does sell, in an effort to goose demand, revenues for the company will fall even more than deliveries – down about 3.3% year over year.

All this being said, however, Potter continues to rate Tesla stock as Outperform (i.e. Buy), and his $205 price target actually implies that Tesla stock will go up ~20% this year. (To watch Potter’s track record, click here)

As the analyst explains, once Tesla begins delivering low-cost “Model 2” EVs, and scales up its high-margin Cybertruck business, its delivery “issues” should disappear by about 2026.

Moreover, bigger picture, the analyst is most optimistic about Tesla’s full self-driving software business, which he believes has the potential to generate 50% or more of Tesla’s gross profits over the long term. Fact is, Potter argues that Tesla’s actual car business is only worth about $80 a share – such that at today’s $176 share price, nearly $100 of the company’s value is represented by future hopes that it can make money selling self-driving software for its (and perhaps other companies’?) cars.

The good news: Potter values “FSD” at roughly $30,000 per Tesla user who decides to pay for it, once the company has overcome the “technical, psychological, and regulatory hurdles associated with autonomous vehicles,” and built FSD into a sustainable business.

The bad news: Investors will probably need to wait a decade to find out if Potter was right on this call.

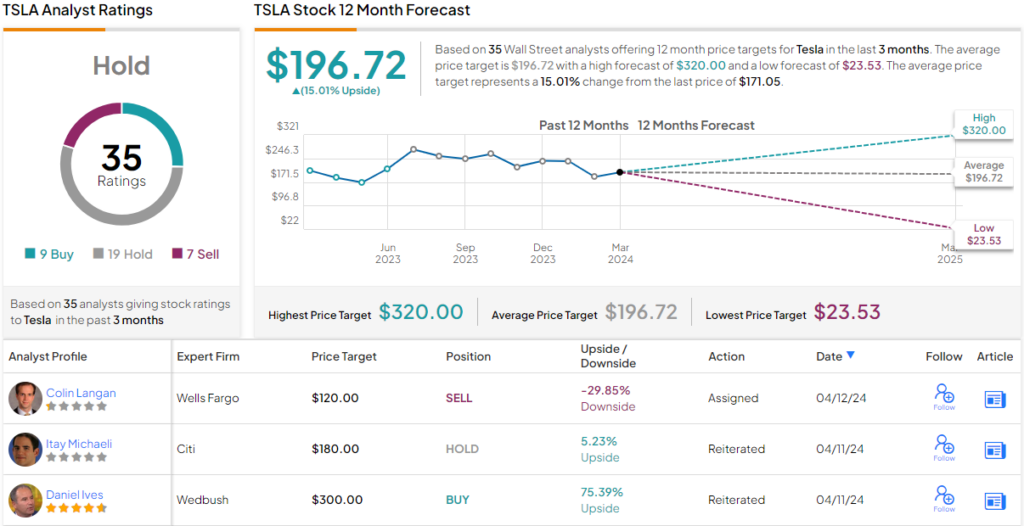

Ultimately, the word on the Street points to a sidelined majority on Tesla. In the last three months, the EV maker has received 9 Buy ratings, 19 Holds, and 7 Sells. It’s clear that Wall Street is largely divided when it comes to Tesla’s market opportunity. That said, the consensus average price target points to $196.72, or nearly 15% upside potential for the stock. (See TSLA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.