DocuSign (NASDAQ:DOCU) shares are in focus today after the e-signature solutions provider delivered a better-than-expected performance for the third quarter. Revenue increased by 9% year-over-year to $700.4 million, exceeding estimates by about $10 million. Moreover, EPS of $0.79 outperformed expectations by a wide margin of $0.16.

Meet Your ETF AI Analyst

- Discover how TipRanks' ETF AI Analyst can help you make smarter investment decisions

- Explore ETFs TipRanks' users love and see what insights the ETF AI Analyst reveals about the ones you follow.

During the quarter, Billings increased by 5% year-over-year to $691.8 million, and Subscription revenue ticked up by 9% to $682.4 million. However, the company’s revenue from Professional services declined by 16% to $18.1 million.

Impressively, the company’s free cash flow for the quarter soared to $240.3 million compared to $36.1 million in the year-ago period. In addition, a new engineering center in India is expected to help DocuSign tap top talent and accelerate critical data-focused product innovation.

For Fiscal Year 2024, DocuSign expects total revenue to hover between $2,746 million and $2,750 million. Billings for the year are anticipated between $2,835 million and $2,845 million. For the upcoming quarter, the company expects total revenue in the range of $696 million to $700 million.

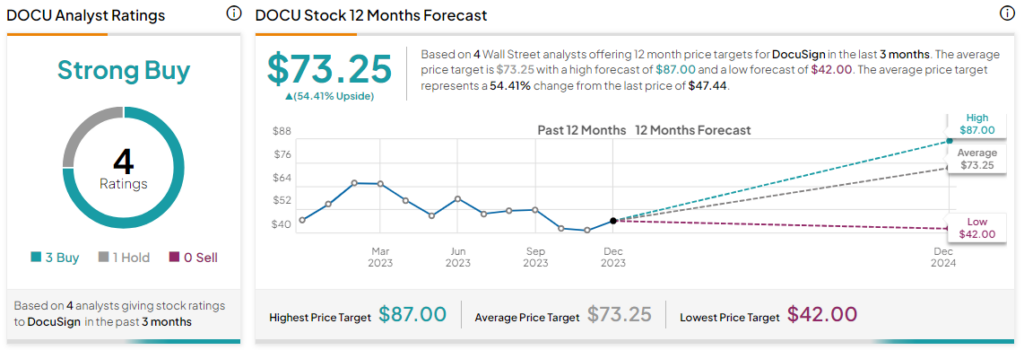

What is the Forecast for DOCU Stock?

Following this performance, JMP Securities’ Patrick Walravens reiterated a Buy rating on DocuSign alongside a $84 price target. Walravens views the stock favorably owing to, “Strategic leadership hires, improving customer acquisition value, and early signs of stabilization in consumption across various sectors.”

Overall, the Street has a Strong Buy consensus rating on DocuSign. Shares of the company have run up nearly 16% over the past month, and the average DOCU price target of $73.25 implies a further 54.4% potential upside in the stock.

Read full Disclosure