Coming off last year’s merciless bear market year, billionaire value investor David Einhorn managed to buck the trend and steer his hedge fund Greenlight Capital to its best performance in a decade. Now, Einhorn finds himself a bit worried about what might come next.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

“If we were ‘bearish’ until March and ‘neutral’ through June, we would now characterize ourselves as ‘worried,’” he recently said. “Should long-term interest rates rise, either due to the strong economy or due to supply/demand issues in the Treasury market, the market could revisit the disinflation theme that has supported the recent advance. We think a reacceleration of inflation and higher rates could disrupt the bull narrative, which has now obtained consensus support. In anticipation, we have tightened our net exposure…”

That said, given his day job involves finding the stocks that will deliver returns no matter the macro backdrop, Einhorn also says that even should the markets enter another difficult phase, the onus is on his fund to find profits in the portfolio. “On that front,” Einhorn concludes, “count us as optimistic!”

With that cautious yet optimistic approach in tow, Einhorn has actively been seeking out the equities that will deliver those profits, and during Q2, he opened positions in two new names. According to the TipRanks database, both stocks are Buy-rated by the Street’s analysts. Let’s see why they would make good additions to a portfolio right now.

NET Power Inc. (NPWR)

Our first Einhorn-backed name is a newcomer to the stock market scene. NET Power, a clean energy enterprise, emerged as a public company just this June, making its debut through the SPAC pathway and amassing over $670 million in the process.

NPWR essentially operates as a licensing enterprise, bringing to market a patented power cycle known as the Allam-Fetvedt Cycle or NET Power Cycle (NPC). It was pioneered by 8 Rivers Capital and involves the use of supercritical carbon dioxide (sCO2) power cycles to generate clean electricity from natural gas in an efficient manner.

The company aims to license its technology and modify it for application in various sectors. This results in a business model that is light on assets, offering access to a worldwide market whilst offering higher gross margins.

The initial utility-scale 300 MWe NPWR plant is presently in the Front-End Engineering Design (FEED) phase, with operations anticipated to kick off in the latter half of 2026. This project is being collaboratively undertaken by NPWR and a consortium of associates, including Occidental Petroleum, Baker Hughes, Constellation Energy, and 8 Rivers, all of whom hold ownership stakes in NPWR.

Einhorn is also amongst the equity holders. It didn’t take much time for him to load up. He purchased 2,510,000 shares in Q2, which currently command a market value of $37 million.

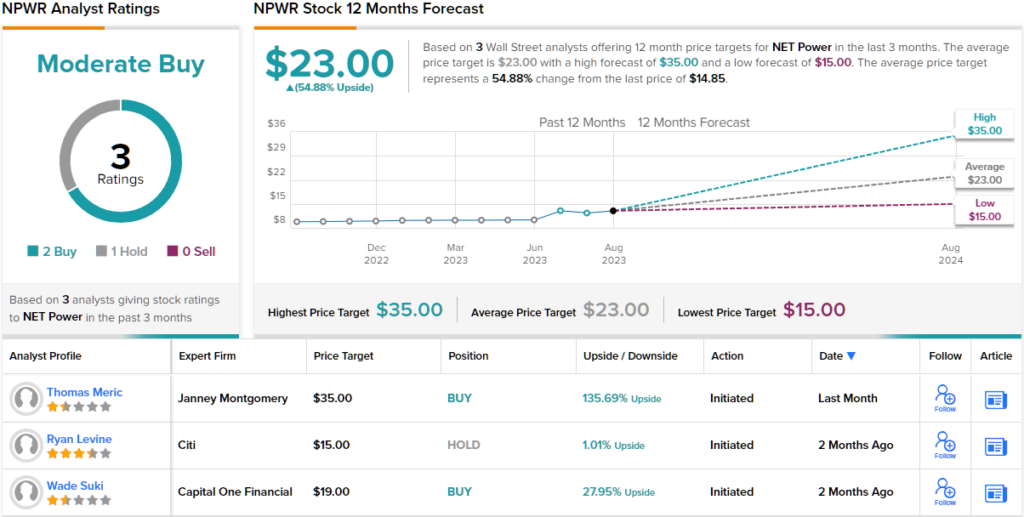

Also showing confidence in this new stock market participant is Janney Montgomery analyst Thomas Meric, who points out how NPWR sets itself apart from the competition.

“We think sCO2 power cycles will become the standard for newbuilds over the next several years based on the supporting physics of its density, its inherent carbon capture, and its lack of other emissions, eventually displacing much of the air breathing fleet. NPWR’s offering is well ahead of competing cycles, not only in terms of process IP, facility demonstration, control system, capitalization, and commercial partnerships, but also in terms of modeled theoretical efficiency and costs,” Meric opined.

These comments underpin Meric’s Buy rating on NPWR, while his $35 price target makes room for big gains of 127% over the coming year. (To watch Meric’s track record, click here)

Overall, NPWR has received 3 analyst reviews since going public, 2 Buys and 1 Hold, making the consensus view here a Moderate Buy. At $23, the average target suggests shares will deliver returns of ~55% a year from now. (See NPWR stock forecast)

First Horizon Corporation (FHN)

Founded all the way back in 1864, First Horizon Corporation is a holding company that, through its banking subsidiary First Horizon Bank, offers the usual array of financial services. These include checking accounts, savings offerings, mortgage banking, lending, whilst also providing individuals and businesses with financing. The bank has a strong presence in the Southeast, a region where it is the fourth biggest regional bank.

2023 has been no easy ride for FHN stock, however. First, the stock got caught in the banking sector woes which saw several banks collapse in the early part of the year. Then things got even worse for investors, when at the start of May, its proposed merger with TD Bank was called off. The result of all the upheaval has been a stock that has shed 47% year-to-date.

Nevertheless, in spite of a difficult operating environment, during Q2, deposit balances rose by $4 billion, or 6.5%, quarter-over-quarter, with the company seeing more than 32,000 new-to-bank clients generating $3.5 billion in deposit balances. At the bottom-line, however, adj. EPS of $0.39 fell short of the consensus estimate by $0.02.

All told, Einhorn must like what’s on offer here. During Q2 he initiated a new position in FHN with the purchase of 1,298,780 shares. At the current share price, these are worth ~$16.4 million.

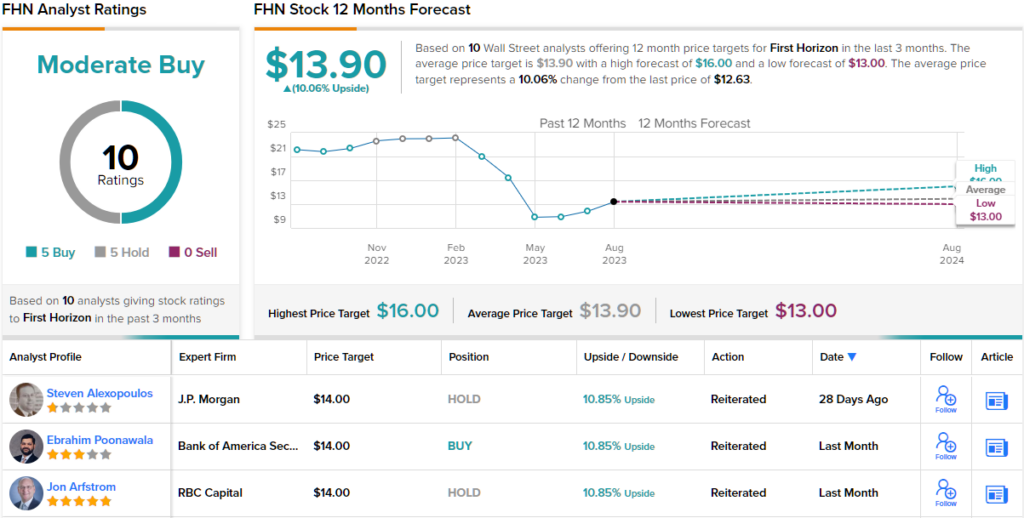

Despite the recent issues, Wells Fargo analyst Jared Shaw also sees plenty of value in this bank.

“Earnings for 2Q23 were a bit messy with the dissolution of the TD transaction, but were highlighted by excellent growth on both sides of the balance sheet,” Shaw opined. “This quarter helped to calibrate Street expectations, as we get a better look at what 6.5% deposit growth costs in this highly competitive environment. There remains wood to chop in regaining an offensive footing, which included accelerated tech. spend, but the current ~120% of TBV valuation remains an attractive entry point.”

Accordingly, Shaw rates FHN shares an Overweight (i.e. Buy) alongside a $16 price target. The implication for investors? Upside of ~27% from current levels. (To watch Shaw’s track record, click here)

Elsewhere on the Street, the stock garners an additional 4 Buys and 5 Holds, all coalescing to a Moderate Buy consensus rating. The forecast calls for 12-month returns of 10%, considering the average target stands at $13.90. (See FHN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.