At a quick glance at the key financial ratios for Zoom Video Communications (NASDAQ:ZM), investors may come away with the impression that the popular teleconferencing platform represents a bargain. However, those thinking about betting big on Zoom need to be cautious. Macro factors imply that the company may be a value trap. Therefore, I am bearish on ZM stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

ZM Stock Entices with Seemingly Positive Datapoints

Not too long ago, ZM stock caught the eye of bullish investors. The company’s metrics, from earnings to forward guidance, make a compelling case for its potential. However, beneath these figures lies a more complex narrative.

Last month, Zoom reported its second-quarter earnings for Fiscal Year (FY) 2024. It reported earnings per share of $1.34, easily surpassing analysts’ predictions of $1.06. Moreover, sales saw a year-over-year increase of 3.6%, reaching $1.14 billion. This tally exceeded analysts’ forecasts by a comfortable $30 million.

The company’s Q3-2023 guidance was also mostly positive. Management projected its revenue and adjusted EPS to range between $1.115-$1.12 billion and $1.07-$1.09, respectively. This stands in contrast to analysts who predicted sales would touch $1.122 billion with an adjusted EPS of $1.03. Following these projections, ZM stock experienced an upswing, reflecting positively on its market status.

Yet, the fundamental driver for Zoom’s potential success might be the persistent work-from-home trend. According to the Bureau of Labor Statistics, nearly 27% of the U.S. workforce operated remotely, at least part-time, during August and September 2022. Intriguingly, academic surveys from institutions like the MIT Sloan School of Management suggest that this figure might actually hover closer to 50%.

In practical terms, this means millions require reliable teleconferencing tools, underscoring the relevance of platforms like Zoom. Furthermore, a brewing discontent is palpable among workers being called back to physical offices. This potential rift between employers and employees could further cement the role of digital communication tools, possibly giving Zoom an even larger audience.

By logical deduction, that’s positive for ZM stock. Still, investors need to be cautious.

A Value Trap Might Await Zoom Speculators

By the combination of financial performances and positive fundamental tailwinds, ZM stock appears to be a winning trade. Specifically, shares trade at a price-to-sales ratio of 4.8x. While this figure seems undervalued relative to the software (system and application) market’s average revenue multiple of 7.14x, Zoom instead could be a value trap.

Diving deeper into Zoom’s financials shows a trend that might be alarming for some investors: its revenue growth is tapering off. Back in FY2021, Zoom reported an impressive revenue of $2.65 billion, marking a 325% surge from the previous year’s figure of $622.66 million. Come FY2022, Zoom’s sales soared to $4.10 billion, a growth of 54.7% year-on-year. Yet, the enthusiasm dwindled in FY2023, where sales of $4.39 billion reflected a mere 7% hike.

More tellingly, on a trailing-12-month (TTM) basis against FY2023, the growth rate slumps to a scanty 1.59%. This gradual descent is further accentuated by the notable dip in the value of ZM stock since October 2020.

However, the concern isn’t just restricted to numbers. Basically, a ground reality is setting in. Big corporations are progressively signaling their employees to return to their office cubicles. Also, while there’s potential for friction between workers wanting to continue remotely and firms pushing for an in-office presence, it’s essential to remember that corporations hold the purse strings.

Further complicating this scenario is the broader economic picture. Americans are neck-deep in credit card debt, which has surpassed the $1 trillion mark. While many workers assume the favorable conditions will persist, this rising debt indicates that the American workforce might not have the leverage it thinks it possesses. Should workers push back too hard against their employers, the financial repercussions could be dire.

Is ZM Stock a Buy, According to Analysts?

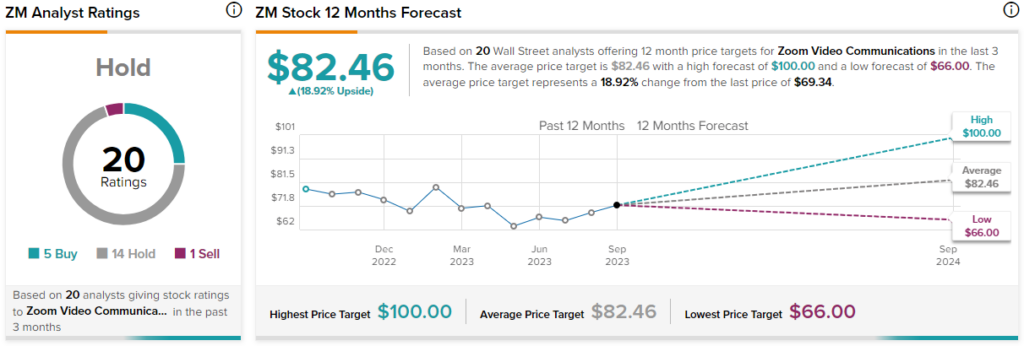

Turning to Wall Street, ZM stock has a Hold consensus rating based on five Buys, 14 Holds, and one Sell rating assigned in the past three months. The average ZM stock price target is $82.46, implying 18.9% upside potential.

The Takeaway: ZM Stock Only Looks Attractive on the Surface

At first glance, ZM stock looks attractive, with metrics suggesting a favorable valuation compared to industry standards. Yet, delving beneath the surface reveals a concerning picture. For example, Zoom’s once-remarkable revenue growth is showing signs of stagnation. Additionally, fundamental shifts in the corporate landscape, like the push for in-office work, cast a shadow over its future prospects. Thus, investors need to think carefully before buying ZM stock.