Having your earnings release before the open on Monday can be quite the mood-setter. Fortunately for SoFi (NASDAQ:SOFI), its latest quarterly statement set a positive tone for the subsequent proceedings.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Shares saw out the session up by 20%, after the neo bank came good on its promise to swing to profitability in the quarter. The company generated net income of $48 Million, compared to a loss of $40 million in the same period a year ago. That translated to GAAP EPS of $0.02, surpassing the Street’s expectation for a break-even quarter.

At the top-line, the company generated record revenue of $594.25 million, amounting to a 34% year-over-year increase and beating the consensus estimate by $22.74 million. The beat was boosted by increasing its fair value mark on personal loans from 104% in Q3 to the fourth quarter’s 104.9%.

Looking ahead, the company is calling for 2024 revenue between $2.404 – $2.444 billion. That was roughly in-line with the expectations of Wedbush analyst David Chiaverini, implying a mid-teens revenue growth rate. That, says the analyst, represents a “notable slowdown” from the ~35% revenue growth seen in 2023.

The company also laid out its longer-term vision, expecting 20% to 25% compound revenue growth through 2026, although Chiaverini thinks the new 2026 guide is “more aspirational than achievable.”

“When taken in the context of longer-term compounded revenue growth rate goals, it implies a significant step-up in 2025/26 growth, which we fear could be difficult to achieve,” the analyst explained. “Even though the company is now GAAP profitable, we believe capital constraints could limit lending segment growth, and we fear the implied growth in the tech segment may not be enough to offset this.”

Slowing lending segment growth is one concern while “potential continued degradation in credit quality” is another. Regarding that, there was a rise in the embedded loss rate assumption for SOFI’s personal loan portfolio in Q4, from 4.6% to 4.8%. Additionally, the net charge-off (NCO) rate increased to 4% in the fourth quarter, vs. Q3’s 3.4%. “We fear credit quality could continue to normalize and perhaps weaken beyond the 4.8% loss rate embedded in the FV marks,” Chiaverini said on the matter.

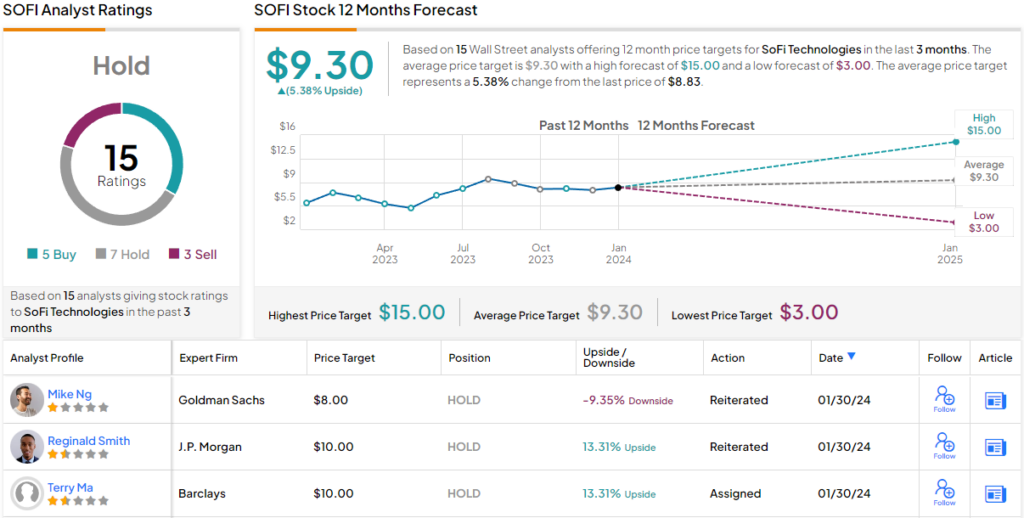

In light of these factors, Chiaverini remains the Street’s most prominent SOFI bear, assigning it an Underweight (i.e., Sell) rating and a price target of $3. This reflects a substantial 67% decline from the current share price. (To watch Chiaverini’s track record, click here)

Joining Wedbush’s bearish outlook, two other analysts share a negative sentiment, while seven recommend a Hold and five suggest a Buy, resulting in a consensus Hold rating. With an average price target of $9.30, it appears that the shares are currently considered almost fully valued. (See SoFi stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.