Given the S&P 500 has delivered returns of 11% already this year, thereby surpassing its historical average of around 10.3%, investors might be inclined to think it a good idea to pack up the year’s investing activities and come back at a later date.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

But that would be a mistake, says billionaire Ken Fisher. The Fisher Investments Founder and its current Executive Chairman and Co-Chief Investment Officer, argues that going by the history books, it will be much more lucrative to stay in a market such as this one. That’s because he says “statistically, average returns aren’t normal – extreme returns are normal.”

Essentially, Fisher’s argument is that while on average the down years balance out the good ones, when a bull market is in play, big returns are the norm, and that happens more often than you might think. “Since 1925, U.S. stocks gained more than 20 per cent in 37 of 98 years – the most frequent result! Next most frequent? Zero to 20-per-cent gains, totaling 35 times,” Fisher, whose investing endeavors have yielded him a net worth of $9 billion, explained.

While Fisher does not necessary think this year will deliver “booming returns” exceeding 20%, he says “it wouldn’t shock me! And now, it shouldn’t shock you. Regardless, when you realize that robust gains aren’t abnormal, you realize ‘too far, too fast’ fears are faulty.”

Well, then, it looks like Fisher’s staying in the market and by doing so remains heavily invested in some of this bull market’s most recognized names – chip heavyweights, Nvidia (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD).

So, let’s take a closer look at the pair and see why you might want to ride the investing legend’s coattails here. For a wider view of these chip giants’ prospects, we also ran the pair through the TipRanks database for some additional color. Here are the details.

Nvidia

First up, Nvidia, a name synonymous with the current market’s biggest trend – AI. This semi giant has been the AI-fueled rally’s firestarter and for good reason. While Nvidia was once primarily a maker of GPUs for the gaming industry, a segment from which it derived the bulk of its revenue, its positioning in the Data Center space has been the catalyst that has turned it into the world’s third most valuable company.

Simply put, Nvidia makes the best AI chips out there. Such is its dominance, its share of the AI chip market stands at more than 90%. Investors first got a glimpse of the outsized success last year as a series of blowout earnings reports first took Wall Street by surprise but have now almost become the norm. While there have been fears the company won’t be able to sustain its tremendous growth, the just-released FQ1 print has put that concern to rest.

In the April quarter, revenue climbed by 262.2% year-over-year to $26.04 billion, beating the analysts’ call by $1.45 billion. That figure factored in record quarterly Data Center revenue of $22.6 billion, amounting to a sequential increase of 23% and a 427% jump vs. the same period a year ago.

There was a beat on the bottom-line too, as adj. EPS of $6.12 outpaced consensus by $0.54. And moving forward, Nvidia expects FQ2 revenue will reach $28.0 billion, plus or minus 2%, while the Street was expecting $26.84 billion.

Surely, Fisher must like all of that as the billionaire has a big stake in Nvidia; he owns 9,133,422 shares, which currently command a market value over $8.67 billion.

For Jefferies’ Blayne Curtis, an analyst ranked in the top 1% of Street stock pros, it is the upcoming release of the Blackwell GPU architecture that should keep the NVDA gravy train on the right track.

“Demand is expected to outpace supply well into next year as Blackwell ramps,” the 5-star analyst said. “This is consistent with our Asia checks (more to come post trip) that suggest NVDA recently increased capacity for 2H and should dispel fears of an air pocket in the 2H. Look for magnitude of beats to accelerate starting in the 2H and accelerating as the GB200 comes to market. Remains top pick with upside to estimates as capacity rises.”

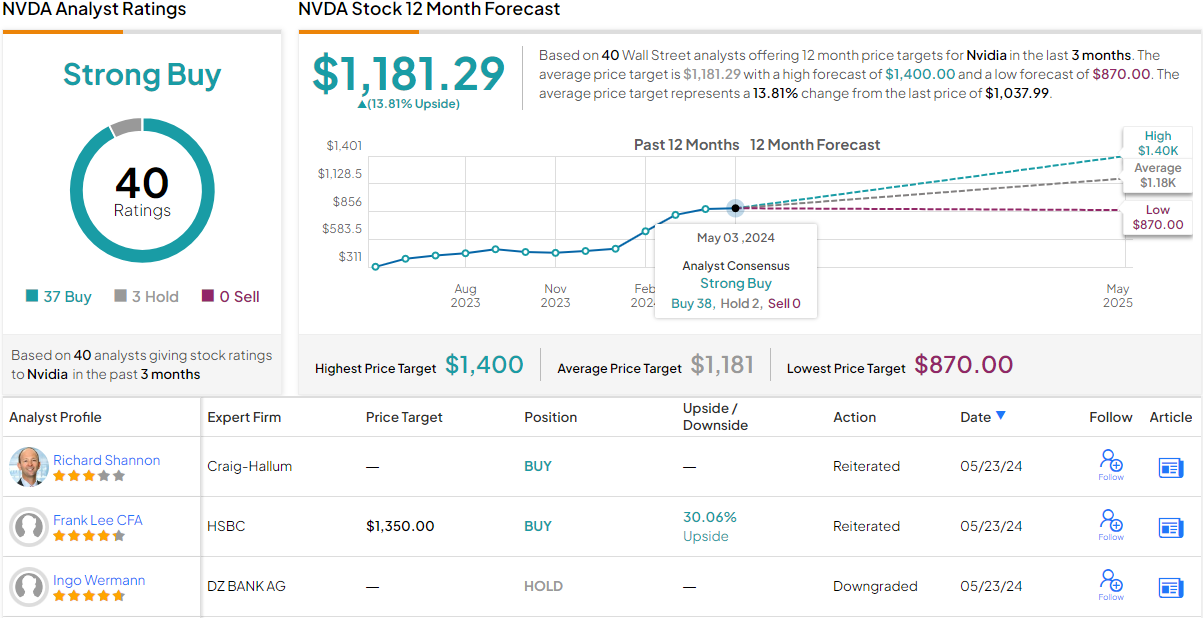

Accordingly, Curtis has a Buy rating on NVDA shares while his price target has moved from $1,200 to $1,350, suggesting the stock will gain another 42% over the coming months. (To watch Curtis’ track record, click here)

The Street currently shows 3 analysts who prefer sitting NVDA out for now, but their Hold ratings are countered by 37 Buys, all naturally coalescing to a Strong Buy consensus rating. The average target stands at $1,181.29, implying shares will deliver returns of ~14% a year from now. (See Nvidia stock forecast)

AMD

Can anyone give Nvidia a run for its money in the AI chip game? That looks to be a tall order right now. But if there’s one company that might be able to close the gap somewhat, AMD is the name that often comes up as the one who might have the wherewithal to do so.

Such a conclusion is not only based on the fact its products aimed at capturing market share (its new MI 300 GPUs, for example) are excellent in their own right but down to the fact that it has already done so in the past. There were times when fellow chip giant Intel was the CPU segment’s undisputed leader. But bringing to market its own great products, and making the most of Intel’s missteps, AMD closed the gap to its once far bigger rival.

It remains to be seen whether it can do the same to Nvidia. In the meantime, there’s an argument to be made that AMD represents a sort of mini-me version of Nvidia. That extends to both the stock market gains, which have been sound but not as majestic and to its quarterly readouts, which have been consistently good without being mind-blowing.

In Q1, revenue rose by 2.2% YoY to $5.47 billion, edging ahead of the consensus estimate by $20 million. Data Center segment revenue also shone here, reaching a record $2.3 billion, amounting to an 80% YoY uptick. At the bottom-line, adj. EPS of $0.62 beat the analysts’ forecast by $0.01. For Q2, the company sees revenue hitting $5.7 billion, plus or minus $300 million. The Street was looking for $5.69 billion.

Meanwhile, Fisher has a substantial stake here too. He owns more than 28.86 million shares boasting a current market value of almost $4.78 billion.

Looking at its prospects, amongst other factors, Wolfe Research’s Chris Caso expects the MI300 will be driving future gains for AMD, saying, “We think MI300 can represent ~$5bn in CY24 revenue and believe a ~$2bn exit rate for the MI300 business by the end of the year is plausible – as that becomes clearer, we believe that will represent an incremental catalyst for the stock. We model CY24/ CY25 server graphics rev contribution of ~$4bn/$7.3bn, and remain constructive on upward AI revenue guidance revisions through 2H24 as demand visibility improves.”

“We anticipate further share gains vs Intel in the datacenter CPU market as Turin launches in 2H24, particularly in the enterprise segment where AMD presently has significantly less share but more opportunity, and enterprise represents higher margin business,” the 5-star analyst went on to further add.

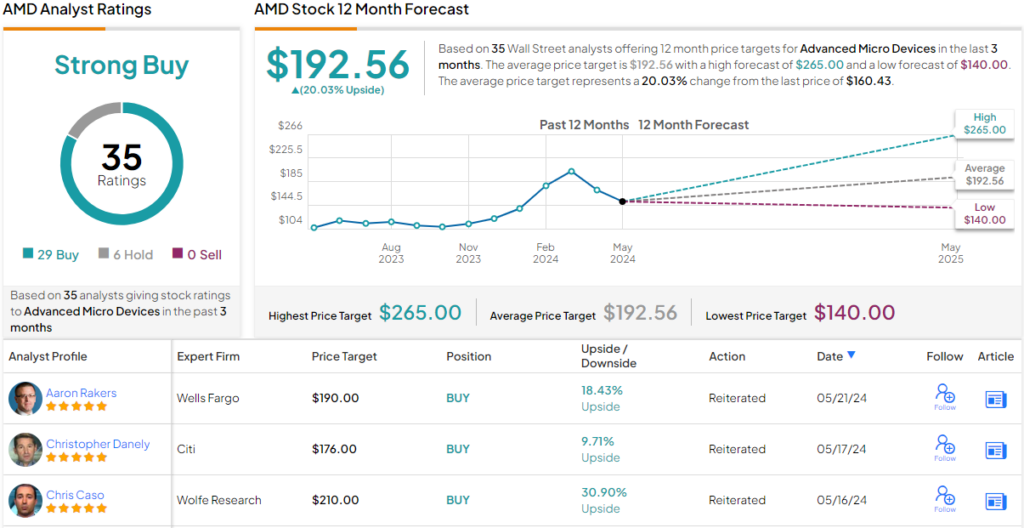

Caso, whose stock recommendations have also positioned him amongst the Street’s top 1%, has an Outperform (i.e., Buy) rating for AMD shares to go along with a $210 price target. The implication for investors? Upside of ~31% from current levels. (To watch Caso’s track record, click here)

Most of Caso’s colleagues agree with that thesis. AMD stock claims a Strong Buy consensus rating, based on a mix of 29 Buys vs. 6 Holds. The average price target stands at $192.56, making room for 12-month returns of 20%. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.