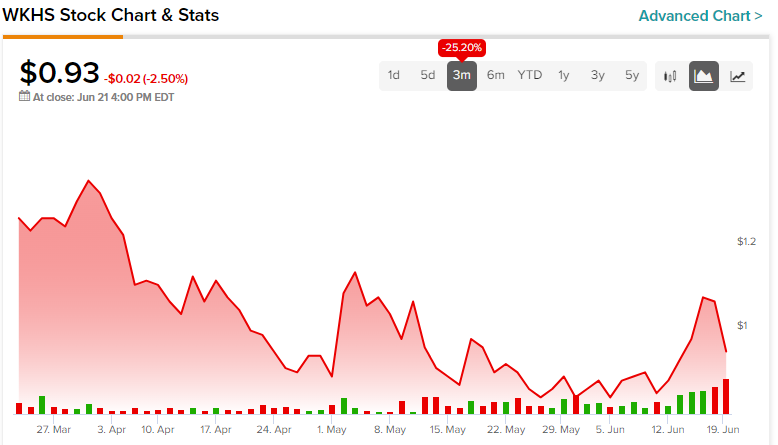

Soaring just over 25% last week (the stock has pulled back since), commercial fleet electric vehicle manufacturer Workhorse (NASDAQ:WKHS) might seem like an enticing wager. Even some analysts bought into the narrative. However, even with fading raw material costs and the power of speculation, the EV upstart is still quite risky. Therefore, I am bearish on WKSH stock.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Why WKHS Stock Suddenly Got So Intriguing

In recent sessions, several EV and automotive-related enterprises – particularly those suffering from less-than-desirable financial statistics – popped sharply last week. Perusing various analyses, no one central catalyst appears to be responsible for the enthusiasm. Arguably, though, the combination of fading raw material costs and good old speculation may have invigorated WKHS stock and its ilk.

Regarding the former point, it’s helpful to look back at what materialized last year. In June, TipRanks’ Swati Goyal noted that EV sector giant Tesla (NASDAQ:TSLA) hiked prices on its car models in the U.S. due in large part to rising raw material costs. Basically, the move represented a familiar tale — passing down increased costs to the consumer.

However, following aggressive efforts by the Federal Reserve to curb skyrocketing prices, this year, raw materials prices started to fade. Fundamentally, this dynamic should help beleaguered EV manufacturers to bolster production, which was also hampered by various supply-chain challenges. On paper, then, WKHS stock seemingly enjoys a rational reason for its dramatic pop.

However, Wall Street learned in the post-pandemic new normal that directed irrationality levers considerable power. Specifically, many retail traders no longer shy away from betting on deeply-embattled enterprises. Indeed, they prefer this contrarian practice in the hopes of sparking a short squeeze.

With WKHS stock featuring a short interest of 25.38% of its float – an elevated figure – it’s no surprise that under the context of speculation, Workhorse blossomed. However, investors need to be extremely cautious about chasing this flawed and vulnerable EV company.

Workhorse Just Isn’t Working

Looking at the company’s latest results, few things appear to be working as they should. Most notably, Workhorse posted revenue of $1.7 million in the first quarter of 2023. That’s well below the $14.3 million generated in the year-ago quarter.

To be sure, it’s not a fair comparison. Given the seismic changes that erupted in 2022, investors must extend grace to companies that were vulnerable to supply-chain disruptions of key commodities. Also, once outside circumstances normalize, Workhorse may be back on track, thus justifying the rally of WKHS stock.

Nevertheless, market participants should carry a heavy dose of skepticism toward any high-risk enterprise. For WKHS stock, the problem comes down to viability. Based on data from TipRanks, Workhorse’s cash and cash equivalents account amounts to only $79.1 million. However, its Q1 free cash flow (FCF) came out to a loss of $38.16 million. In Q4 2022, the FCF loss was $33.13 million.

Stated differently, Workhorse probably can’t just rely on investor sympathy regarding the great disruption of 2022. Instead, it needs to start delivering substantively on the financial print. Otherwise, it risks running out of cash.

A Crazy Premium for a Troubled Business

Cash burn isn’t the only problem impacting WKHS stock. Instead, prospective investors must pay a wild premium for the privilege of equity ownership. Frankly, that might be too much of an ask.

At the moment, the market prices WKHS stock at 26 times trailing-12-month sales. Without benefiting from sector data, it’s relatively easy to presume that such a ratio is wildly overvalued. In fact, data provided by NYU Stern School of Business shows that the price-to-sales ratio for the auto and truck industry is only 1.3 times.

Let’s look at it this way. If you buy WKHS stock right now, you’ll be paying a premium of nearly 20 times relative to its sector. Almost surely, astute, rational investors will walk away unless they know with high confidence that Workhorse can deliver.

Not even almighty Tesla (NASDAQ:TSLA) – which is priced at 9.6 times trailing sales – has a valuation multiple approaching Workhorse’s. Unless you have a crystal ball, you’re taking a massive risk with WKHS stock.

Is WKHS Stock a Buy, According to Analysts?

Turning to Wall Street, WKHS stock has a Moderate Buy consensus rating based on two Buys, one Hold, and zero Sell ratings. The average WKHS stock price target is $3.17, implying 242% upside potential.

The Takeaway: WKHS Stock Simply Isn’t Worth the Trouble

While some elements of last week’s sharp rise in WKHS stock make sense – particularly the fading costs of raw materials – it still represents a high-risk venture only appropriate for professional gamblers. Financially, Workhorse appears vulnerable due to its cash burn. Also, investors would be paying a hefty premium for equity ownership.