Boeing incurred a pre-tax expense of $6.5 billion for its 777X widebody commercial airplane in 4Q as it pushed back the delivery of the aircraft to late 2023. Shares dropped by 4% and closed at $194.03 on Jan. 27.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

During the fourth quarter, the aerospace giant’s revenue fell by 15% year-on-year to $15.3 billion versus analysts’ estimates of $15.1 billion. The company posted a loss of $14.65 per share and a core (non-GAAP) loss of $15.25 per share.

Boeing (BA) CEO Dave Calhoun commented, “2020 was a year of profound societal and global disruption which significantly constrained our industry. The deep impact of the pandemic on commercial air travel, coupled with the 737 MAX grounding, challenged our results.”

“While the impact of COVID-19 presents continued challenges for commercial aerospace into 2021, we remain confident in our future, squarely-focused on safety, quality and transparency as we rebuild trust and transform our business,” Calhoun added.

The grounding of Boeing’s 737 Max aircraft resulted in the company’s backlog worth $363 billion for FY20. (See BA stock analysis on TipRanks)

Meanwhile, the European Union on Jan. 27 granted the planemaker the regulatory approval to bring the 737 Max airplanes back to the skies. US regulators have already lifted the ban on the 737 Max. As of Jan. 25, Boeing delivered over 40 of its 737 Max aircraft, the company said.

The 737 Max had been grounded for a 20-month period, following two fatal crashes.

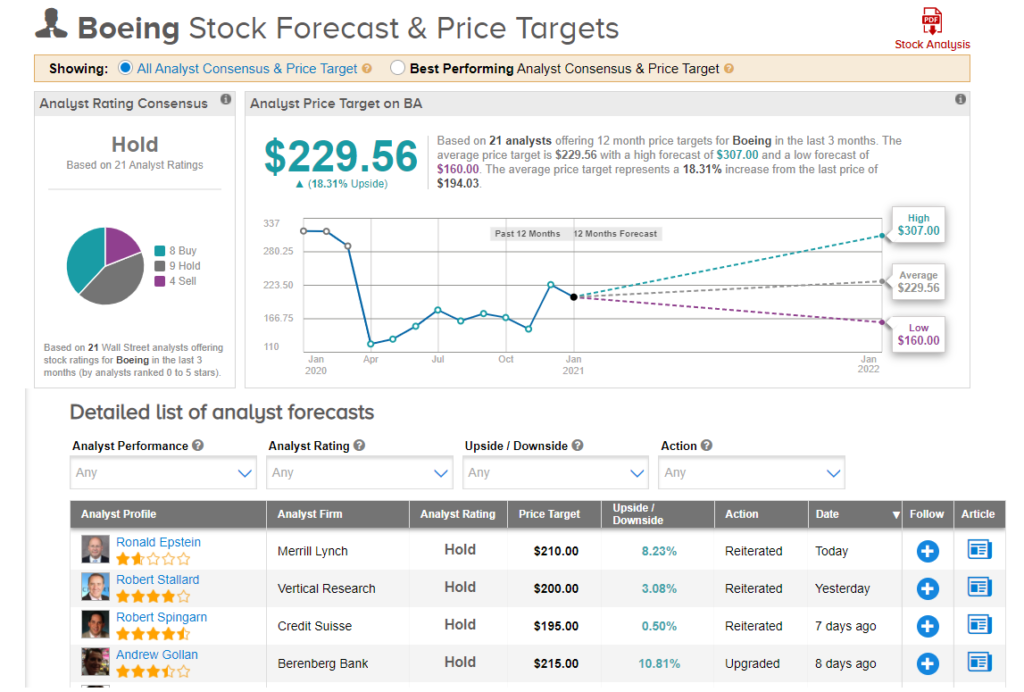

Following the quarterly results, Cowen & Co. analyst Cai Rumohr reiterated a Hold rating on the stock with a price target of $225.

“777X pushout charge & expected continuing high abnormal production charges are key negatives in the Q4 release; continuing plan to hike 737 to 31/month in early 2022 is somewhat encouraging. Investors also will focus on 787 manufacturing issues, preventing deliveries,” Rumohr wrote in a note to investors.

The rest of the Street is in line with Rumohr’s outlook with a Hold consensus rating. That’s based on 8 analysts recommending a Buy, 9 analysts suggesting a Hold and 4 analysts suggesting a Sell. The average analyst price target of $229.56 implies 18.3% upside potential to current levels.

Related News:

AT&T Shares Slide As 2021 Sales Outlook Disappoints

3M Posts Surprise 4Q Profit Amid Strong Demand For Face Masks

Tilray To Supply Medical Cannabis To France; Shares Gain 14%