Oil prices have been quite volatile recently. While a surprise output cut announced by OPEC+, strong Chinese economic data, and declining U.S. inventories are supporting oil prices, concerns about a potential slow down in the U.S. has been a drag. With this backdrop in mind, we used TipRanks’ Stock Comparison Tool, to pit Exxon Mobil (NYSE:XOM), ConocoPhillips (NYSE:COP), and Chevron (NYSE:CVX) against each other to find Wall Street’s top energy stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Exxon Mobil (NYSE:XOM)

Exxon was one of the top-performing S&P 500 (SPX) stocks in 2022, thanks to the spike in oil and gas prices due to the Russia-Ukraine war. The company delivered stellar net income of $55.7 billion in 2022, up 142% from the prior year. Exxon generated free cash flow of $62.1 billion last year.

However, the oil and gas giant recently announced some preliminary Q1 2023 numbers, which indicate decline in earnings compared to the fourth quarter of 2022, due to lower energy prices and other factors.

Is Exxon Stock a Good Buy?

On Tuesday, UBS analyst Jon Rigby upgraded XOM stock from a Hold to Buy and increased the price target to $144 from $125, saying, “We see the Integrated Oils as best positioned to outperform this upcycle, driven by improved balance sheets and significantly more capital efficient asset bases that generate higher FCF with greater visibility to support consistent shareholder returns.”

The analyst’s optimism about Exxon is based on expectations of high-margin upstream volume growth in 2024 and 2025 and capacity additions in downstream and chemicals, while maintaining annual capital expenditure at $20 billion to $25 billion.

Additionally, the analyst projects Exxon’s balance sheet to be in a net cash position by mid-2024, which will give it the flexibility to drive shareholder returns above the $17.5 billion per year buyback pace, while “providing downside support.”

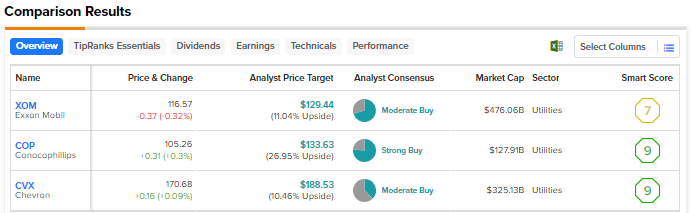

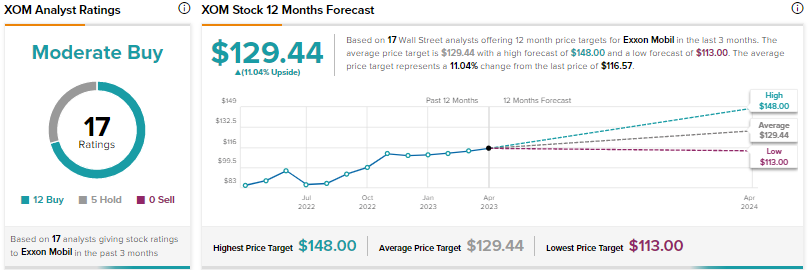

Overall, Wall Street is cautiously optimistic about Exxon, with a Moderate Buy consensus rating based on 12 Buys and five Holds. The average price target of $129.44 suggests 11% upside. Shares have advanced 6% so far in 2023. XOM offers a dividend yield of 3.2%.

ConocoPhillips (COP)

Exploration and production company ConocoPhillips has operations in 13 countries. The company’s 2022 net income grew 131% to $18.7 billion, fueled by higher realized commodity prices and increased sales volumes mainly due to its Shell Permian acquisition.

At its recently-held analyst and investor meeting, ConocoPhillips highlighted its 10-year plan, which aims to generate free cash flow available for distributions of greater than $115 billion.

The company continues to strengthen its balance sheet and is on track to achieve $5 billion debt reduction target by 2026. It retired debt worth $3.3 billion in 2022.

Is ConocoPhillips a Buy, Sell, or Hold?

Morgan Stanley analyst Devin McDermott raised his price target for ConocoPhillips to $122 from $115 and maintained a Buy rating following the analyst and investor meeting on April 12. The analyst feels that given the rising investor focus on inventory, the company’s 30-plus year, below $40 per barrel cost-of-supply resource base differentiates it from its peers.

As part of its 10-year plan, the company aims to hold a resource base of about 20 billion barrels of oil equivalent at less than $40 per barrel WTI, representing a resource life of over 30 years at current production levels. McDermott also believes that ConocoPhillips “checks all the boxes for sustained outperformance.”

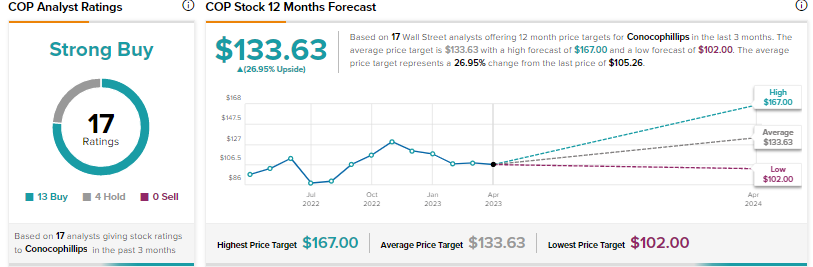

Overall, the Strong Buy consensus rating for ConocoPhillips stock is based on 13 Buys and four Holds. The average price target of $133.63 indicates upside potential of nearly 27% from current levels. Shares have declined 5% since the start of 2023. COP’s dividend yield stands 2.2%.

Chevron (NYSE:CVX)

Chevron’s net income surged 128% to $35.5 billion in 2022, while free cash flow increased 78% to $37.6 billion. The company is focused on strengthening its traditional oil and gas and new energy businesses.

Earlier this year, Chevron confirmed its annual organic capital expenditure guidance of $13 billion to $15 billion through 2027. The company projects annual free cash flow growth of greater than 10% at $60 Brent level.

What is the Price Target for Chevron Stock?

Last week, Scotiabank analyst Paul Cheng upgraded Chevron stock from a Hold to Buy and raised the price target to $200 from $195. Cheng feels that Chevron could outperform Exxon due to its “higher oil leverage following the OPEC+ latest production cut announcement.”

In contrast, the analyst downgraded Exxon to a Hold from Buy due to the company’s larger exposure to refined products, which he believes could impact earnings, as the refining market might reach an inflection point in the second half of this month.

With five Buys and ten Holds, Chevron earns Wall Street’s Moderate Buy consensus rating. The average price target of $188.53 suggests 10.5% upside. Shares are down 5% year-to-date. Chevron offers a dividend yield of 3.5%.

Conclusion

Analysts are cautiously optimistic about Exxon and Chevron, while they are more bullish on ConocoPhillips. Wall Street sees higher upside potential in ConocoPhillips than the other two energy stocks. As per TipRanks’ Smart Score System, ConocoPhillips scores a nine out of 10, implying that the stock could outperform the broader market.