Shares of Bed Bath & Beyond tanked 11% after the retailer’s third-quarter profit and sales missed analysts’ expectations as the resurgence in Covid-19 cases hit store traffic.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Bed Bath (BBBY) reported adjusted net earnings of 8 cents per diluted share for its third fiscal quarter ended November, lagging the 19 cents per share expected by analysts. Net sales during the reported quarter declined 5% to $2.6 billion year-on-year, primarily due to “planned divestitures of non-core banners” and store closures, the company said. Analysts had been looking for quarterly sales of $2.75 billion.

Meanwhile, same-store sales rose 2% as more shoppers went online. Digital sales surged 77% year-on-year, driven by online growth of 94% in Bed Bath’s banner. The retailer said it counted more than 2 million new online customers in the third quarter.

“The consistent execution of our growth strategy is unlocking improved financial performance and we delivered a second consecutive quarter of comparable sales and profit growth,” Bed Bath CEO Mark Tritton said. “Additionally, we drove strong cash flow generation and balance sheet improvements in the third quarter and have re-initiated capital return to shareholders.”

Looking ahead, Bed Bath said that due to the significant pandemic-led headwinds including heavy store traffic declines, major shipping constraints and higher freight costs, the company is not disclosing “specific” sales and earnings guidance for the fiscal 2020 fourth quarter. At the same time, the company expects that its stores will remain open and not be required to close due to government restrictions.

Instead, Bed Bath did provide some directional guidance. The retailer expects significant sales growth to be generated from its digital channels, while store sales are anticipated to be “unfavorably” impacted by declines in store traffic. Net sales in the fiscal 2020 fourth quarter are projected to be lower by a double-digit percentage range. Gross Margin and adjusted EBITDA are expected to be approximately in line with the prior year period, as Bed Bath plans to offset higher freight costs via promotions and markdowns, as well as a favorable product mix.

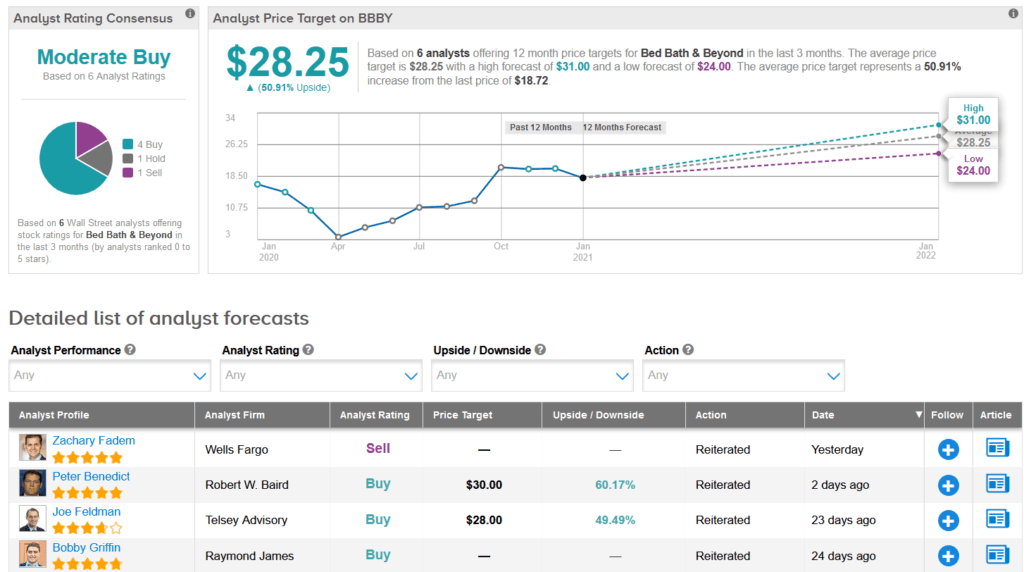

Bed Bath shares have dropped 14% over the past three months, while the average analyst price target of $28.25 suggests that 51% upside potential lies ahead over the coming year.

Wells Fargo analyst Zachary Fadem just this week reiterated a Sell rating on the stock as he sees downside risk to FY21 consensus estimates for BBBY.

“We believe asset sale excitement has begun to wane with the recent sale of Cost Plus (among other assets) and we see 2021 all about management turnaround efforts that likely proves lumpy with no guarantee of success,” Fadem wrote in a note to investors.

The rest of the Street is cautiously optimistic on the stock’s outlook. The Moderate Buy analyst consensus shows 4 Buys, 1 Hold and Wells Fargo’s Sell. (See BBBY stock analysis on TipRanks)

Related News:

T-Mobile Expands 5G Coverage; Street is Bullish

CureVac Teams Up With Bayer On Covid-19 Vaccine; Shares Pop 20%

LafargeHolcim Inks $3.4B Deal To Buy Firestone Building; Shares Rise 4.6%