Bristol Myers Squibb (NYSE: BMY), a global biopharmaceutical company, has posted better-than-expected results for the first quarter of 2022. Results reflected strong growth in In-line products, increased acceptance of its new product portfolio, and a strong execution on a commercial basis.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Despite the beat, shares of the company declined 2.5% to close at $75.27 on Friday on management’s expectations of reduced revenue from its cancer drug Revlimid and lower adjusted EPS for 2022.

Results in Detail

Bristol Myers Squibb recorded adjusted earnings of $1.96 per share, ahead of the consensus estimate of $1.94 per share. The company reported adjusted earnings of $1.74 per share in the same quarter last year.

Total revenues generated during the quarter stood at $11.65 billion, up 7% year-over-year, and came in above analysts’ expectations of $11.42 billion.

Interestingly, U.S. revenues grew 10% year-over-year to $7.7 billion, while adjusted International revenues jumped 3% to $4 billion, driven by elevated demand mainly for drugs Eliquis and Opdivo.

On a segment basis, revenues for In-line products grew 8% to $8.3 billion, while New product portfolio revenues more than doubled to $350 million.

Gross margin came in at 79.2%, up from 78.1% in the prior-year quarter, mainly driven by foreign exchange impact.

While marketing, selling, and administrative expenses surged 10% year-over-year to $1.8 billion during the quarter, research and development expenses reflected a rise of 2% to $2.3 billion.

Pipeline Update & Guidance

In a press release, the CEO of Bristol Myers, Giovanni Caforio, said, “We continue to execute against our strategic priorities, deliver solid revenue and earnings growth and advance our product pipeline…we achieved regulatory approvals of Opdualag and Camzyos, our new first-in-class medicines for patients living with metastatic melanoma and symptomatic obstructive hypertrophic cardiomyopathy, respectively.”

“These milestone achievements, combined with our promising product pipeline and strong financial flexibility, provide a solid foundation that will enable us to deliver sustained growth and long-term benefits for our patients,” Caforio added.

For 2022, the company expects revised adjusted EPS in the range of $7.44 to $7.74, compared to the consensus estimate of $7.73. The prior range stood at earnings of $7.65 to $7.95 per share. Additionally, total net sales are expected to be in line with 2021.

Revlimid sales are likely in the range of $9 billion to $9.5 billion, down from the prior range of $9.5 billion to $10 billion.

Other Developments

Recently, Bristol Myers Squibb bagged the U.S. Food and Drug Administration’s (FDA) approval for the first-of-its-kind cardiac myosin inhibitor Camzyos (mavacamten, 2.5 mg, 5 mg, 10 mg, 15 mg capsules). The allosteric and reversible inhibitor is designed to treat adults with symptomatic New York Heart Association (NYHA) class II-III obstructive hypertrophic cardiomyopathy (obstructive HCM). It aids in improving functional capacity and symptoms.

The U.S. regulator’s decision was based on data from the Phase 3 EXPLORER-HCM trial, which enrolled 251 adults with symptomatic (NYHA class II or III), obstructive hypertrophic cardiomyopathy. The trial met the primary endpoint and demonstrated marked improvement compared to the placebo group for all secondary endpoints.

Analyst Recommendations

Following the positive clinical development and decent Q1 results, BMO Capital analyst Evan Seigerman reiterated a Buy rating and a price target of $87 (15.58% upside potential) on Bristol-Myers Squibb.

Seigerman said, “On the heels of the mavacamten FDA approval, Bristol printed an ok quarter with top- and bottom-line beats (including better-than-expected Revlimid sales, +11%), but product line misses and guidance adjustments give us pause.”

The rest of the Street is cautiously optimistic about the stock, with a Moderate Buy consensus rating based on six Buys, two Holds, and one Sell. That’s alongside an average Bristol Myers Squibb price target of $74.78, which implies 0.65% downside potential to current levels.

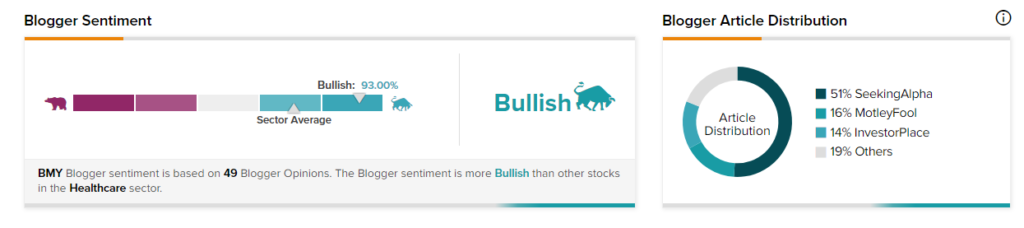

Bloggers Weigh in

Bloggers seem enthused by the company’s earnings results and positive clinical development. TipRanks data shows that financial blogger opinions are 93% Bullish on BMY, compared to a sector average of 71%.

Discover new investment ideas with data you can trust

Read full Disclaimer & Disclosure

Related News:

Unilever Scathed as Inflation Hits Consumer Goods Sector

Moderna Seeks EUA to Vaccinate Young Children with mRNA-1273

Qualcomm Stock Rises on Upbeat Q2 Results, Strong Outlook