SoFi Technologies (NASDAQ:SOFI) has delivered the goods for investors in 2023. Boosted by the high interest rate environment and the end of the student loan moratorium, the shares have recorded gains of 111% throughout the year.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

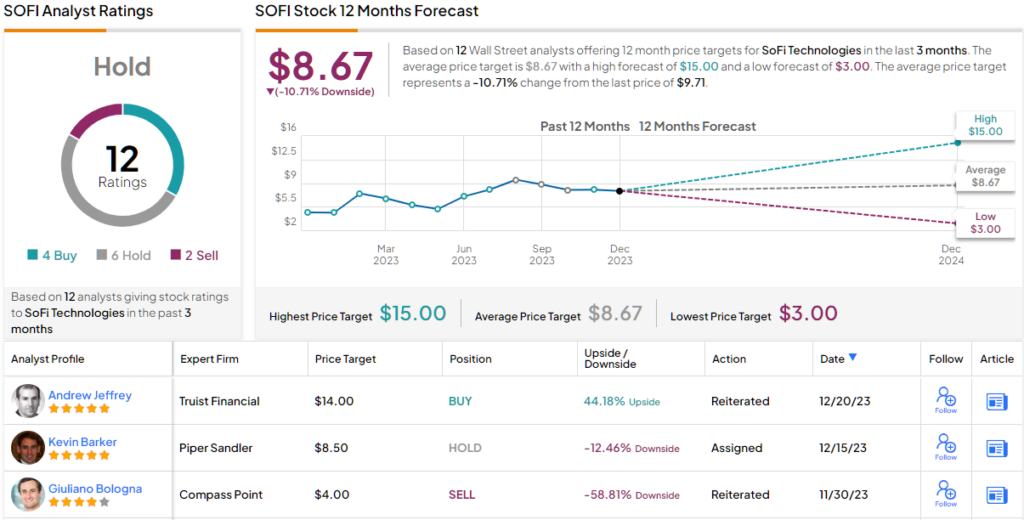

The good news, according to Truist’s Andrew Jeffrey, a 5-star analyst rated in the top 1% of the Street’s stock pros, is that there’s plenty more room for the stock to run in 2024. In addition to maintaining a Buy rating, Jeffrey has set a $14 price target on SOFI, implying that further growth of 44% lies ahead. (To watch Jeffrey’s track record, click here)

That target, says Jeffrey, is “roughly consistent” with SOFI’s C24E valuation. “We see the multiple supported by durability of SoFi’s profit model, despite slower C24E loan growth after two years of rapid expansion,” the 5-star analyst explained. “We argue earnings quality improves as mix shifts to non-Lending. While some may push back on modestly lower EBITDA, we submit SoFi is being prudent given uncertain macro/regulatory. We believe our estimates are conservative and expect greater long-term contribution from non-Lending.”

Following C23E loans out of ~$22 billion compared to just ~$6 billion at in 2021, Jeffrey believes SOFI is happy with keeping a ~7% Personal Loan market share.

While Jeffrey thinks there’s plenty of capital to support loan growth of $12 billion-$14 billion in C24E, he anticipates the company will hold loans “roughly flat.” The result of which will be ~10% NII (net interest income) growth, some distance below his +26% estimate and far lower than the Street’s +37% forecast.

So, is that a bad thing? Not necessarily. “We see this Lending downshift consistent with regulatory uncertainty during a period of higher-for-longer rates,” he explained. “Although Bears may argue SoFi is capital constrained, we think this is wrong.”

Meanwhile, Jefferies believes it is the non-Lending investments that “underpin long-term earnings power.” Until now, the analyst thinks SoFi has been satisfied achieving approximately three times the Lifetime Value to Customer Acquisition Cost (LTV/CAC) ratio through its Financial Services Productivity Loop (FSPL). This approach has led to total products reaching ~10.5 million, with a year-over-year increase of 45% in 3Q23. But to drive faster product growth to be monetized in the future, in 2024, Jeffrey expects the company to “accelerate investment,” all the while keeping an incremental EBITDA margin of 30% or more. “This Fin Product investment is facilitated by improving segment profitability, in our opinion, as the company drives adoption and scale,” Jeffrey elaborated.

So, that’s Truist’s view, what does the rest of the Street have in mind for SOFI? On balance, it’s a rather more subdued take. Based on a mix of 4 Buys, 6 Holds, and 2 Sells, the analyst consensus rates the stock a Hold. The average target stands at $8.67, implying the shares will fall by ~11% in the year ahead. (See SoFi stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.