Thursday is shaping up to be another bad day for PayPal (NASDAQ:PYPL), as the digital payments leader grapples with a roughly 11% decline in its shares. Despite surpassing expectations on both revenue and earnings in its 4Q23 report, PayPal experienced a decline in active accounts. Furthermore, the company’s guidance fell short of expectations, contributing to investor disappointment.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

In the quarter, revenue climbed by 8.1% year-over-year to $8 billion, coming in $130 million above the Street’s call. At the opposite end of the scale, adj. EPS of $1.48 outpaced the analysts’ forecast by $0.12. There were other strong metrics. Total payment volume (TPV) saw a 15% increase (13% FXN) to $409.8 billion, while payment transactions per active account rose by 14% to 58.7.

However, on the negative front, total active accounts dropped from 435 million at the end of 2022 to 426 million. And looking ahead, for 2024, the company expects adjusted EPS of ~$5.10, about the same as last year, and falling below Wall Street’s forecast of $5.53. For Q1, PayPal expects mid-single-digit EPS growth. That should see the figure land at ~$1.23, below consensus at $1.26.

This is a period of transition at PayPal with new CEO Alex Chriss aiming to re-accelerate the company’s growth. Investors might be showing disappointment with how that is going so far, but Goldman Sachs analyst Michael Ng believes the company is making the right noises and thinks the cautious outlook might turn out to be a good thing eventually.

“In our view,” said the analyst, “the quarter was relatively balanced with 2024E estimates being sufficiently conservative and setting up PYPL to potentially beat numbers throughout the year on better opex discipline and new product contributions (which isn’t reflected in the guidance). We’re also encouraged by PYPL’s new disclosures around TPV growth (e.g., PSP, branded checkout, and Venmo), incorporation of SBC as an expense in adjusted results starting in 1Q24, and commitment to returning another $5.0 bn to shareholders through repurchases in 2024E.”

Summing up, Ng reiterated his Buy rating on PayPal shares, stating, “We believe that PayPal’s consumer brand trust and ongoing PayPal investment in value-added features should support PYPL’s current market share position, with opex efficiencies (relative to historical levels) that should position PYPL for strong performance when ecommerce growth strengthens back to historical DD% growth rates.”

That Buy rating comes with a $74 (down from $80) price target, suggesting the shares will surge 32% over the coming year. (To watch Ng’s track record, click here)

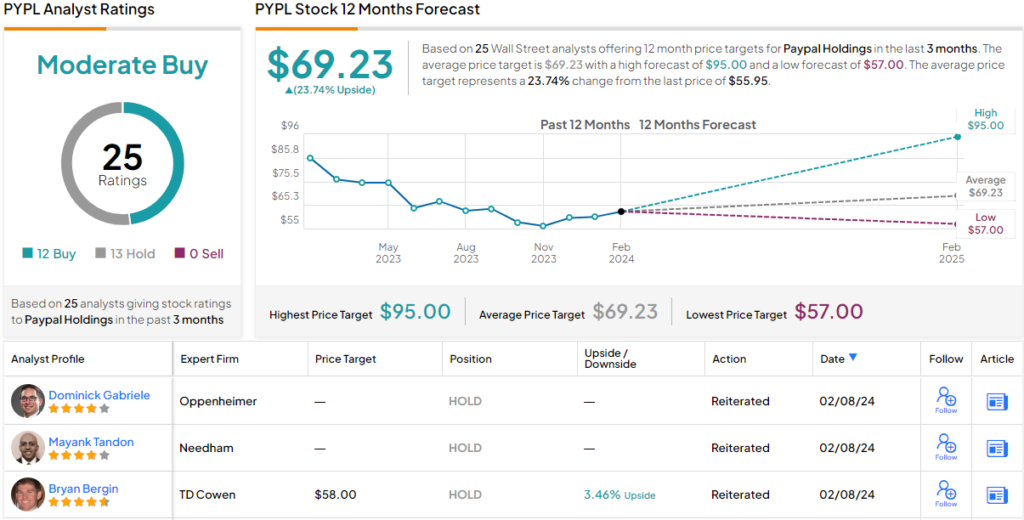

Among Ng’s colleagues, the PYPL bulls and conservatives are almost evenly matched. Based on 12 buys and 13 holds, the stock claims a moderate buy consensus rating. Going by the $69.23 average price target, a year from now, the shares will be changing hands for ~24% premium. (See PayPal stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.